Lululemon shares were in focus recently, running hot since mid-October when news broke it would be added to the S&P 500 index. The stock was roughly 5% below all-time highs ahead of today’s earnings results, which were mixed versus expectations.

The athleisure retailer posted $2.20 billion in revenues during the third quarter, topping estimates of $2.19 billion. Driving that was a 12% increase in North American sales and a 49% jump internationally. Comparable sales rose 13%, with store sales rising 9% and direct-to-consumer (DTC) revenues rising 18%. DTC revenues remained at 41% of total sales, flat QoQ. 🛒

Adjusted earnings per share of $2.53 was essentially in line with expectations. Gross margins rose 110 bps YoY to 57%, below the 57.7% expected by Wall Street. The impairment of its Mirror assets weighed on margins this quarter, which is concerning with investors so focused on profitability in a weak(er) sales environment. 🔺

CEO Calvin McDonald said, “As we enter the holiday season, we are pleased with our early performance and are well-positioned to deliver for our guests in the fourth quarter.” Despite that commentary, its fourth-quarter earnings per share guidance of $4.85 to $4.93 was mixed versus estimates of $4.80 to $5.19. That also caused its full-year guidance to be worse than anticipated.

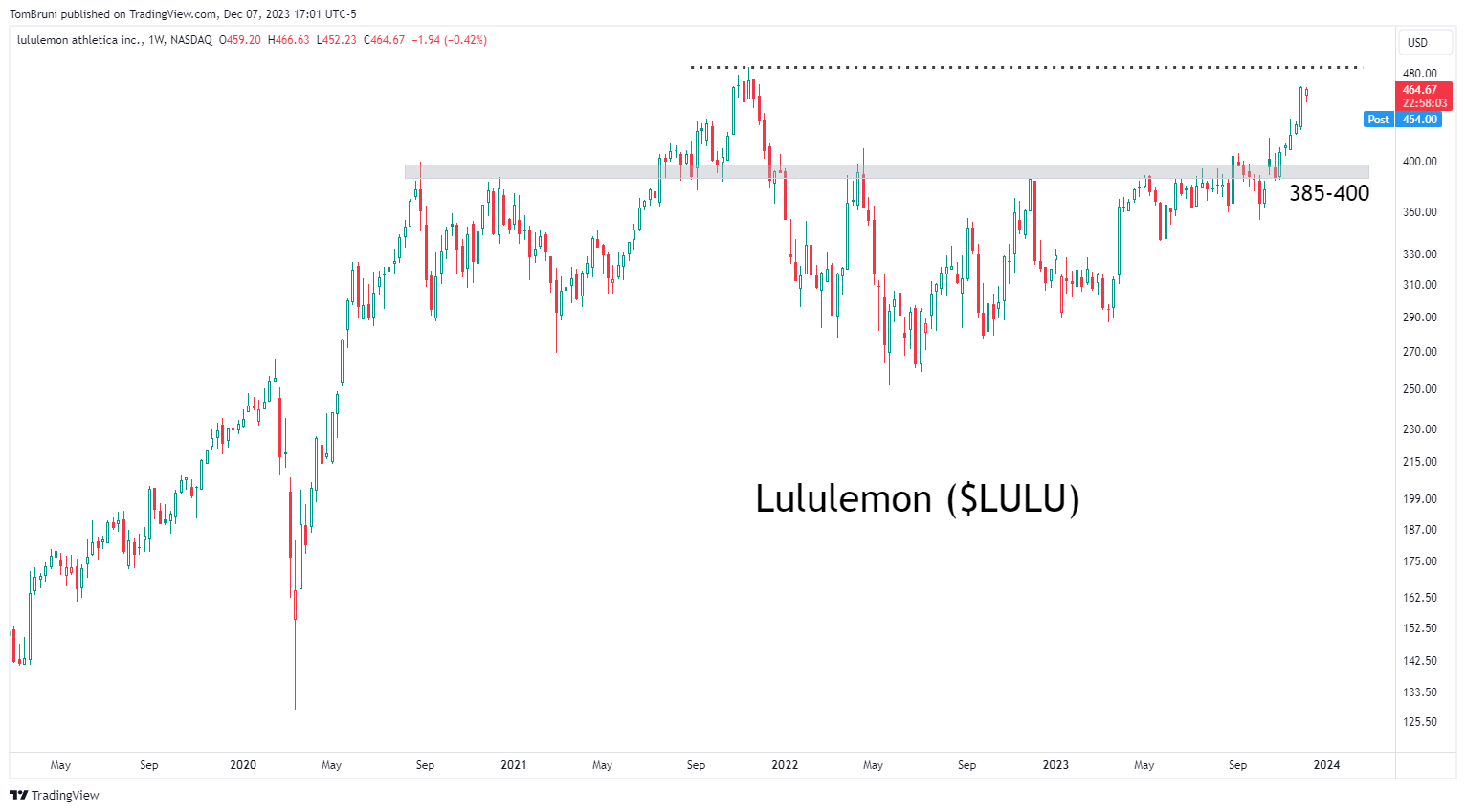

$LULU shares are down about 2% after the bell. Technical analysts continue to focus on the stock’s long-term support and resistance level, which is near 385-400. They suggest that the price’s longer-term breakout remains intact above there and that dip buyers are likely to scoop up shares if prices drift lower. 🧘