Advertisement|Remove ads.

Dell Posts Record Q4 EPS On AI Server Boom, But Revenue Misses — Retail Cheers Dividend Hike, Valuation

Dell Technologies, Inc. (DELL) reported mixed results for the fourth quarter of the fiscal year 2025 and announced a dividend hike. The company also augmented its stock buyback authorization by $10 billion.

The fiscal year 2026 guidance was positive, but the first quarter outlook fell short of expectations.

The Round Rock, Texas-based company’s fourth-quarter non-GAAP earnings per share (EPS) climbed to a record $2.68 from $2.27 in 2024. Revenue increased 7% year over year (YoY) to $23.9 billion.

Advertisement|Remove ads.

The bottom line exceeded the consensus estimates of $2.52 and the guidance of $2.50, plus or minus $0.10, while the topline trailed the $24.57 billion-consensus estimate and the guidance of $24 billion to $25 billion.

CFO Yvonne McGill said, “FY25 was a transformative year – we hit $95.6 billion in revenue, grew our core business double digits, unlocked efficiencies, and drove record EPS.”

The Infrastructure Solution Group’s (ISG) revenue rose 22% YoY to $11.4 billion, with Servers and Networking revenue climbing 37% due to artificial intelligence (AI) and traditional server demand. Storage revenue increased a much more moderate 5% to $4.7 billion.

Advertisement|Remove ads.

The segment generated a record operating income of $2.1 billion, up a robust 44%.

COO Jeff Clarke said, “Our prospects for AI are strong, as we extend AI from the largest cloud service providers, into the enterprise at-scale, and out to the edge with the PC.”

“The deals we’ve booked with xAI and others puts our AI server backlog at roughly $9 billion as of today.”

Advertisement|Remove ads.

The growth of the Client Solutions Group (CSG) was an anemic 1% to $11.9 billion, with the 5% growth in commercial client revenue helping to offset a 12% decline in customer revenue. The segment's operating profit fell 19% to $631 million.

Dell raised its annual dividend by 18% to $2.10, with the first quarterly distribution of $0.525 payable on May 2 to shareholders of record as of April 22. The company’s board also approved a $10 billion increase to its share repurchase authorization.

Looking ahead, the company expects an adjusted EPS of $1.65 for the first quarter and $9.30 for the full year, compared to the consensus estimates of $1.83 and $9.29, respectively.

Advertisement|Remove ads.

It guided revenue for the quarter to be between $22.5 billion and $23.5 billion and for the year to be between $101 billion and $105 billion. Analysts, on average, estimate $23.72 billion and $103.62 billion, respectively.

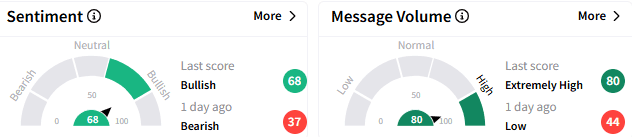

On Stocktwits, the retail sentiment toward the stock turned ‘bullish’ (68/100) from ‘bearish’ a day ago, and the message volume surged to ‘extremely high’ levels.

A retail watcher recommended buying the stock and predicted the stock would gain in Friday’s session due to the “fantastic” earnings results.

Advertisement|Remove ads.

Another user sees the stock as “attractively valued,” especially when weighed against the ‘magnificent’ earnings beat and the 18% dividend increase.

Advertisement|Remove ads.

Dell stock slipped 1.14% to $106.60 in the after-hours session. The stock has shed over 6% this year after a substantial 53% rally in 2024.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2227346980_jpg_6dab82ca22.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/shivani_photo_jpg_dd6e01afa4.webp) Shivani Kumaresan·8m ago

Shivani Kumaresan·8m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2258805990_jpg_bfe7a0fe9e.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_9209_1_d9c1acde92.jpeg) Yuvraj Malik·16m ago

Yuvraj Malik·16m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_space_stocks_jpg_dc40875420.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_8805_JPG_6768aaedc3.webp) Deepti Sri·18m ago

Deepti Sri·18m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_kevin_warsh_OG_2_jpg_3e8b6e9a47.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Aashika_Suresh_Profile_Picture_jpg_2acd6f446c.webp) Aashika Suresh·59m ago

Aashika Suresh·59m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2225995334_jpg_67de820c56.webp) Deepti Sri·1h ago

Deepti Sri·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2225143639_jpg_3c14ece7e4.webp) Shivani Kumaresan·1h ago

Shivani Kumaresan·1h ago