Advertisement|Remove ads.

QCOM Still ‘Cheap AF,’ Says Citrini Research After Stock Surges On Q2 Delight

- The research firm also believes Qualcomm is undervalued, arguing that the company’s underperformance will fade amid rising demand for phones.

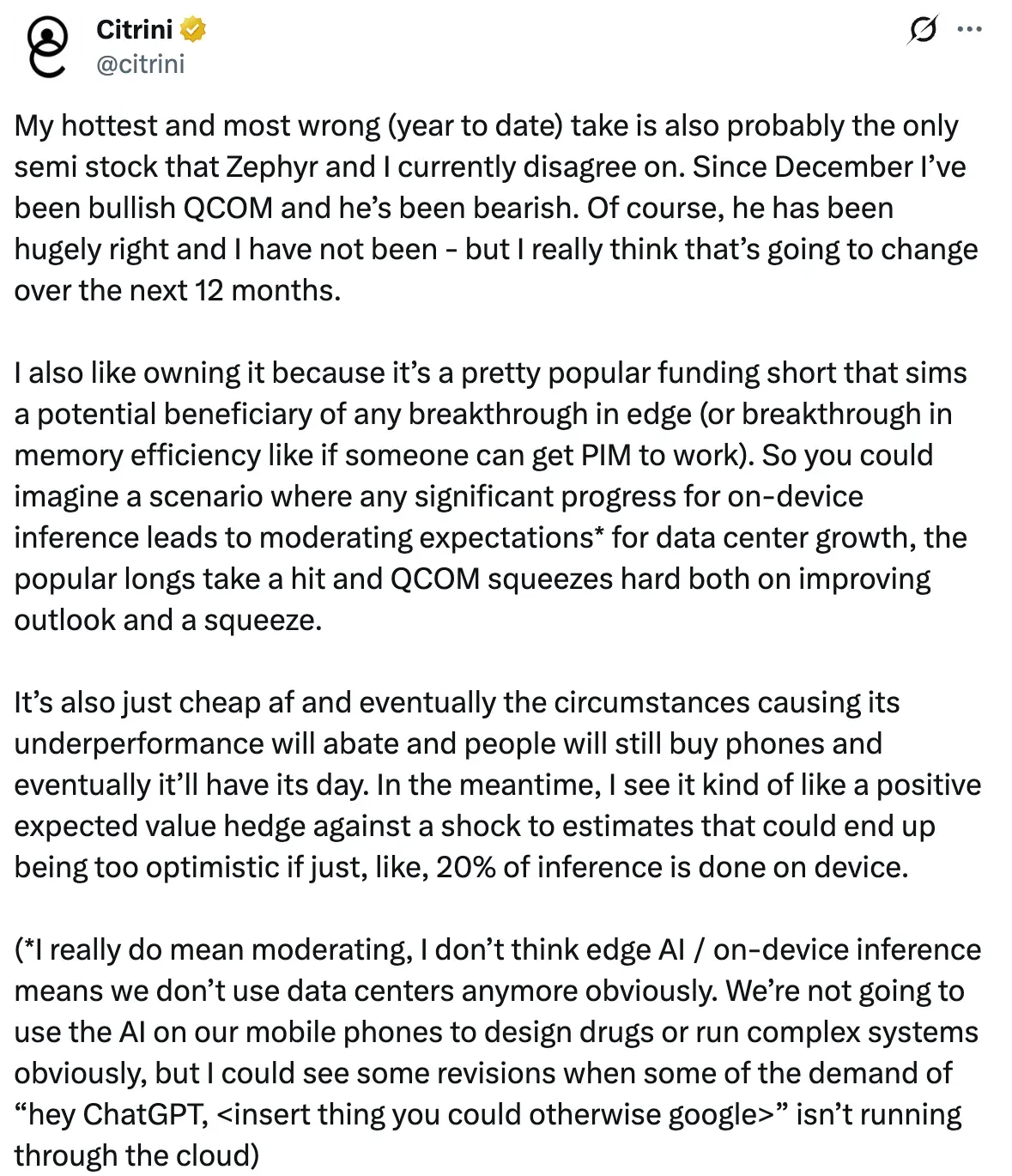

- Citrini Research added that Qualcomm is a popular short, but it still stands to benefit from breakthroughs in AI edge or memory efficiency.

- For the upcoming quarter, Qualcomm forecast adjusted profit of $2.10 to $2.30 per share, slightly below expectations.

Advertisement|Remove ads.

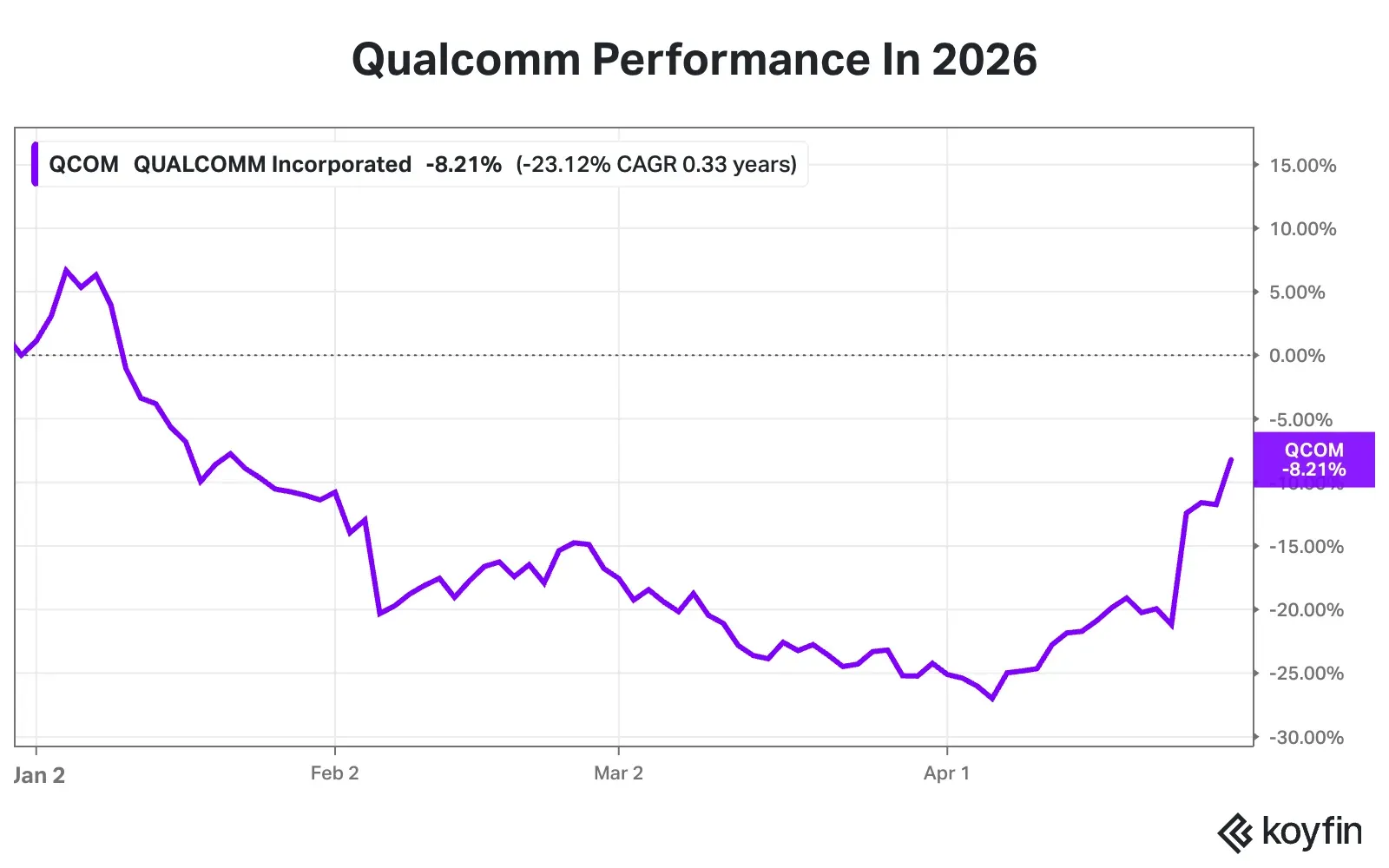

Shares of Qualcomm Inc. (QCOM) soared more than 13% in Wednesday’s overnight session, clawing back some of the year-to-date losses, after the chipmaker’s second-quarter (Q2) revenue and earnings beat market expectations.

QCOM shares were down nearly 10% this year before the surge in extended trading hours. Meanwhile, Citrini Research sees this downward trend reversing over the next 12 months.

The firm also believes Qualcomm is undervalued, arguing that the company’s underperformance will fade amid rising demand for phones. “It’s also just cheap af and eventually the circumstances causing its underperformance will abate and people will still buy phones and eventually it’ll have its day,” the investment research firm said in a post on X.

Advertisement|Remove ads.

Short interest in Qualcomm (QCOM) has risen steadily from 1.5% to 4.1% over the past year, according to Koyfin data. However, the stock remains relatively attractive on valuation, trading at a forward price-to-earnings ratio of about 15x, compared with roughly 50x for Advanced Micro Devices, Inc. (AMD) and 30x for Broadcom Inc. (AVGO).

QCOM’s Edge Case: Citrini Research

The New York-based firm said that Qualcomm is a popular “funding short” that still stands to benefit from breakthroughs in AI or memory efficiency.

“So you could imagine a scenario where any significant progress for on-device inference leads to moderating expectations* for data center growth, the popular longs take a hit and QCOM squeezes hard both on improving outlook and a squeeze,” the firm said, while also flagging that greater adoption of edge AI does not eliminate the need for data centers.

Advertisement|Remove ads.

Citrini also said that it sees Qualcomm as a positive-risk hedge against optimistic AI forecasts. “I see it kind of like a positive expected value hedge against a shock to estimates that could end up being too optimistic if just, like, 20% of inference is done on device,” it said.

Recent reports also suggest that Qualcomm is likely to power the next-gen AI smartphone for OpenAI. Taiwan-based market analyst Ming-Chi Kuo said earlier this week that the company would be developing the smartphone’s processors, with production expected in 2028.

QCOM’s Earnings Snapshot

In Q2, Qualcomm posted revenue of $10.6 billion, beating Wall Street expectations despite a year-on-year decline of about 3.6%. The company reported earnings of $2.65 a share, beating analyst estimates.

Advertisement|Remove ads.

For the upcoming quarter, Qualcomm forecast adjusted profit of $2.10 to $2.30 per share, below expectations of $2.43, according to data from Fiscal.ai. However, the company said it will start shipping chips to a large hyperscaler data center customer earlier than the fiscal 2027 timeline previously provided.

“We’re pursuing multiple opportunities with large hyperscalers, cloud service providers, sovereign AI projects, and other global partners,” said CEO Cristiano Amon. “Building on that momentum, we’re also entering the custom silicon space, beginning our ramp with a leading hyperscaler.”

Retail Stance On QCOM

On Stocktwits, retail sentiment around QCOM stock was in the ‘extremely bullish’ territory at the time of writing amid ‘extremely high’ message volumes.

Advertisement|Remove ads.

One bullish user said QCOM shares were still cheap. “From autonomous cars and robotics to military tech, smart glasses, and sports gear like ski gogles—the applications are endless. The time is now for edge devices,” the user said.

Another bullish user predicted that the company’s shares would reach $200 at the very least. QCOM shares were trading around $174.50 at the time of writing.

Advertisement|Remove ads.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2222341271_jpg_26b9066cf6.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Whats_App_Image_2026_05_11_at_09_45_43_1_jpeg_a08c0cf251.webp) Aveek Bhowmik·15h ago

Aveek Bhowmik·15h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_rivian_original_jpg_ac931d57b1.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·15h ago

Anan Ashraf·15h ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2257784104_jpg_4f7b38e8a2.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·16h ago

Shashank Nayar·16h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2281173544_jpg_d65fbb26dd.webp) Anan Ashraf·16h ago

Anan Ashraf·16h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2217651425_jpg_0d7dc8a6cd.webp) Shashank Nayar·16h ago

Shashank Nayar·16h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2263028790_jpg_bad9ec600a.webp) Aveek Bhowmik·17h ago

Aveek Bhowmik·17h ago