Advertisement|Remove ads.

LULU Stock Plunges Overnight: Brand Backlash And Product Misfires Cast Shadow Ahead Of New CEO’s Arrival

- Co-CEO Meghan Frank said Lululemon's slowdown was driven by negative media and social media commentary that hurt customer traffic.

- Analyst Dana Telsey said the new CEO would face demand, product, and brand challenges, with recovery likely taking several quarters.

- Lululemon has faced criticism over its product innovation and growing competition from cheaper rivals.

Advertisement|Remove ads.

Lululemon Athletica (LULU) stock plunged over 11% overnight on Thursday, as the company cited softer business conditions heading into the fiscal second quarter (Q2), referring to weaker customer engagement and uneven product performance despite a good start to the year.

The athletic apparel retailer expects Q2 revenue to be between $2.45 billion and $2.48 billion, which would be 2% to 3% lower than a year ago. The company also forecasts earnings of $1.76 to $1.81 per share.

For the full year 2026, Lululemon lowered its outlook, now expecting revenue of $11.0 billion to $11.15 billion, down from its earlier forecast of $11.35 billion to $11.5 billion.

Advertisement|Remove ads.

Negative Brand Buzz And Weak Product Launches Weigh On LULU’s Growth

Speaking on the first-quarter (Q1) earnings call, interim co-CEO and CFO Meghan Frank said Lululemon saw positive indicators throughout much of the quarter but faced new challenges as Q1 ended and Q2 began.

Frank said the company identified two primary factors behind the recent slowdown.

“First, we experienced spikes of negative commentary in the media and on social channels with regard to our brand, which had an impact on traffic and overall top line performance. And second, not all of our product launches have met our expectations,” said Frank.

Advertisement|Remove ads.

She specifically highlighted a new yoga apparel collection that was well received by customers, but it did not lead to stronger sales and added that Lululemon remains confident in its upcoming product lineup.

"These styles were met with good guest response, but so far, the campaign hasn't had the expected halo effect on other areas of our assortment," Frank said. "Over the course of the year, we'll continue to bring newness, excitement and new fabrics into the assortment with focus areas including outerwear and lounge.”

Frank indicated that the updated forecast reflects both the traffic-related weakness and the disappointing response to select merchandise launches.

Advertisement|Remove ads.

Analyst Expects Additional Weakness for LULU

Retail analyst Dana Telsey of Telsey Advisory Group argued that the company's turnaround remains in its early stages. She suggested Lululemon could face deeper discounting activity and said U.S. sales may decline by double-digit percentages in the coming quarter.

“There’s more markdowns ahead of us to take and some of the new products haven’t really resonated. So there’s work to be done,” Telsey said in a CNBC interview.

Telsey noted that incoming CEO Heidi O'Neill will inherit a business dealing with several simultaneous challenges, including softer demand, recent negative publicity and merchandise that has not consistently resonated with shoppers. She estimated investors may need to wait three to four quarters before signs of stabilization become visible.

Advertisement|Remove ads.

Heidi O'Neill, a Nike veteran, will take charge as Lululemon’s CEO in September. The company faced criticism from founder Chip Wilson, who lambasted the board for making the wrong choice for CEO.

The tug-of-war between Wilson and the board continued until a truce was reached in late May.

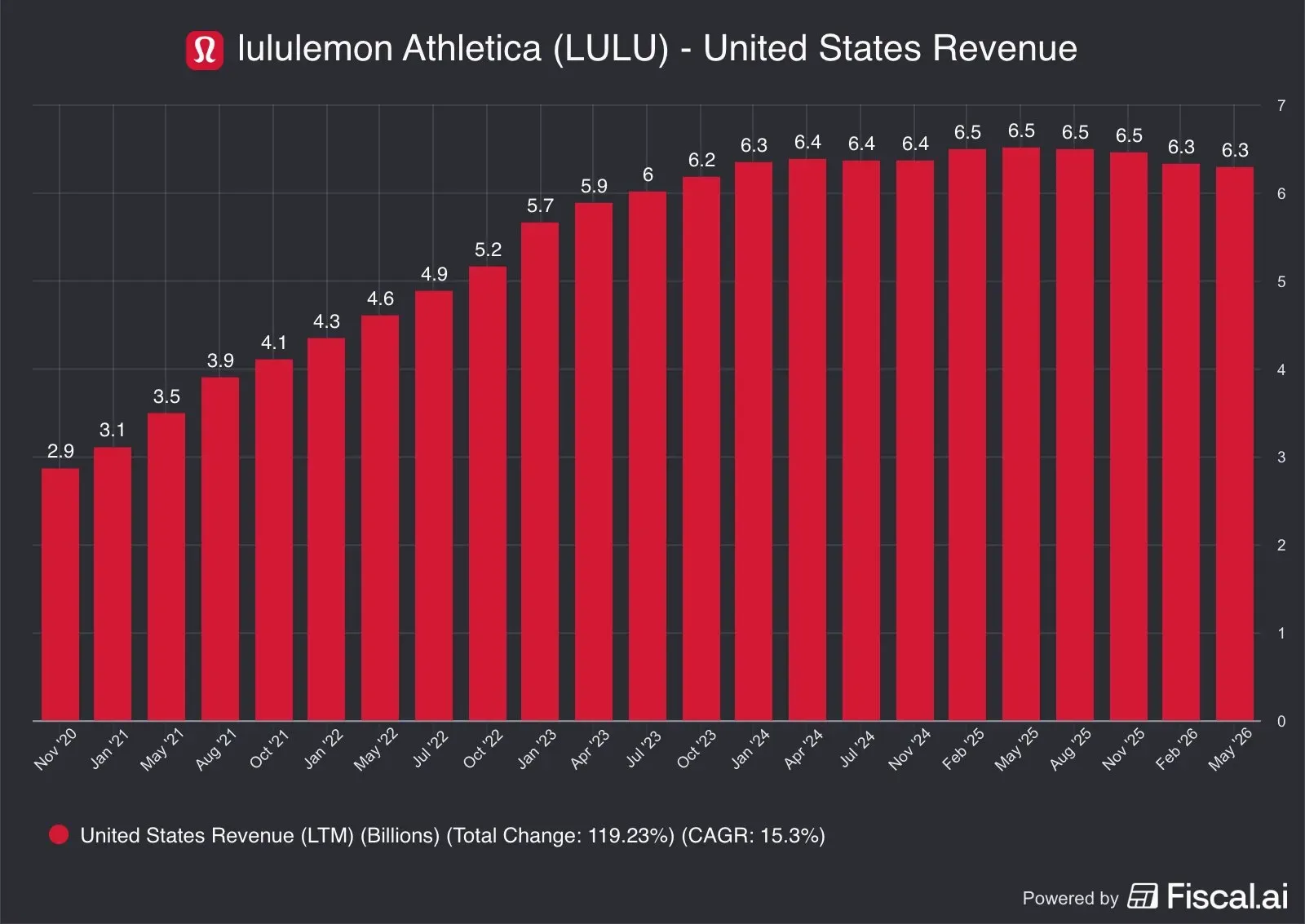

LULU’s Growth Concerns

Data from Fiscal AI highlights why investors are concerned. Lululemon’s U.S. revenue grew from about $2.9 billion in 2020 to $6.5 billion by 2025, but growth has recently stalled, and revenue has fallen slightly to around $6.3 billion.

Advertisement|Remove ads.

The athleisure brand has faced criticism for its product innovation and for increasing competition from lower-priced alternatives. LULU shares have lost more than 60% over the last 12 months.

However, investor Michael Burry, best known for anticipating the housing-market collapse portrayed in "The Big Short," disclosed ahead of earnings that he added to his Lululemon position. Burry wrote in a Substack post that he purchased additional shares at $129.44.

LULU Retail Traders View

On Stocktwits, retail sentiment around the stock turned to ‘extremely bullish’ from ‘bullish’ territory the previous day, with over 1,300% surge in message volume in 24 hours.

Advertisement|Remove ads.

A user said, “drama with founder has killed the stock- founder just thinks about his intrests than investors and what sort of impression going to market with this pathetic cat fight.”

Another user said, “Revenue is still increasing, so not all that bad.”

LULU stock has plunged nearly 40% year-to-date.

Advertisement|Remove ads.

Also See: Why Did STI, BB, CSCO Stocks Surge To 52-Week Highs Today?

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2259521351_jpg_932f293a89.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/shivani_photo_jpg_dd6e01afa4.webp) Shivani Kumaresan·34m ago

Shivani Kumaresan·34m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Sound_Hound_jpg_7961ee756a.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_8805_JPG_6768aaedc3.webp) Deepti Sri·38m ago

Deepti Sri·38m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2259083983_bcdf18efc0.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_9209_1_d9c1acde92.jpeg) Yuvraj Malik·1h ago

Yuvraj Malik·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/Stocktoberfest_2026_8b30935c54.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/large_spacex_53269b0228.jpg) Deepti Sri·1h ago

Deepti Sri·1h ago/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/large_vecteezy_data_center_computers_large_facility_with_servers_storage_21993068_2bc22427bf.jpg) Shivani Kumaresan·2h ago

Shivani Kumaresan·2h ago