Advertisement|Remove ads.

Dell's 'Best Quarter Ever' Is Not Just A One-Time Phenomenon, Say Analysts — Wall Street Hikes Price Target By Up To 200%

- Piper Sandler analyst James Fish raised his price target on Dell to $497 from $167 while maintaining an ‘Overweight’ rating.

- Fish described the quarter as "what many will call its best quarter ever," noting that Dell’s revenue growth during Q1 was driven largely by AI infrastructure deployments.

- He added that the performance was not merely a one-quarter phenomenon, as the company's backlog and sales pipeline continue to grow faster than revenue.

Advertisement|Remove ads.

Dell Technologies Inc.’s (DELL) blowout first-quarter (Q1) results have Wall Street buzzing with optimism, with analysts hiking their price targets by up to 200% on Friday.

According to TheFly, analysts at Barclays hiked their price target for Dell to $505 from $168, while keeping an ‘Overweight’ rating on the stock, citing the company’s beat-and-raise Q1 results and guidance for fiscal year 2027.

Dell shares were up more than 35% in Friday’s pre-market trade after closing about 4% higher on Thursday. DELL was among the top trending tickers on Stocktwits at the time of writing.

Advertisement|Remove ads.

DELL’s Q1 Performance Not A One-Time Phenomenon, Says Wall Street

Piper Sandler analyst James Fish raised his price target on Dell to $497 from $167 while maintaining an ‘Overweight’ rating. Fish described the quarter as what "many will call its best quarter ever," noting that Dell’s revenue growth during Q1 was driven largely by AI infrastructure deployments.

He added that the performance was not merely a one-quarter phenomenon, as the company's backlog and sales pipeline continue to grow faster than revenue. While some demand may have been pulled forward amid ongoing industry supply constraints, Piper Sandler believes Dell's growth momentum remains firmly intact.

JPMorgan raised its price target on Dell to $500 from $280 and maintained an ‘Overweight’ rating, citing stronger-than-expected demand and a materially higher fiscal 2027 outlook. The firm said Dell's expanding pipeline provides greater visibility, with underlying demand remaining robust despite some pull-forward effects.

Advertisement|Remove ads.

Wells Fargo analysts said the biggest surprise from Dell’s results was non-AI server revenue, which surged 93% year over year to $8.5 billion, far exceeding expectations. The firm raised its price target on Dell to $505 from $270 and maintained an ‘Overweight’ rating.

UBS raised its price target on Dell to $440 from $243 while maintaining a ‘Neutral’ rating, cautioning that supply constraints, potentially unsustainable PC strength, and weaker second-half earnings could limit further upside.

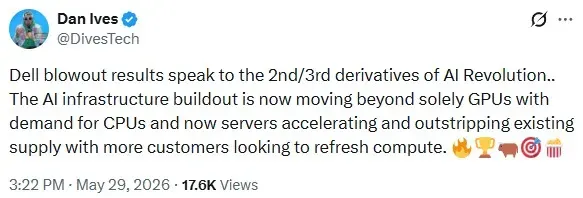

Wedbush’s Global Head of Tech Research, Dan Ives, said in a post on X that Dell’s Q1 results speak to the second and third-order derivatives of the AI revolution.

Advertisement|Remove ads.

“The AI infrastructure buildout is now moving beyond solely GPUs with demand for CPUs and now servers accelerating and outstripping existing supply with more customers looking to refresh compute,” he said.

According to Koyfin data, of the 27 analysts covering Dell, 18 have a ‘Buy’ or ‘Strong Buy’ rating, seven recommend ‘Hold’, while two rate it ‘Sell.’

DELL’s Q2 And FY27 Guidance

Dell expects second-quarter (Q2) revenue to come in between $44 billion and $45 billion, growing 49% year-over-year at a midpoint of $44.5 billion.

Advertisement|Remove ads.

For fiscal year 2027, Dell expects revenue to range between $165 billion and $169 billion, growing 47% YoY to a midpoint of $167 billion. The company had previously guided for FY27 revenue to come in between $138 billion and $142 billion during its fourth-quarter (Q4) results.

Dell reported earnings per share (EPS) of $4.86 on revenue of $43.8 billion, compared to Wall Street estimates of an EPS of $2.96 on revenue of $35.8 billion, according to Fiscal.ai data.

How Did Retail Traders React To Dell?

Retail sentiment on Stocktwits around Dell trended in the ‘extremely bullish’ territory, with message volumes at ‘extremely high’ levels at the time of writing.

Advertisement|Remove ads.

One bullish user believes that the rally in Dell shares is not over yet, and that the stock is going the AMD route.

DELL stock is up 152% year-to-date and 179% over the past 12 months. The S&P 500 ETF Trust (SPY) and the iShares Core S&P 500 ETF (IVV) are up 28% over the past 12 months.

Advertisement|Remove ads.

The Vanguard Total Stock Market Index Fund ETF (VTI) is up 29% during this period, while the State Street Technology Select Sector SPDR ETF (XLK) is up 62%.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1234739851_1_4e5d1263a0.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·1h ago

Anushka Basu·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1317870360_fd65c7f7d0.jpg) Anushka Basu·3h ago

Anushka Basu·3h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2245018150_cbf31ea70f.jpg) Anushka Basu·5h agoAnushka Basu·6h ago

Anushka Basu·5h agoAnushka Basu·6h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2208663076_29e54f9e10.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·14h ago

Shashank Nayar·14h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2282676708_jpg_9f31eb6ee5.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·14h ago

Anan Ashraf·14h ago