Advertisement|Remove ads.

PYPL Stock Is Trading Near The Cheapest Valuation In Years — So Why Is Wall Street Still On The Fence?

- Despite the discounted valuation, Wall Street remains cautious about the company’s growth prospects.

- According to Koyfin data, 31 out of 43 analysts rate the company a ‘Hold.’

- Most recently, Piper Sandler analyst Bill Carcache lowered the price target on PayPal to $42 from $46 and maintained a ‘Neutral’ rating on the shares.

Advertisement|Remove ads.

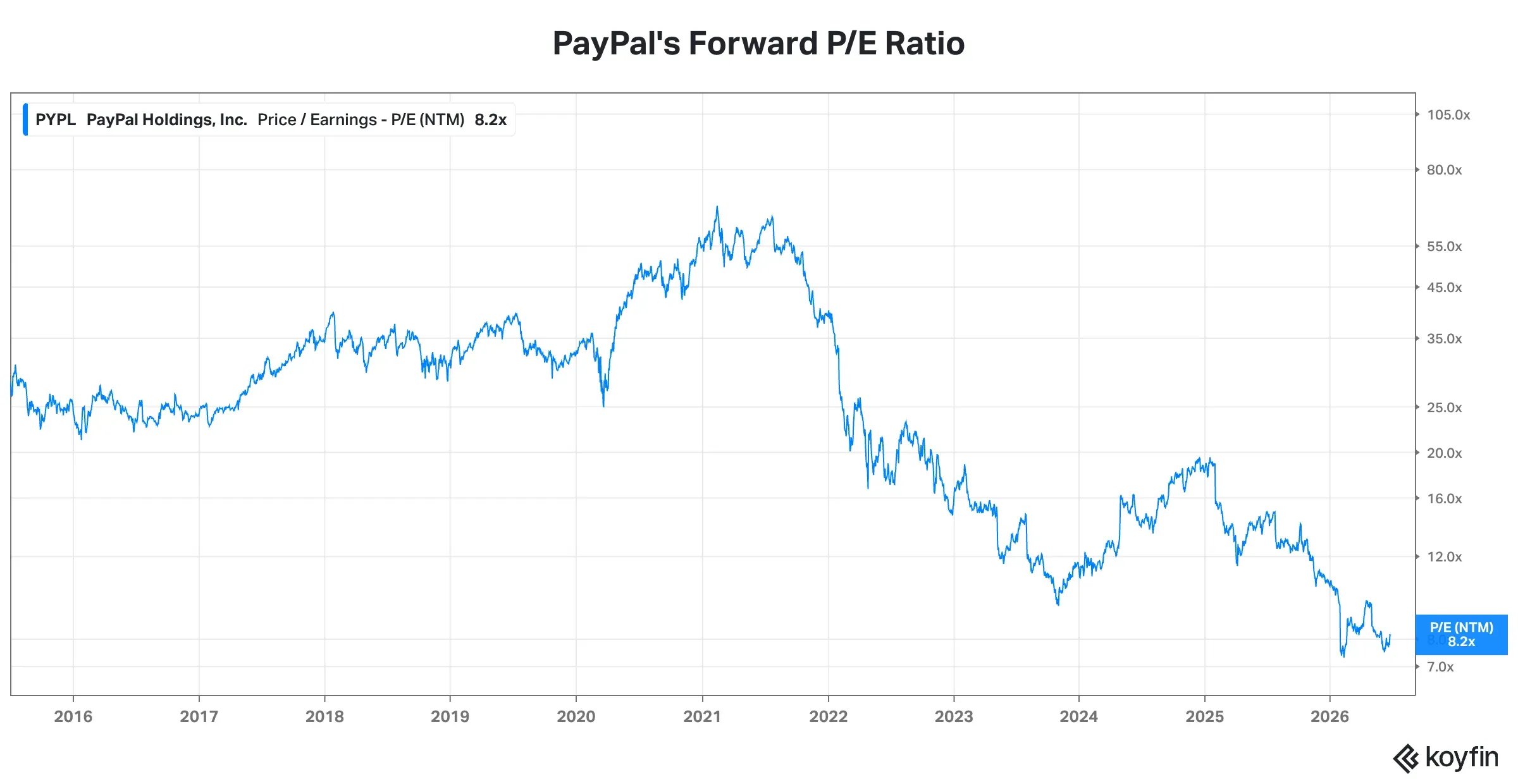

PayPal Holdings Inc. (PYPL) shares are down about 40% in the last year, and the stock’s valuation multiple is nearing decade lows.

According to Koyfin data, the stock’s forward price-to-earnings ratio is at 8.2. Meanwhile, companies like Affirm Holdings (AFRM) and Wise Group PLC (WSE) trade at forward valuation multiples of 21.2x and 21.1x, respectively.

Wall Street Stance On PayPal

Despite the discounted valuation, Wall Street remains cautious about the company’s growth prospects. According to Koyfin data, 31 out of 43 analysts rate the company a ‘Hold,’ even though the 12-month average price target indicates a 16% upside from its last closing price.

Advertisement|Remove ads.

Most recently, Piper Sandler analyst Bill Carcache lowered the price target on PayPal to $42 from $46 and maintained a ‘Neutral’ rating on the shares. The analyst launched coverage of the payments and consumer finance group with a "selectively constructive" view, according to TheFly.

Earlier this month, Morningstar said in its coverage of PayPal that 2026 will be a reset year for the payments firm. The analyst cited the company’s network of merchants and consumers as a positive factor in building and maintaining a strong competitive position in the online payments channel. However, the analyst also noted that the company has faced headwinds following the reversal of pandemic-related trends and the emergence of new competition.

At the same time, Morningstar highlighted management’s efforts to increasingly focus on cost control and product innovation to drive higher profitability and growth. “We see this evolution as the right move, but it will likely take some time to fully execute,” the analyst said.

Advertisement|Remove ads.

“PayPal remains a somewhat unique player within the payments space. We think this remains its key strength, but its position on both the merchant and consumer side could be increasingly challenged over the long run,” it added.

PYPL: Financial Snapshot

PayPal reported first-quarter results in May, posting net revenue of $8.4 billion, up 7% year-over-year, although GAAP operating income declined 3% to $1.5 billion.

The company said that its total payment volume increased 11% to $464 billion, underscoring ongoing growth in payment activity across the platform. The company ended the quarter with 439 million active accounts and generated $0.9 billion in free cash flow.

Advertisement|Remove ads.

PayPal's new CEO, Enrique Lores, who took the reins of the company in March, is focused on improving operating efficiency, modernizing the technology stack, and driving profitable growth. Meanwhile, the company is pursuing an aggressive buyback strategy, repurchasing $1.5 billion in shares in Q1 and bringing its total buybacks over the trailing 12 months to $6 billion.

In the latest earnings call, Lores said PayPal would focus on “becoming a technology company again, sharpening our focus on consumers, aligning the company around three strong businesses, and simplifying how we work with clear accountability and a stronger emphasis on execution.”

PYPL Stock: Retail Stance

On Stocktwits, retail sentiment around PYPL stock has remained in the ‘bearish’ territory over the past week, even as message volume on the platform has surged 937% in the past 24 hours.

Advertisement|Remove ads.

Investors expressed their discontent with management over the company’s recent underperformance.

One bearish user said, “Watch all those buybacks! Wow they really do a lot! Management is incompetent.”

Advertisement|Remove ads.

Another user said, “Fire Enrique and Jamie miller,” referring to the company’s CEO and CFO.

A third user said, “Have fun losing while the market makes new ath again.”

Advertisement|Remove ads.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_499669876_jpg_86c4dfd07c.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_6979_jpg_a2a1032fdc.webp) Ahmed Farhath·9m ago

Ahmed Farhath·9m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2285371071_jpg_fcacba42c4.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/Prabhjote_DP_67623a9828.jpg) Prabhjote Gill·9m ago

Prabhjote Gill·9m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2191588209_jpg_4bdcedf469.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·17m ago

Anushka Basu·17m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2195599761_jpg_ec0e618b8c.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·19m ago

Arnab Paul·19m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2274012713_jpg_b438f6a2bc.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·24m ago

Rounak Jain·24m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2204272021_jpg_74c54b89de.webp) Prabhjote Gill·41m ago

Prabhjote Gill·41m ago