Advertisement|Remove ads.

Akamai Technologies Q4 Earnings Likely To Decline, But Analyst Says Expect A Surprise In 2025: Retail Sentiment Perks Up

Akamai Technologies Inc. (AKAM) is on course to post a fall in earnings as it gears up to announce its fourth-quarter results on Thursday after the bell.

According to Wall Street consensus, Akamai’s earnings per share (EPS) are likely to be $1.52 in Q4, down from $1.69 a year earlier.

On the other hand, Akamai’s topline is expected to see modest growth—Wall Street expects the company to post revenue of $1.02 billion during Q4, up from $995 million during the same period a year ago.

Advertisement|Remove ads.

Akamai’s recent record shows that the content delivery network and cybersecurity provider’s earnings have beaten estimates in the previous four quarters, while revenue surpassed expectations in only two.

However, analysts at UBS underscored that Akamai’s margins have expanded minimally, while Citi’s recent survey pointed to “mostly uninspiring” results in the information security segment, according to The Fly.

Not everyone is as unoptimistic about Akamai’s prospects, though.

Advertisement|Remove ads.

Analysts at Scotiabank are bullish on U.S. software equities in 2025 after a good showing in 2024. The brokerage raised its price target for the Akamai stock to $115 from $112, implying an upside of 15% from Wednesday’s close. It maintained an ‘Outperform’ rating on the stock.

The brokerage added that Akamai could deliver earnings surprises in 2025, resulting in some estimate revisions.

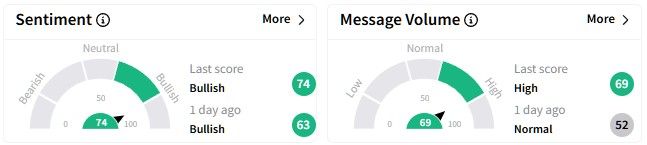

Retail sentiment on Stocktwits around the Akamai stock perked up from a day ago while remaining in the ‘bullish’ (74/100) territory as earnings inch closer.

Advertisement|Remove ads.

Message volumes climbed into the ‘high’ (69/100) level, showing increased interest among retail investors on the platform.

Akamai’s stock has witnessed volatility over the past few months – it fell 1.4% during the last six months, and its one-year performance is worse, with a decline of nearly 7.5%.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Coinbase_ed6fc0a54f.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·9h ago

Anushka Basu·9h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2246906029_12e72a0754.jpg) Anushka Basu·10h ago

Anushka Basu·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_kevin_o_leary_OG_jpg_2789641a97.webp) Anushka Basu·11h ago

Anushka Basu·11h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_495548174_f3e67390cf.jpg) Anushka Basu·13h ago

Anushka Basu·13h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2286958469_d1bf5147bd.jpg) Anushka Basu·14h ago

Anushka Basu·14h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1042183586_jpg_3373e909e0.webp) Anushka Basu·16h ago

Anushka Basu·16h ago