Advertisement|Remove ads.

Dan Ives Says Tesla Is ‘Morphing Into A Physical AI Stalwart’ – But Questions On Capex Linger

- Tesla recorded better-than-expected first-quarter earnings and raised capex to $25 billion from $20 billion for 2026.

- Wells Fargo said the capex increase will pressure Tesla’s free cash flow.

- Barclays maintained an ‘Equal Weight’ rating with a $360 price target, according to The Fly.

Advertisement|Remove ads.

Tesla’s (TSLA) push to reposition itself beyond electric vehicles is gaining momentum, but it’s also getting more expensive. While it reported a modest first-quarter beat, Wall Street is concerned about the cost of its transition.

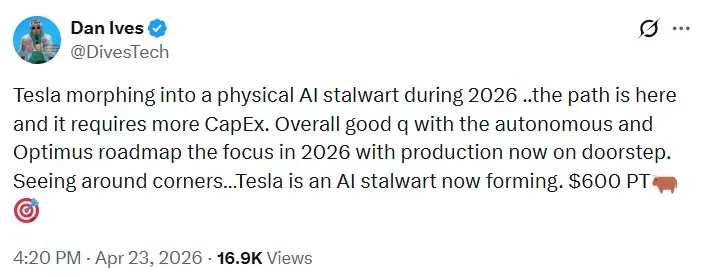

Dan Ives, managing director at Wedbush Securities, remains firmly in the bullish camp, arguing that Tesla is steadily evolving into a physical AI giant, with its autonomous driving, robotaxi, and Optimus humanoid robot initiatives set to take center stage by 2026 as they move closer to production; though it will require higher capital spending.

Ives said Tesla delivered a “good” quarter,” maintaining a $600 price target on the stock, which represents a 55% upside from Wednesday’s closing price.

Advertisement|Remove ads.

TSLA stock was down 3% in pre-market trading on Thursday.

“Tesla morphing into a physical AI stalwart during 2026 ..the path is here, and it requires more CapEx,” he wrote in a post on X.

Advertisement|Remove ads.

The company reported first-quarter (Q1) adjusted earnings of $0.41 per share, beating estimates of $0.35, according to Fiscal.ai. Revenue came in at $22.39 billion, slightly above consensus estimates of $22.20 billion.

Lot Of Bad News, Says Wells Fargo

According to The Fly, Wells Fargo maintained an ‘Underweight’ rating with a $125 price target and said it sees a “lot of bad news” despite a decent quarter.

Analyst Colin Langan of Wells Fargo said Tesla’s $25 billion in capex will pressure free cash flow, and the $1 billion year-over-year increase in operating expenses has limited near-term returns. He noted that while the Robotaxi rollout is progressing, meaningful revenue is unlikely before 2027.

Advertisement|Remove ads.

Langan also highlighted slow ramp-up for the Optimus humanoid robot and the semi-electric freight truck, delayed monetization of the AI5 chip, and the need for retrofits in Hardware 3 vehicles to achieve full self-driving.

“Hardware 3 does not have the capability to support unsupervised FSD,” Elon Musk said in the earnings call, noting that it has only about one-eighth the memory bandwidth of Hardware 4, a key requirement for achieving fully self-driving capability.

Barclays: Scaling Robotaxis Still Needs Proof

Meanwhile, Barclays maintained an ‘Equal Weight’ rating with a $360 price target. The brokerage said questions remain around its Terafab and solar investments.

Advertisement|Remove ads.

Barclays said investors still need clearer proof that Tesla can successfully scale its Robotaxi business. While full self-driving adoption is growing and approvals are expected in China and Europe, the firm warned that Tesla’s older hardware could limit uptake.

TSLA Stock: How Did Retail Traders React?

Retail sentiment on Stocktwits changed to ‘bullish’ from ‘extremely bullish’ a day earlier, amid ‘high’ message volumes.

One user highlighted “hidden liabilities” of the AI infrastructure pivot.

Advertisement|Remove ads.

Another user speculated whether part of Tesla’s capex will be redirected to fund SpaceX.

Advertisement|Remove ads.

TSLA stock has declined more than 17% so far in 2026.

Read also: Dilution Fears Return: Why ALT Stock Is Getting Hit Again

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2240015030_jpg_df09394581.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·14m ago

Shashank Nayar·14m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2266383349_jpg_cfed5c8fb1.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Whats_App_Image_2026_05_11_at_09_45_43_1_jpeg_a08c0cf251.webp) Aveek Bhowmik·1h ago

Aveek Bhowmik·1h ago/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/large_Stock_market_Image_public_domain_declining_wc_96197f57d2.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·1h ago

Arnab Paul·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_immunitybio_jpg_eb6402d336.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·1h ago

Anan Ashraf·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2221835373_jpg_b8b70aff84.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_6979_jpg_a2a1032fdc.webp) Ahmed Farhath·2h ago

Ahmed Farhath·2h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2247045310_jpg_c3c3feb79b.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·2h ago

Rounak Jain·2h ago