Advertisement|Remove ads.

Targa Reports Record Q4 Adjusted Operating Profit, But Revenue Falls Short Of Street Expectations: Retail Gets More Bearish

Energy infrastructure company Targa Resources Corp (TRGP) was in the spotlight on Thursday after the company reported record fourth-quarter adjusted profits, but its revenue failed to meet Wall Street expectations.

Targa reported a 4% year-over-year (YoY) rise in revenues to $4.41 billion, but fell short of the Street’s estimate of $4.65 billion, according to FinChat.

However, during the quarter, the firm reported record adjusted earnings before interest, tax, depreciation, and amortization (EBITDA) of $1.1 billion, marking a 5% increase sequentially. The company attributed the rise to higher volumes across the Gathering and Processing (G&P) and Logistics and Transportation (L&T) systems.

Advertisement|Remove ads.

The quarter also saw record Permian, NGL transportation, fractionation, and LPG export volumes.

The G&P segment saw higher sequential adjusted operating margins driven by record Permian natural gas inlet volumes and higher fees, partially offset by the expiration of a lower-margin high-pressure gathering and processing agreement in the Delaware Basin.

In the L&T segment, record NGL pipeline transportation, fractionation, and LPG export volumes drove the sequential increase in segment-adjusted operating margin. This was partially offset by a lower sequential marketing margin.

Advertisement|Remove ads.

For 2025, Targa expects full-year adjusted EBITDA to be between $4.65 billion and $4.85 billion, with the midpoint of the range representing a 15% rise over 2024. The firm expects to benefit from meaningful growth across its Permian G&P footprint, which is expected to drive record Permian, NGL pipeline transportation, fractionation, and LPG export volumes in 2025.

Targa also said it intends to recommend to its board a quarterly common dividend of $1.00 per common share for the first quarter.

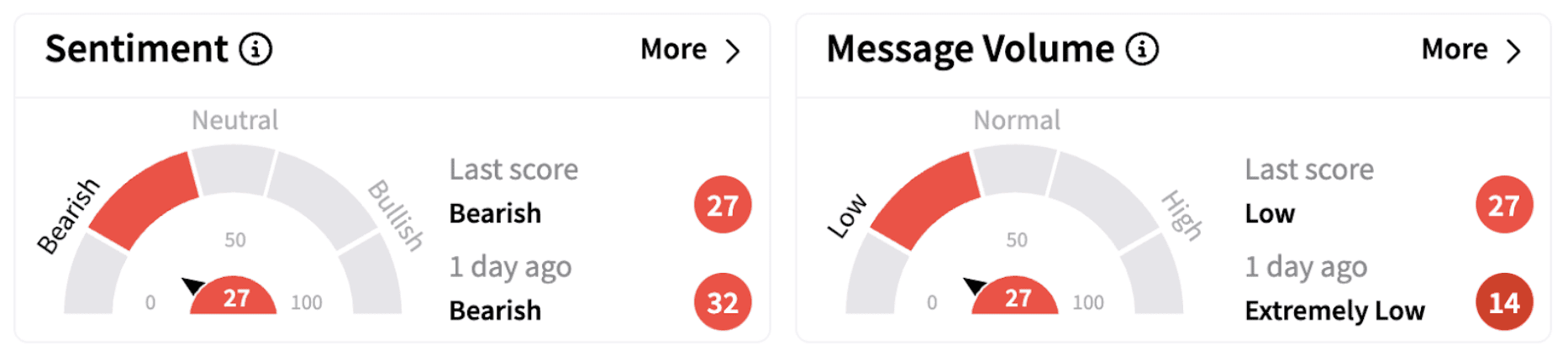

On Stocktwits, retail sentiment dipped further into the ‘bearish’ territory (27/100).

Advertisement|Remove ads.

On Thursday, Targa also announced a definitive agreement to repurchase all the outstanding preferred equity in Targa Badlands LLC from funds managed by Blackstone for approximately $1.8 billion in cash. The company said the refinancing of higher-cost preferred equity with its lower cost of debt capital will result in meaningful cash savings.

Targa shares have risen nearly 15% in 2025 and have more than doubled over the past year.

Also See: KKR Completes Second Tender Offer To Acquire Fujisoft In $4.4B Deal: Retail Sentiment Brightens

Advertisement|Remove ads.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2245018150_cbf31ea70f.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·25m agoAnushka Basu·2h ago

Anushka Basu·25m agoAnushka Basu·2h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2208663076_29e54f9e10.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·10h ago

Shashank Nayar·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2282676708_jpg_9f31eb6ee5.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·10h ago

Anan Ashraf·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Novo_Nordisk_jpg_96dd19f953.webp) Anan Ashraf·10h ago

Anan Ashraf·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Amazon_7e122accde.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Whats_App_Image_2026_05_11_at_09_45_43_1_jpeg_a08c0cf251.webp) Aveek Bhowmik·11h ago

Aveek Bhowmik·11h ago