Advertisement|Remove ads.

Cisco Analysts Brace For Q1 Beat As Spending Environment Improves: Retail Mood Buoyant

Networking giant Cisco Systems, Inc. ($CSCO) is scheduled to report its fiscal 2025 first-quarter results after the market closes on Wednesday.

Analysts, on average, expect the San Jose, California-based company to report non-GAAP earnings per share (EPS) $0.87 and revenue of $13.78 billion. This marks a decline from the year-ago quarter’s $1.11 and $14.7 billion, respectively

Morgan Stanley analyst Meta Marshall expects a small top-line beat as results from peers and checks show a gradual improvement in spend environment amid dissipation in “inventory digestion” headwinds

Advertisement|Remove ads.

The analyst predicts that Cisco stock will move higher following the print, catalyzed by strong orders. She models a 30% year-over-year (YoY) increase in organic orders.

But Splunk synergies or networking pull-through from a stronger security portfolio would be needed for meaningful upside, the analyst said.

Cisco completed its $28 billion all-cash acquisition of data analytics and intelligence software company Splunk in mid-March.

Advertisement|Remove ads.

Marshall expects upside relative to EPS expectations due to RIG/Splunk synergies.

Morgan Stanley has an “Overweight” rating and $58 price target for Cisco shares.

On Tuesday, JP Morgan analyst Samik Chatterjee upgraded Cisco shares from “Neutral” to “Overweight” and upped the price target from $55 to $66. The analyst premised his optimism on the recovery cycle in enterprise networking demand, the recent investment in the security segment and the stock trading off its peak valuation multiple.

Advertisement|Remove ads.

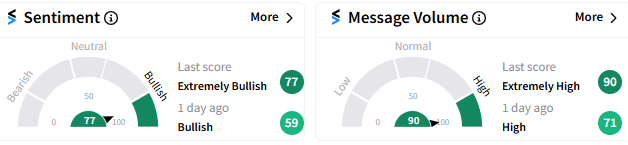

Retail mood is “extremely bullish” (77/100) on Stocktwits platform, with message volume spiking to “extremely” high.

As of 11:50 am ET, Cisco shares edged up 0.09% to $58.76.

Advertisement|Remove ads.

For updates and corrections email newsroom@stocktwits.com

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Traders_at_New_York_Stock_Exchange_c86a5c6148.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Whats_App_Image_2026_05_11_at_09_45_43_1_jpeg_a08c0cf251.webp) Aveek Bhowmik·19m ago

Aveek Bhowmik·19m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_BE_Bloom_faee9b1d61.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·23m ago

Shashank Nayar·23m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_corcept_therapeutics_jpg_0778e9d4e5.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·28m ago

Arnab Paul·28m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2227347466_jpg_9056eff14e.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·30m ago

Anan Ashraf·30m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2285371071_jpg_fcacba42c4.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·41m ago

Rounak Jain·41m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_viking_jpg_7a4076836e.webp) Arnab Paul·1h ago

Arnab Paul·1h ago