Advertisement|Remove ads.

Trump Orders Fed To Reassess Fintech Access To Payment System – As Crypto Firms Eye Access

- The Fed and federal regulators have 90 days to review fintech access to U.S. payment rails and rule on master account applications under Trump's new executive order.

- The White House said current rules "favor incumbents at the expense of innovators," language that Coinbase's Paul Grewal, Custodia's Caitlin Long, and Sen. Cynthia Lummis praised.

- ABA wanted unified standards for all bank-like entities, while ICBA defended Fed discretion and urged a pause on stablecoin and master account policies.

Advertisement|Remove ads.

U.S. President Donald Trump on Tuesday signed an executive order requiring federal financial regulatory agencies to re-evaluate rules that restrict fintech and digital asset companies’ access to the U.S. payment system. Executives in the cryptocurrency industry immediately voiced support, while banking trade groups issued cautious responses.

The executive order mandates that the Federal Reserve assess the legal framework governing relevant institutions’ access to payment accounts. All federal regulatory agencies must submit their research conclusions within 90 days. The White House fact sheet explicitly stated that within the same time frame, the Federal Reserve must complete the review and approval of master account applications that meet statutory requirements.

Federal Reserve master accounts, which allow institutions to directly access the Federal Reserve’s payment infrastructure, were originally only open to traditional banks. In recent years, most applications submitted by fintech and cryptocurrency firms, including Ripple (XRP), Kraken, and Custodia, have been rejected or remain unresolved. The current administration has criticized existing payment rules, saying that so far the rules have “favor[ed] incumbents at the expense of innovators."

Advertisement|Remove ads.

The new executive order builds on Trump’s earlier orders, which established a Strategic Bitcoin Reserve (SBR) and advanced the GENIUS Act, legislation that regulates payment stablecoins. Previously, JP Morgan (JPM) also acknowledged that it had closed Trump’s accounts after the President filed a $5 billion lawsuit against CEO Jamie Dimon.

Industry Response

Shortly after this statement was released, stakeholders across multiple sectors in the United States issued various responses to regulatory issues, including cryptocurrency firms. Parties supporting open access were the first to speak out.

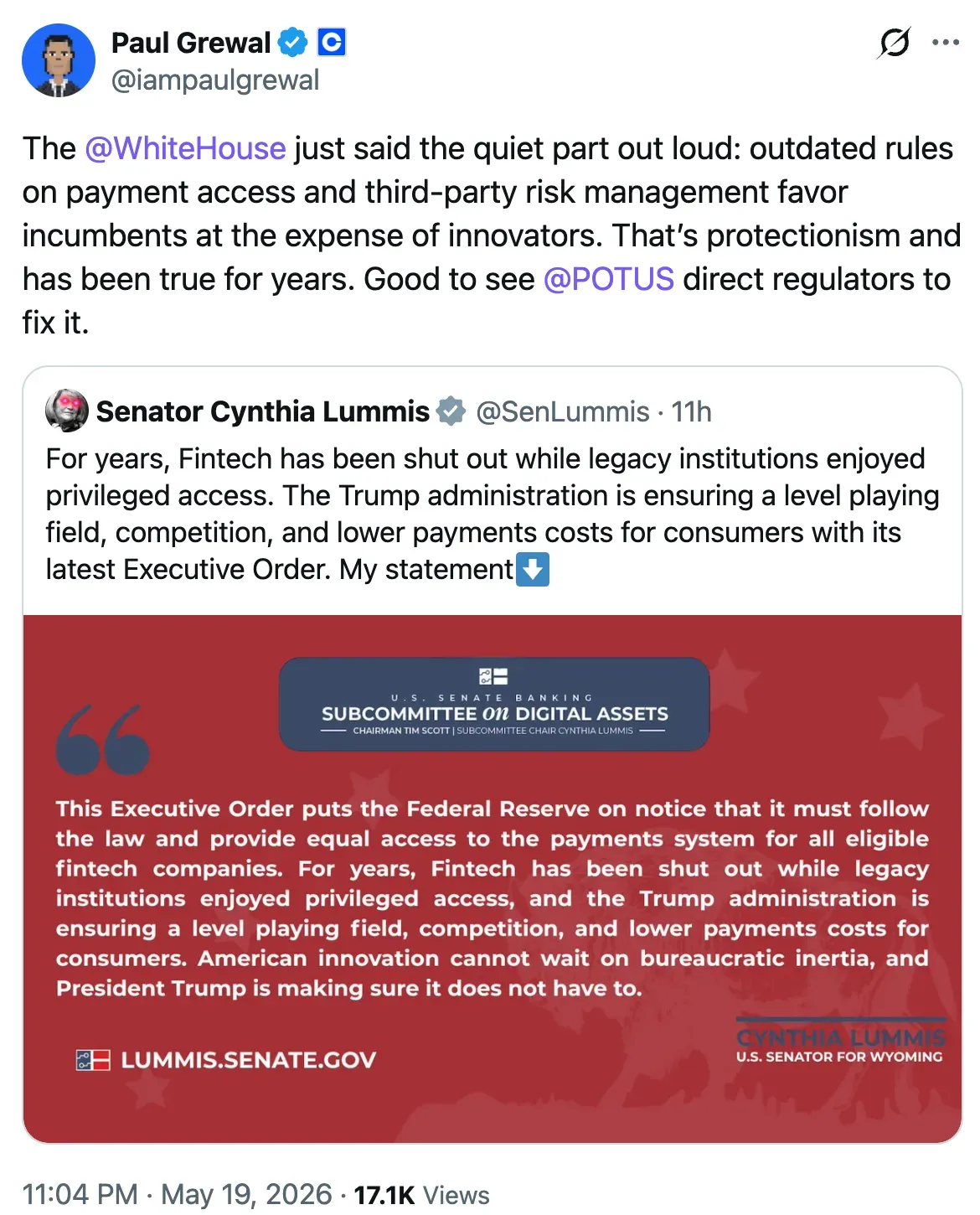

Paul Grewal, Chief Legal Officer of Coinbase (COIN), said on X, “outdated rules on payment access and third-party risk management favor incumbents at the expense of innovators. That’s protectionism and has been true for years.”

Advertisement|Remove ads.

Caitlin Long, Founder and CEO of Custodia Bank, who was denied access to a Federal Reserve master account in 2023, and Cynthia Lummis, Senator (R-WY) who is the Chair of he Sentate Banking Committee’s Digital Assets Subcommittee, all called for compliant institutions to receive equal access to payment systems.

The banking community adopted a cautious stance. Rob Nichols, President of the American Bankers Association (ABA), demanded that all bank-like entities comply with unified regulatory standards, while Rebecca Romero Rainey, President of the Independent Community Bankers of America (ICBA), argued that the Federal Reserve should retain discretionary authority to review and approve master account applications. The ICBA also called for a suspension of new policies related to stablecoins, Federal Reserve master accounts, and OCC national trust charters.

All Eyes On New Fed Chair

Kevin Warsh, who will be sworn in as Chair of the Federal Reserve to succeed Jerome Powell, was nominated by Donald Trump. He was confirmed by the Senate on May 13 by a vote of 54-45. He previously served as an advisor to cryptocurrency investment firm Electric Capital and has called on the Federal Reserve to implement reforms to its regulatory system.

Advertisement|Remove ads.

As of Wednesday morning, the Federal Reserve had not issued any public response.

Read also: 'What Is XRP Really Doing?': Helius Founder Says Zcash Mispriced Below XRP, BNB — Targets 10% Of Bitcoin's Market Cap

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_trump_airforceone_Jul9_jpg_f56fdf4d39.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·9h ago

Anushka Basu·9h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2182554552_jpg_787178ad47.webp) Anushka Basu·9h ago

Anushka Basu·9h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_166274033_jpg_0fe9601e87.webp) Anushka Basu·10h ago

Anushka Basu·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1252110749_2cb6360816.jpg) Anushka Basu·12h ago

Anushka Basu·12h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2118998147_7e5bba34cd.jpg) Anushka Basu·13h ago

Anushka Basu·13h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_morgan_stanley_bitcoin_jpg_6c2c7ffcd9.webp) Anushka Basu·14h ago

Anushka Basu·14h ago