Advertisement|Remove ads.

From $100K Loss Per Car To Cosmos — Lucid’s High-Stakes Bet On Cheaper EVs

- LCID stock gained about 33% this week after it dismissed rumors of an impending bankruptcy filing or take-price deal earlier this week.

- Lucid incurred a gross loss of around $100,800 per vehicle delivered in Q1.

- The company is looking forward to launching its Cosmos vehicle later this year.

Advertisement|Remove ads.

Shares of EV maker Lucid Motors (LCID) clocked their best week in a year after the company reiterated its liquidity will last well into 2027, and dismissed rumors that a bankruptcy filing is up the alley.

LCID stock gained about 33% this week, thanks to a steady three-day rally until Friday.

How Much Cash Is Lucid Really Burning?

According to data from the company’s last earnings report, Lucid had total cash, cash equivalents and restricted cash of $765.7 million as of March 31. Total liquidity, including undrawn credit facilities and investments, amounted to around $3.2 billion. After capital raising actions in April, the company pegged this at around $4.7 billion.

Advertisement|Remove ads.

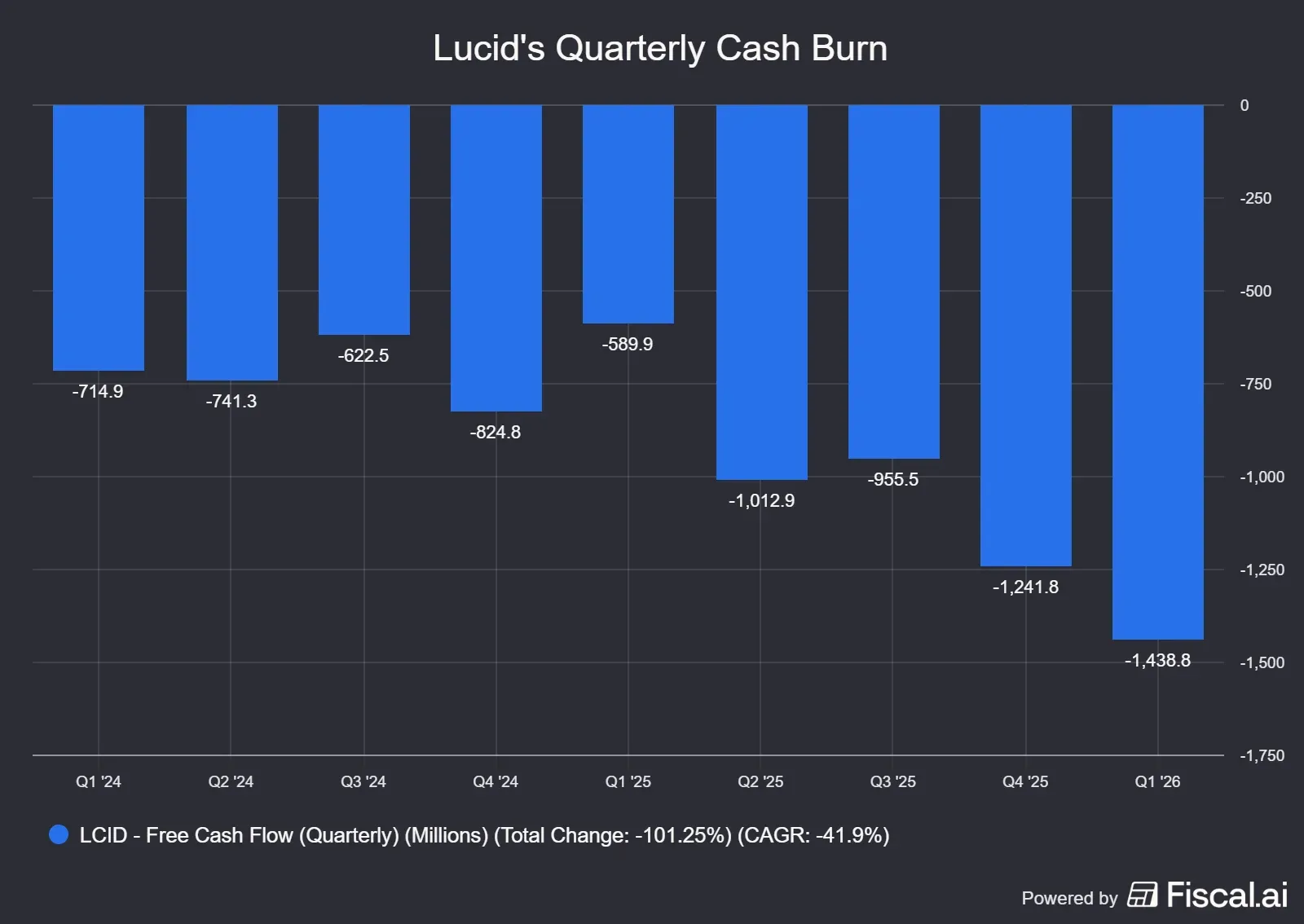

Despite its strong balance sheet, Lucid is also burning cash at a phenomenal rate. In the quarter ended March, the company reported total cash burn of $1.439 billion, much higher than the $590 million burn in the corresponding quarter of 2025.

The higher cash burn was aggravated by a higher inventory buildup and manufacturing issues, which stopped the company from delivering its vehicles for a few days in the quarter. The company is also looking to introduce three new consumer vehicle models based on its mid-size platform, implying significant additional investments into its research and development efforts.

If one were to assume a similar cash burn in the remaining quarters of this year, Lucid would still run out by 2027.

Advertisement|Remove ads.

Are LCID’s Backers A Safety Net?

Lucid, unlike many of its less fortunate predecessors, such as Nikola and Lordstown, which filed for bankruptcy, has a big backer. It is majority owned by Saudi PIF, which many, including rival firm Tesla’s (TSLA) CEO Elon Musk, have previously predicted will save the company by taking it private.

Lucid, however, is optimistic that higher delivery numbers will help it eventually bring down losses. It is one of the reasons that the company has planned three vehicles based on its mid-size platform. Current Lucid vehicles in production, both the Air sedan and the Gravity SUV, cater to a more premium consumer base.

Advertisement|Remove ads.

Lucid has previously said they are targeting a starting price below $50,000 for the mid-size model. The first mid-size model, called Cosmos, is slated to be launched later this year. The Earth would follow a year later.

However, it is unclear as to how many mid-size vehicles the company intends to deliver this year, after the company has suspended its overall 2026 guidance. Historically, initial volumes have usually been small for EV makers as they ramp production and ease creases in their supply chain. Lucid continues to face challenges scaling production of the Gravity SUV, with repeated supplier issues, supply chain bottlenecks, and slower-than-expected ramp-up rates, despite starting its production in late 2024.

In addition to PIF, Lucid also counts ride-hailing platform Uber Technologies (UBER) among its shareholders after the company invested $300 million into it last year. Earlier this year, Uber added another $200 million.

Advertisement|Remove ads.

Lucid’s Loss Accumulation So Far

As of the end of the first quarter, Lucid delivered 3,093 vehicles and incurred a gross loss of $311.7 million. This implies that the company incurred a gross loss of around $100,800 per vehicle delivered.

This means that for every Air sedan or Gravity SUV it sold, Lucid incurred a loss close to the sticker price.

Lucid’s Model Y Moment?

Lucid is envisioning a Tesla-like growth story. Launch with a premium vehicle, and eventually start making a mass market vehicle, which can push volumes and profitability.

Advertisement|Remove ads.

And if one were to go with Tesla’s timeline of achieving its first profitable quarter in five years of delivering its first vehicle, the clock is ticking for Lucid, which delivered its first vehicle in late 2021. Lucid is yet to report a quarterly profit.

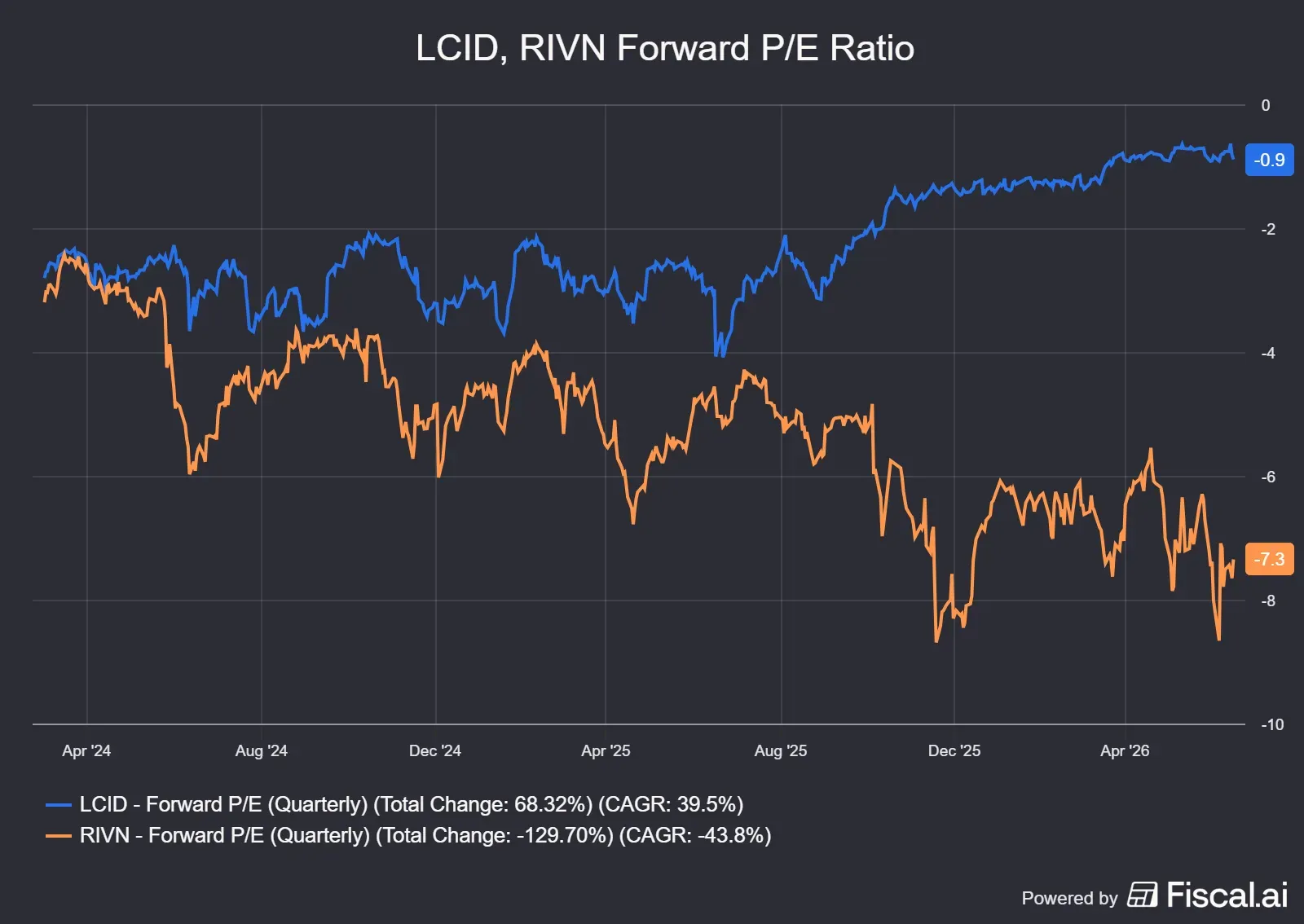

Lucid is not alone in hoping for a small, cheaper vehicle to revive its growth trajectory. Its rival Rivian Automotive (RVN) has already launched a cheaper SUV called the R2, and is trying to ramp up production numbers. However, a look at the two companies’ forward profit-to-earnings ratio shows that the market is pricing Lucid as significantly less unprofitable going forward, as compared to Rivian.

Advertisement|Remove ads.

In a positive for Lucid, Uber has already inked a deal to take several of their mid-size vehicles and deploy them as robotaxis, powered by tech from California startup Nuro Inc. While Uber has committed to deploying at least 35,000 Lucid vehicles as robotaxis, the ratio between Gravity and the newer models is unclear. The first robotaxis under the deal are expected to hit the road in the Bay Area later this year.

Wall Street Weighs In

Morgan Stanley analyst Andrew Percoco believes Lucid's new management team is "keenly focused" on strengthening the business and reducing cash burn as it readies for the mid-size launch. He forecast Lucid issuing $2 billion of equity and $500 million of debt in 2027, increasing potential dilution risk. The firm has an ‘Underweight’ rating and $5 price target on Lucid shares, as per TheFly.

Lucid CEO Silvio Napoli, who joined the company in June, said in a post on LinkedIn earlier this week that the company is working to improve operational performance and execution and that he is focused on turning the company around.

Advertisement|Remove ads.

To that end, the company announced an 18% cut to its U.S. workforce last month. The move impacted nearly 1500 employees, including full-time staff, contractors, and hourly manufacturing workers. The company also eliminated a second production shift at its Arizona factory in a bid to save cash and carried out a leadership overhaul that included the removal of the role of Chief Operating Officer and a new CFO.

How Did LCID Retail Traders React?

On Stocktwits, retail sentiment around LCID stock was ‘extremely bullish’ at the time of writing. Platform data showed an 587.5% increase in chatter over the last seven days.

Advertisement|Remove ads.

LCID stock gained 14% on Friday. The shares have dropped 30% year-to-date and nearly 76% in the past 12 months.

Read More: CELH Stock Clocks Second Consecutive Week Of Losses Amid UK Ban Concerns, Analyst Price Target Cuts

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/large_Stock_trading_4d940a6373.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·33m agoArnab Paul·42m ago

Arnab Paul·33m agoArnab Paul·42m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2280120668_jpg_fa8f332632.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·55m ago

Shashank Nayar·55m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_TMUS_jpg_ac08226907.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Whats_App_Image_2026_05_11_at_09_45_43_1_jpeg_a08c0cf251.webp) Aveek Bhowmik·1h ago

Aveek Bhowmik·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2222819201_jpg_edcbb1336e.webp) Shashank Nayar·1h ago

Shashank Nayar·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/gettyimages_1145334043_612x612_19c5d6bffe.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·2h ago

Rounak Jain·2h ago