Advertisement|Remove ads.

Asana Stock Tumbles As Subpar Revenue Guidance, CEO Retirement Overshadow Upbeat Q4 – Retail Sentiment Plummets

Asana, Inc. (ASAN) shares tumbled in Tuesday’s premarket session as investors digested the enterprise work management platform provider’s subpar revenue guidance and a leadership transition. However, the company’s quarterly results exceeded the consensus estimates.

The San Francisco, California-based company announced that Dustin Moskovitz has informed the board of his intention to step down as CEO once a replacement is found and transition to the role of Chairman.

Separately, Asana reported break-even results on an adjusted basis for the fourth quarter of the fiscal year 2025 compared to an adjusted loss per share of $0.04 a year ago. The bottom-line result beat the consensus estimate for a loss of $0.01 per share.

Advertisement|Remove ads.

Revenue climbed 10% year over year (YoY) to $188.3 million, roughly in line with the average analysts’ estimate of $188.13 million.

While the bottom-line result exceeded the guidance, quarterly revenue was just shy of the $188.50 million estimated by the company.

CFO Sonalee Parekh said, “FY25 was a pivotal year for Asana, with stabilization across key metrics, our emergence as a multi-product company, achieving over 800 basis point improvement in Q4 non-GAAP operating margin and positive free cash flow for the full year—a major milestone on our path to sustained profitable growth.”

Advertisement|Remove ads.

Moskovitz noted that the early momentum with AI Studio exceeded expectations, with “strong early customer adoption across segments and geographies, rapidly growing credit usage and a multi-million dollar pipeline.

Among operational metrics, the annualized growth in the number of core customers (defined as ones spending $5,000 or more) was 11% YoY at 24,062, the same pace of growth as in the third quarter.

The number of customers spending $100,000 or more on an annualized basis was 726, up 20%, faster than the 18% growth in the third quarter.

Advertisement|Remove ads.

The dollar-based net retention rate was 96%, the same as in the previous quarter.

Parekh said the company’s efficiencies and productivity gains position it to achieve a 1,000-point improvement in non-GAAP operating margin in the fiscal year 2026. The company is also set to achieve non-GAAP profitability, beginning in the first quarter of the new fiscal year.

Asana expects first-quarter adjusted earnings per share (EPS) of $0.02 and revenue of $184.5 million to $186.5 million. Analysts, on average, estimate a loss of $0.01 and revenue of $190.69 million.

Advertisement|Remove ads.

It forecasts a 1%-2% non-GAAP operating margin.

For the fiscal year 2026, the company projected a non-GAAP EPS of $0.19-$0.20 versus the $0.01 per share loss estimated by analysts. It guided revenue to $782 million to $790 million, below the consensus estimate of $802.98 million.

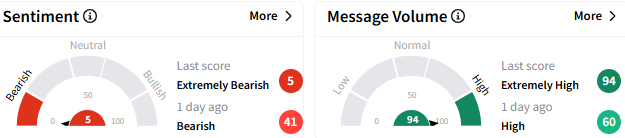

On Stocktwits, sentiment toward Asana stock worsened to ‘extremely bearish’ (5/100) from the ‘bearish’ mood that prevailed a day ago. Reflecting heightened trader chatter, the message volume spiked to ‘extremely high’ levels.

Advertisement|Remove ads.

A bearish watcher panned Asana for its inadequate cash reserves, liquidity issues, and loss-marking streak.

Another user lamented the slowdown in revenue growth from 13.88% last year to just 10%.

Advertisement|Remove ads.

In premarket trading, Asana stock plunged 27.46% to $12.10, heading toward the lowest level since Nov. 5. If the premarket losses are sustained, the stock is on track to record its biggest one-day loss ever. The stock has lost about 18% year-to-date

For updates and corrections email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1407197934_3a2e8235c9.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·8h ago

Anushka Basu·8h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2197413796_2ae5f600f7.jpg) Anushka Basu·9h ago

Anushka Basu·9h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2279969005_jpg_d203b64c52.webp) Anushka Basu·10h ago

Anushka Basu·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2244288176_jpg_c3909aa8e5.webp) Anushka Basu·10h ago

Anushka Basu·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2272863239_jpg_ed937b18d0.webp) Anushka Basu·12h ago

Anushka Basu·12h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_andre_francois_mckenzie_i_G_Yi_Bhd_N_Tp_E_unsplash_jpg_3d063f0b23.webp) Anushka Basu·14h ago

Anushka Basu·14h ago