Advertisement|Remove ads.

El-Erian Says Softer CPI Print Should Help 'Temper' Hawkish Tilt As Markets Rethink Fed Path

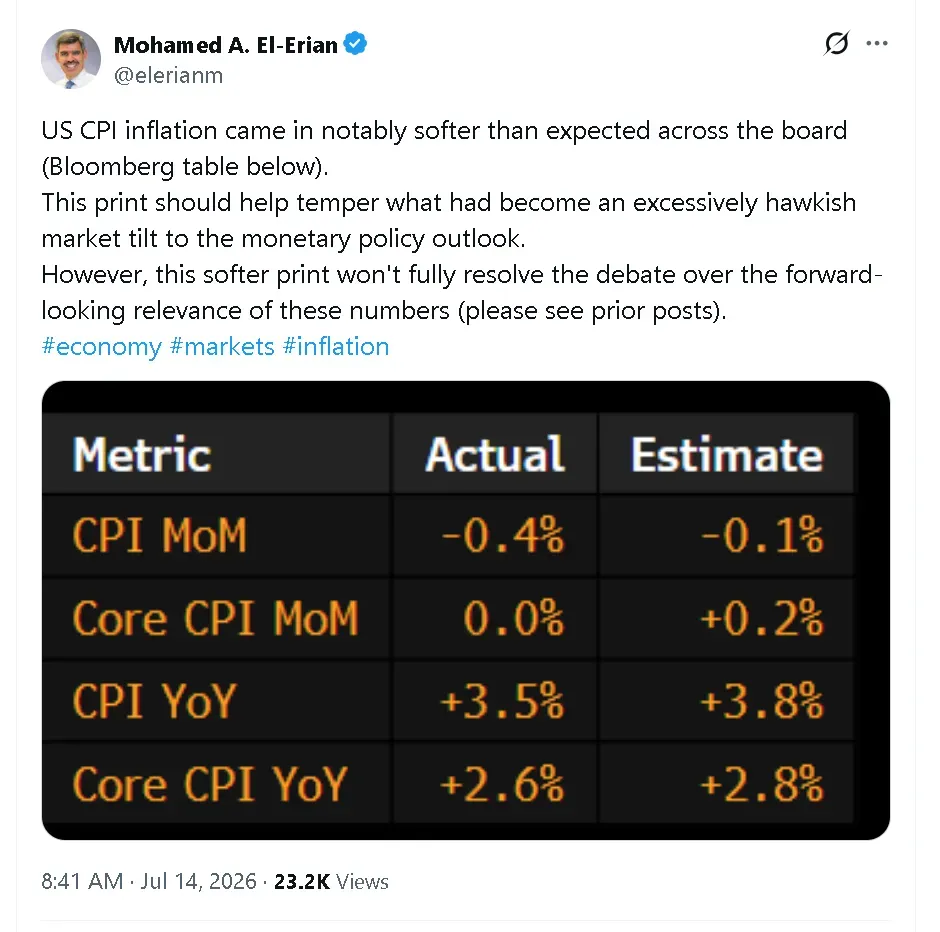

- June CPI rose 3.5% year over year while core inflation increased 2.6%, and consumer prices fell 0.4% from the previous month, marking the largest monthly decline since May 2020.

- U.S. stocks and gold moved higher following the inflation report, with the Nasdaq-100 outperforming the broader market.

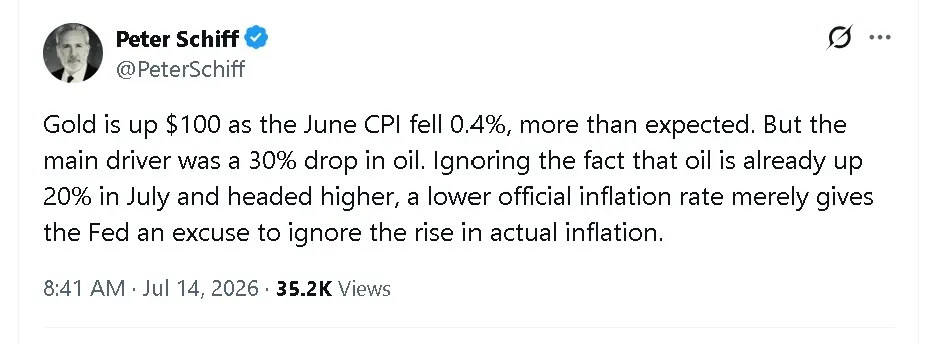

- Peter Schiff stated that the decline in inflation was driven largely by falling oil prices and warned that renewed increases in energy costs could push inflation higher again.

Advertisement|Remove ads.

Mohamed El-Erian, Chief Economic Advisor at Allianz, said on Tuesday that the softer-than-expected June Consumer Price Index (CPI) reading should help “temper” what had become a “hawkish market tilt” toward monetary policy.

The Consumer Price Index rose 3.5% from a year earlier in June, below expectations, while core CPI came in at 2.6%. On a monthly basis, prices fell 0.4%, the sharpest decline since May 2020.

“This print should help temper what had become an excessively hawkish market tilt to the monetary policy outlook,” El-Erian said in a post on X. “However, this softer print won't fully resolve the debate over the forward-looking relevance of these numbers.”

Advertisement|Remove ads.

The overall market trended higher on Monday morning. The SPDR S&P 500 ETF (SPY) was up 0.26%, the SPDR Dow Jones Industrial Average ETF (DIA) gained 0.12%, and the Nasdaq-100 tracking Invesco QQQ Trust (QQQ) rose over 1%. Retail sentiment around QQQ on Stocktwits continued to trend in ‘bullish’ territory over the past day, accompanied by chatter at ‘normal’ levels.

Peter Schiff Agrees Inflation Pressures Remain

Gold prices also rose, with the SPDR Gold Shares ETF (GLD) up nearly 2% in morning trade. Retail sentiment around the ETF remained in ‘neutral’ territory over the past day, with chatter at ‘normal’ levels.

Gold bull and cryptocurrency critic Peter Schiff took a different approach from El-Erian, but agreed that inflation pressures remain. In a post on X, he stated that gold rose because the CPI fell 0.4% and that the main driver was a 30% drop in oil. He added that oil already rose again in July, warning that a lower official inflation rate could give “the Fed an excuse to ignore the rise in actual inflation.”

Advertisement|Remove ads.

Retail traders on Stocktwits were split between some being surprised that the market didn’t see more of a rally, while others noted that the CPI print was still above the Federal Reserve’s intended target of 2%.

Advertisement|Remove ads.

The CME Fed Watch Tool showed that the market is pricing in no rate cut at the July Federal Open Market Committee (FOMC) meeting, while September odds have eased to roughly 50/50 after the softer CPI print. Before the release, markets were pricing in about a 76% probability of a September hike.

For updates and corrections, email newsroom[at]stocktwits[dot]com

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_lucid_jpg_96d120e028.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·54m ago

Anan Ashraf·54m ago/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·1h ago

Shashank Nayar·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2261647056_jpg_19488f4a48.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Whats_App_Image_2026_05_11_at_09_45_43_1_jpeg_a08c0cf251.webp) Aveek Bhowmik·1h ago

Aveek Bhowmik·1h ago/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/large_biogen_fda_resized_3ea96b95df.jpg) Anan Ashraf·2h ago

Anan Ashraf·2h ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2231800416_jpg_1dc0b4f662.webp) Shashank Nayar·2h ago

Shashank Nayar·2h ago/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/large_fuelcellenergy_resized_ef1a57cfe6.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_6979_jpg_a2a1032fdc.webp) Ahmed Farhath·2h ago

Ahmed Farhath·2h ago