Advertisement|Remove ads.

Pagaya’s Retail Traders Brace For Q3 Results As Short Interest Surges To Record High — Fintech's Asset Quality In Focus

- Pagaya is expected to report fiscal year 2025 third-quarter adjusted earnings per share (EPS) of $0.21 and revenue of $338.35 million.

- A recent Moody’s report warned about the complexity of the company’s financial reporting.

- The stock has gained more than 145% this year.

Advertisement|Remove ads.

Pagaya Technologies Ltd. (PGY) shares elicited brisk retail chatter on Stocktwits early Monday as retail traders discussed the company’s quarterly results, which are due to be released before the market opens. The Israeli company, based in Tel Aviv and New York, is a fintech platform that focuses on subprime U.S. consumers, utilizing artificial intelligence (AI) technology to analyze loans.

Pagaya stock has gained more than 145% this year. In the overnight hours, the stock jumped over 7%, according to Yahoo Finance.

Retail Optimism Grows

Retail sentiment toward the small-cap Pagaya among users of the Stocktwits platform remained ‘neutral’ as of early Monday, and the message volume was also ‘normal.

Advertisement|Remove ads.

A bullish watcher said the Senate vote on the government shutdown could not have come at a better moment. The user predicted a short-squeeze if the earnings are good.

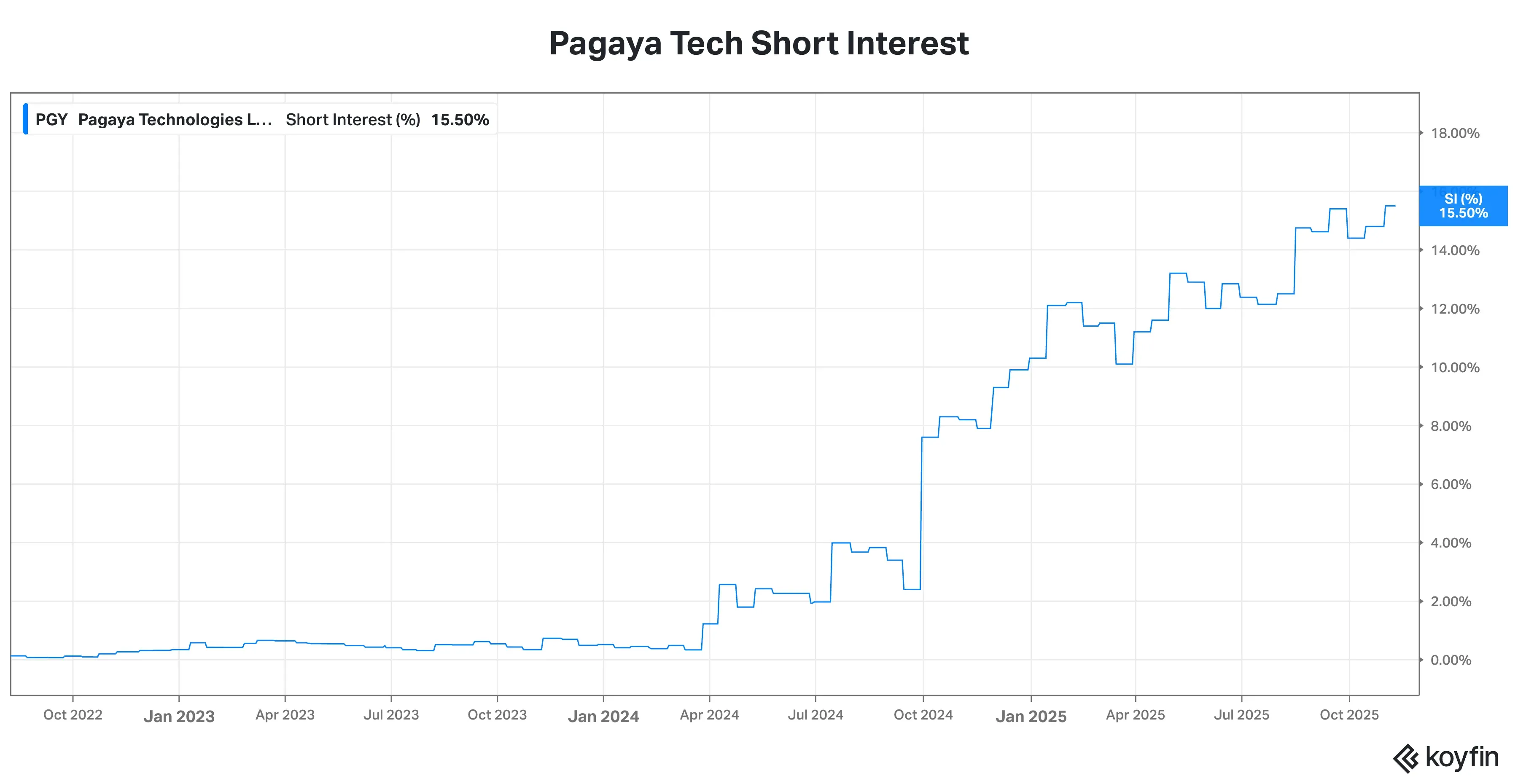

The short interest in the stock is at 15.50%, the highest on record. The company went public in June 2022 through a Special Purpose Acquisition Company (SPAC) route.

Advertisement|Remove ads.

Source: Koyfin

Source: Koyfin

Another user said they expected revenue to be normal but flagged write-offs and bad loans as the most important issue. “Analysts will be examining this closely,” they said.

Advertisement|Remove ads.

But some also have apprehensions about the valuation, with a user stating that the stock is still “too overpriced.”

What Analysts Expect From Pagaya's Q3

According to Stocktwits data, Pagaya is expected to report fiscal year 2025 third-quarter adjusted earnings per share (EPS) of $0.21 and revenue of $338.35 million. In early August, the company guided to third-quarter revenue of $330 million to $350 million.

Advertisement|Remove ads.

For the full year, the company expects revenue to be between $1.25 billion and $1.325 billion, and net income to be between $55 million and $75 million.

Earlier this month, Pagaya said it had clinched a new forward flow agreement with Castlelake, an alternative asset management firm specializing in asset-based private credit, for the purchase of up to $500 million of auto loans sourced through its platform. The company also announced several asset-backed securities (ABS) deals.

In early October, the company announced that it had expanded its revolving credit facility with top-tier banks, with the enhanced amount now at $132 million. The larger facility was negotiated with a 400-basis-point reduction in the interest rate.

Advertisement|Remove ads.

Asset Quality Under Scrutiny

A Bloomberg report said Pagaya’s ABS issuance faces its most significant test as U.S. consumers come under increasing strain. Despite management's assurance that it has tightened risk management, a recent Moody’s report warned about the complexity of the company’s financial reporting. The firm also flagged “a lack of reporting of securitization asset quality metrics such as problem loan and net charge-off ratios.”

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Oil_Iran_tensions_jpg_f34e3cef73.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·6m ago

Arnab Paul·6m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Circle_Internet_jpg_add0182c9c.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Prabhjote_DP_67623a9828.jpg) Prabhjote Gill·20m ago

Prabhjote Gill·20m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1401171512_7_jpg_ff7adea960.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_6979_jpg_a2a1032fdc.webp) Ahmed Farhath·35m ago

Ahmed Farhath·35m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_snap_resized_jpg_9672f61595.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_9209_1_d9c1acde92.jpeg) Yuvraj Malik·1h ago

Yuvraj Malik·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Snap_jpg_11a44b44a0.webp) Yuvraj Malik·1h ago

Yuvraj Malik·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_globalstar_jpg_ce94345876.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_8805_JPG_6768aaedc3.webp) Deepti Sri·2h ago

Deepti Sri·2h ago