Advertisement|Remove ads.

This Small-Cap Fintech Stock Is Crushing PayPal, SoFi, Klarna In 2026: Analyst Says Rally Isn't Over Yet

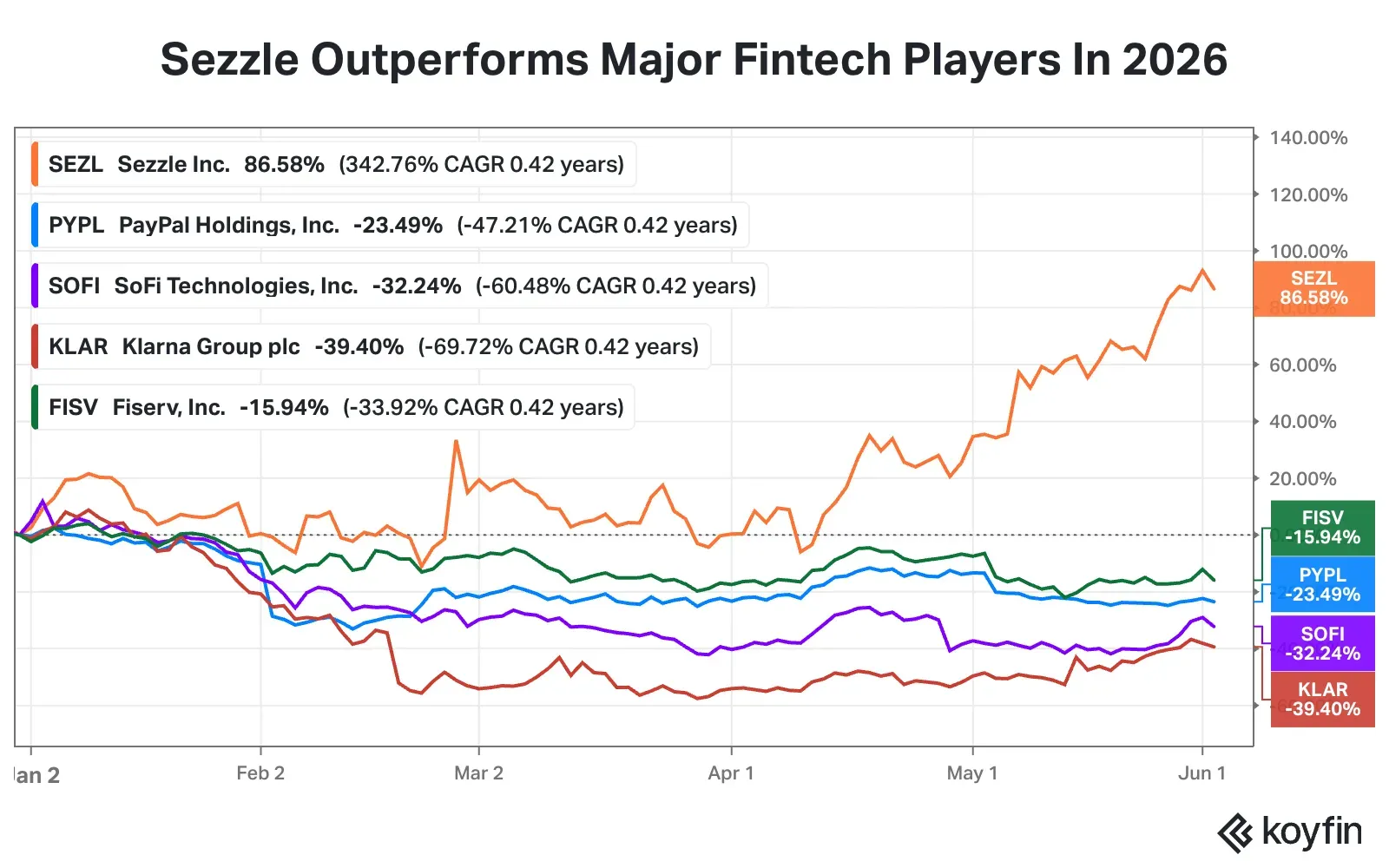

- SEZL stock has surged more than 86% in 2026, while larger fintech companies such as PayPal, SoFi Technologies, Klarna, and Fiserv have declined.

- Buckley Capital Advisors has said it believes Sezzle is a high-growth buy-now-pay-later platform that is mispriced relative to its earnings power and growth trajectory.

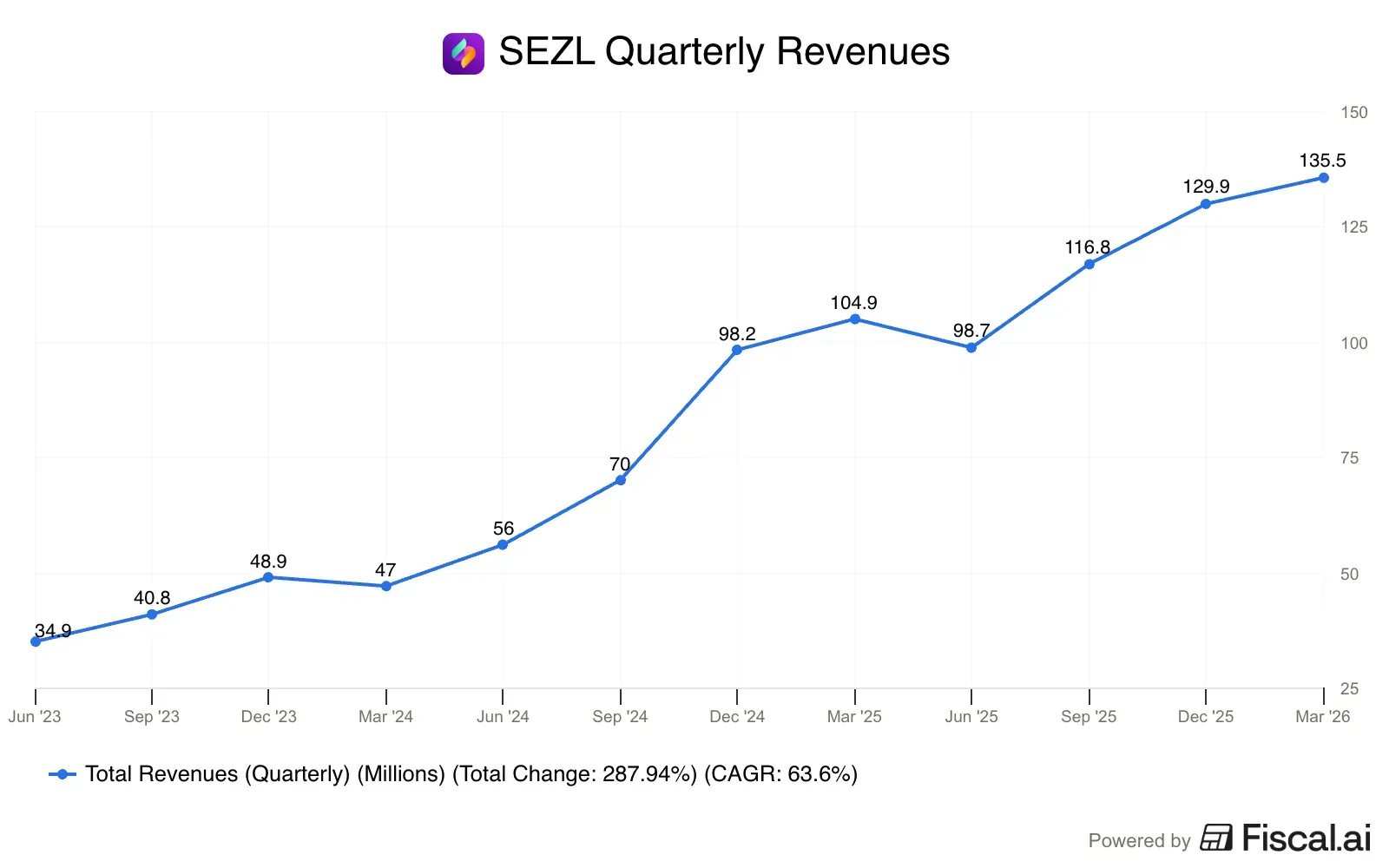

- Last month, Sezzle reported a 29% growth in Q1 revenue to $135.5 million and a 41.9% increase in net income.

Advertisement|Remove ads.

Sezzle Inc. (SEZL) has emerged as one of the standout performers in the fintech space this year, with shares of the company surging more than 86% and significantly outpacing larger peers such as PayPal Holdings (PYPL), SoFi Technologies (SOFI), Klarna Group (KLAR), and Fiserv, Inc. (FISV).

Despite the massive uptick, Wall Street analysts believe that the Buy Now, Pay Later firm still has room to rally.

Most recently, B. Riley raised the price target on Sezzle to $141 from $117 and maintained a ‘Buy’ rating on the shares, implying an upside potential of more than 19% from its last close.

Advertisement|Remove ads.

What Is Wall Street Saying About Sezzle?

B. Riley has highlighted Sezzle’s integration with Knot's CardSwitcher API, which will enable automatic updates of Sezzle virtual cards as the preferred payment method across merchants such as Amazon, Walmart, and Uber. This will likely improve checkout convenience and help drive top-of-wallet behavior among users, the analyst said.

As per the analyst, this move alone will align Sezzle with similar integrations already seen at companies like American Express (AXP) and PayPal.

Meanwhile, Buckley Capital Advisors, an investment management company, said in its first quarter 2026 investor letter that Sezzle is “a high-growth buy now pay later platform that we believe is mispriced relative to its earnings power and growth trajectory.”

Advertisement|Remove ads.

Sezzle trades at approximately 21.8x its forward earnings, according to Koyfin data, compared to PayPal at 8.2x and Fiserv at 6.9x.

“The BNPL space is growing at 20% per year, and SEZL has the best business model within the industry. While its stock is highly sensitive to market perceptions around consumer credit, given how quickly the company’s book turns over, it can easily pull back on credit or tighten its lending standards and see meaningful improvements in credit performance,” Buckley Capital said in the letter.

“This makes Sezzle a much lower-risk business model from a credit standpoint than its stock volatility would imply, and a very high-quality business given how quickly it is able to grow and the growth runway ahead of it,” it added.

Advertisement|Remove ads.

SEZL Earnings Snapshot

Last month, Sezzle reported first-quarter (Q1) earnings results, posting a 29% growth in total revenue to $135.5 million.

The company’s net income also increased 41.9% to $51.3 million for the quarter. Sezzle’s gross merchandise volume (GMV) for Q1 increased 37.3% year-on-year to $1.1 billion, active transacting consumers grew 13.6% to about 3.1 million, and average purchase frequency reached a quarterly record of 7.1x in the quarter, up from 6.1x in the same period of last year, indicating that existing users are transacting more frequently within the ecosystem.

The company also hiked its full-year 2026 guidance across all metrics: forecasting total revenue growth of up to 35% from 25% to 30%, and adjusted net income to $180 million, up from $170 million, among others.

Advertisement|Remove ads.

Meanwhile, Buckley Capital believes the company is likely to surpass guidance, telling investors that it believes “the company is being very conservative with its financial guidance and is likely to exceed consensus expectations.”

SEZL Vs Other Fintech Firms

Sezzle is one of the best-performing fintech stocks this year, having surged more than 86%. In comparison, PYPL, SOFI, KLAR, and FISV have all declined so far in 2026.

On Stocktwits, retail sentiment around SEZL shares declined from ‘neutral’ to ‘bearish’ territory over the past 24 hours. FISV stock was also in the ‘bearish’ territory at the time of writing.

Advertisement|Remove ads.

Meanwhile, retail sentiment on SOFI and PYPL was ‘extremely bullish’ and ‘bullish’ respectively, while it was ‘neutral’ for KLAR.

One user who is bullish on SEZL said, “we can have a red day it's ok! Biggest mistake would be selling before it's explode! 180 $ is coming!”

Advertisement|Remove ads.

SEZL stock has clocked five consecutive weeks in the green and surged more than 48% in May alone.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2222921905_jpg_63b8dc6cd7.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Prabhjote_DP_67623a9828.jpg) Prabhjote Gill·10m ago

Prabhjote Gill·10m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1307216100_jpg_3f3e6f9ccd.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·14m ago

Rounak Jain·14m ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2250240969_jpg_dd9be8c5ea.webp) Rounak Jain·49m ago

Rounak Jain·49m ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_1238344097_jpg_8e929809b1.webp) Prabhjote Gill·52m ago

Prabhjote Gill·52m ago/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/Celsius_Holdings_energy_drinks_07c24a37ad.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·2h ago

Arnab Paul·2h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2287813772_c9b550d3a1.jpg) Prabhjote Gill·2h ago

Prabhjote Gill·2h ago