Advertisement|Remove ads.

Bank of Baroda targets 11-13% credit growth led by retail, agriculture, and MSME segments

Debadatta Chand, Managing Director and CEO of Bank of Baroda, said that unless interest rates are cut, the bank has likely reached the lowest point in pricing for both deposits and loans.

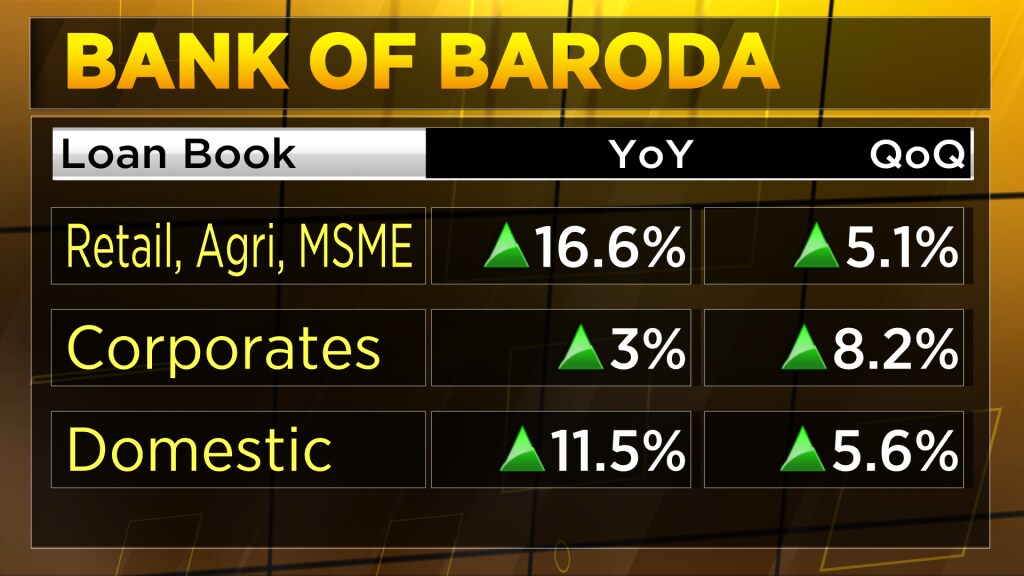

Bank of Baroda (BoB) is targeting a full-year credit growth of 11–13%, led by strong traction in its retail, agriculture, and MSME (RAM) segments, which are expected to expand over 15%, according to Managing Director and CEO Debadatta Chand.

The corporate book is projected to grow at a moderate 10–11% for the year, despite only 8% sequential growth in the second quarter. Chand said the bank remains cautious about aggressively pursuing low-margin corporate refinancing deals to preserve profitability.

The state-run lender delivered a resilient performance in its July-September quarter of 2025 (Q2FY26), with net interest margins (NIMs) expanding by five basis points to 2.96%, defying market expectations of a contraction. Chand attributed the strong showing to prudent liability management and a stable asset quality outlook.

Addressing the margin improvement, Chand acknowledged that an income tax refund contributed about 7–8 basis points to the NIMs but emphasised that the core performance was driven by strong net interest income (NII) growth and effective cost management. “The cost of deposit is at an all-time low at 4.91%,” he said, adding that the bank expects its full-year NIM to remain in the 2.85–3% range. “Assuming no rate cut and everything stands as it is, I think we have seen the lowest point in pricing, both on deposits and lending.”

On asset quality, Chand allayed concerns about potential stress in the micro, small & medium enterprises (MSME) and agriculture segments. Fresh slippages declined to ₹2,669 crore — lower than both the previous quarter and the same period last year. “The fresh slippage component-wise, both under retail and MSME, is lower than that of the last quarter,” he said, while a marginal uptick in agriculture slippages was not seen as worrisome. The bank maintained its slippage ratio guidance at 1% to 1.25% for the year.

Also Read: RBI reforms to boost Bank of Baroda’s credit growth, lending flexibility | Q&A with MD&CEO

Chand also discussed the impact of the Reserve Bank of India’s upcoming expected credit loss (ECL) provisioning norms, estimating that the change could temporarily lift credit costs by 20–25 basis points for about a year. However, he said the bank’s overall credit cost guidance of below 0.75% already factors in this impact. Recoveries from written-off accounts are expected to normalise at ₹700–₹750 crore per quarter.

He sees a growth opportunity in acquisition financing, following the RBI’s draft guidelines on external commercial borrowings (ECBs). With an international loan book of around ₹2.2 lakh crore and established experience in overseas markets, he believes Bank of Baroda is well-positioned to capitalise on this space. “As India becomes a more mature market, we need to have this product, and a bank like ours can play a significant role,” he said.

Bank of Baroda’s market capitalisation stands at about ₹1.51 lakh crore, with its shares gaining nearly 16% over the past year.

Also Read: Banks’ second quarter FY26 outlook: Loan growth steady, margins tighten

For the entire interview, watch the accompanying video

Catch all the latest updates from the stock market here

The corporate book is projected to grow at a moderate 10–11% for the year, despite only 8% sequential growth in the second quarter. Chand said the bank remains cautious about aggressively pursuing low-margin corporate refinancing deals to preserve profitability.

The state-run lender delivered a resilient performance in its July-September quarter of 2025 (Q2FY26), with net interest margins (NIMs) expanding by five basis points to 2.96%, defying market expectations of a contraction. Chand attributed the strong showing to prudent liability management and a stable asset quality outlook.

Addressing the margin improvement, Chand acknowledged that an income tax refund contributed about 7–8 basis points to the NIMs but emphasised that the core performance was driven by strong net interest income (NII) growth and effective cost management. “The cost of deposit is at an all-time low at 4.91%,” he said, adding that the bank expects its full-year NIM to remain in the 2.85–3% range. “Assuming no rate cut and everything stands as it is, I think we have seen the lowest point in pricing, both on deposits and lending.”

On asset quality, Chand allayed concerns about potential stress in the micro, small & medium enterprises (MSME) and agriculture segments. Fresh slippages declined to ₹2,669 crore — lower than both the previous quarter and the same period last year. “The fresh slippage component-wise, both under retail and MSME, is lower than that of the last quarter,” he said, while a marginal uptick in agriculture slippages was not seen as worrisome. The bank maintained its slippage ratio guidance at 1% to 1.25% for the year.

Also Read: RBI reforms to boost Bank of Baroda’s credit growth, lending flexibility | Q&A with MD&CEO

Chand also discussed the impact of the Reserve Bank of India’s upcoming expected credit loss (ECL) provisioning norms, estimating that the change could temporarily lift credit costs by 20–25 basis points for about a year. However, he said the bank’s overall credit cost guidance of below 0.75% already factors in this impact. Recoveries from written-off accounts are expected to normalise at ₹700–₹750 crore per quarter.

He sees a growth opportunity in acquisition financing, following the RBI’s draft guidelines on external commercial borrowings (ECBs). With an international loan book of around ₹2.2 lakh crore and established experience in overseas markets, he believes Bank of Baroda is well-positioned to capitalise on this space. “As India becomes a more mature market, we need to have this product, and a bank like ours can play a significant role,” he said.

Bank of Baroda’s market capitalisation stands at about ₹1.51 lakh crore, with its shares gaining nearly 16% over the past year.

Also Read: Banks’ second quarter FY26 outlook: Loan growth steady, margins tighten

For the entire interview, watch the accompanying video

Catch all the latest updates from the stock market here

Read about our editorial guidelines and ethics policy

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_bmnr_OG_jpg_83d4f3cc27.webp)

Why Did BMNR Stock Fall 7% Today?/filters:format(webp)https://news.stocktwits-cdn.com/shivani_photo_jpg_dd6e01afa4.webp) Shivani Kumaresan·6m ago

Shivani Kumaresan·6m ago

Shivani Kumaresan·6m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_uniqure_jpg_33b6552285.webp)

uniQure Stock Tumbled 55% Today: What’s The FDA Angle?/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·1h ago

Anan Ashraf·1h ago

Anan Ashraf·1h ago/filters:format(webp)https://images.cnbctv18.com/uploads/2025/10/shutterstock-2501739307-2025-10-861f01af47d926fe047e6d845acde591-scaled.jpg)

Foreign interest in Indian banks will continue, but expect a trickle, not a flood: Banking veterans/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/cnbctv18logo.png) CNBCTV18·50m ago

CNBCTV18·50m ago

CNBCTV18·50m ago/filters:format(webp)https://images.cnbctv18.com/uploads/2021/08/startup_funding1.jpg)

SalarySe raises $11.3 million Series A funds to expand financial solutions for India’s salaried workforceCNBCTV18·51m ago

CNBCTV18·51m ago/filters:format(webp)https://images.cnbctv18.com/uploads/2025/02/info-edge-2025-02-fe5e35de37c15a12e7140bf59ee0db52.jpeg)

Info Edge India to invest ₹100 crore in Redstart LabsCNBCTV18·1h ago

CNBCTV18·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2149589805_jpg_ceec7778b8.webp)

Adeia’s Stock Crashed 24% Today To Dip Below 200-DMA For First Time Since Early August: What’s Driving The Decline?/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·1h ago

Arnab Paul·1h ago

Arnab Paul·1h ago