Advertisement. Remove ads.

Affirm Holdings Stock Soars Over Upbeat Q4, Strong Guidance: Retail Investors Remain ‘Bullish’

Affirm Holdings (AFRM) shares rose nearly 22% in Thursday’s pre-market after the firm, which provides point-of-sale installment loans for shopping, reported an upbeat set of fourth-quarter results and provided strong guidance.

The company reported an adjusted loss of $0.14 compared to an analyst estimate of $0.51. Revenue grew 48% year-over-year (YoY) to $659 million versus an estimate of $604 million. Affirm’s net loss narrowed to $45.14 million from $205.96 million in the year-ago period.

Affirm reported a 31% YoY rise in its gross merchandise value (GMV) — the total value of transactions — to $7.2 billion. CEO Max Levchin said the firm expects to be profitable on a GAAP basis in the fourth fiscal quarter, and plans to operate the business while maintaining GAAP profitability thereafter.

The firm’s operating loss came in at $73 million versus $244 million a year earlier, helped by a $43 million YoY reduction in other operating expenses, which the company partly attributed to a restructuring program announced in February 2023 and the realization of several operational efficiency efforts.

The largest decline was seen in technology and data analytics expenses, which fell $28 million YoY, it said.

The company expects current-quarter GMV in the range of $7.1 billion to $7.4 billion. The firm expects to report revenue of $640 million to $670 million, higher than Wall Street’s estimate of $625 million.

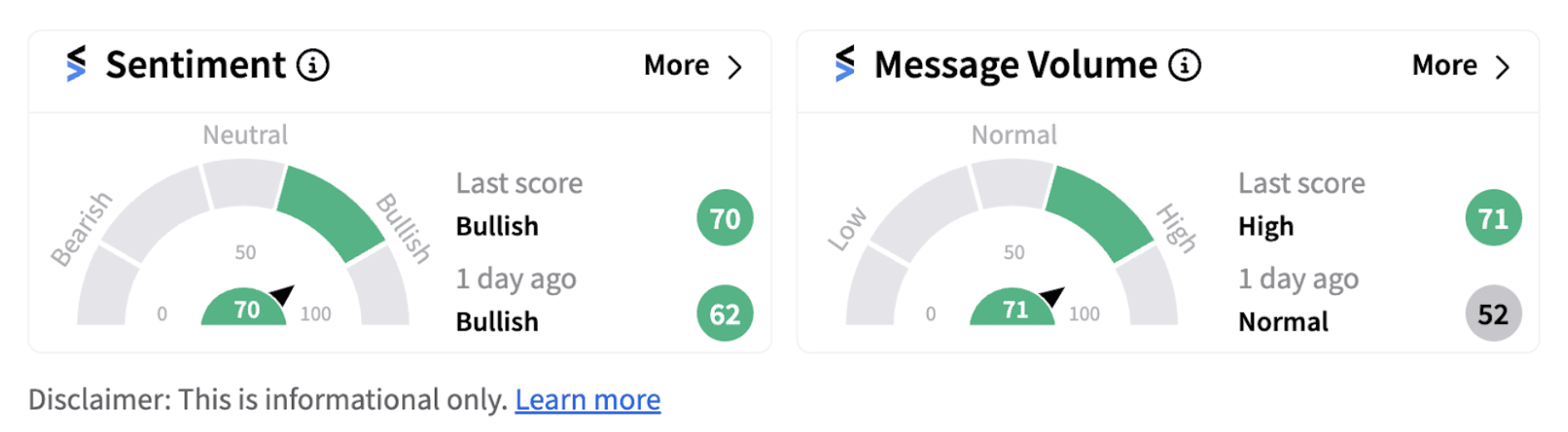

Following the announcement, retail sentiment on Stocktwits continued to trend in the ‘bullish’ territory (70/100), with a higher score and accompanied by ‘high’ message volume.

Federal Reserve Chairman Jerome Powell said recently that time has come to adjust the policy rate. The widely anticipated commencement of a rate cut cycle in September is expected to aid Affirm Holdings bring down its cost of funds and improve margins.

Shares of the firm have lost over 32% since the beginning of the year and are down over 87% since its highs in Nov. 2021. Despite a decent rebound in August, the stock still trades below its 200-day moving average. Investors are cheering the latest earnings beat but will be watching out if the firm uses the potential rate cuts to its advantage in the coming times.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Bitcoin_new_b2128e67d9.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/Prabhjote_DP_67623a9828.jpg) Prabhjote Gill·40m ago

Prabhjote Gill·40m ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2228236200_jpg_4e01019dfd.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/shivani_photo_jpg_dd6e01afa4.webp) Shivani Kumaresan·1h ago

Shivani Kumaresan·1h ago/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·46m ago

Anan Ashraf·46m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2149589805_jpg_ceec7778b8.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_4530_jpeg_a09abb56e6.webp) Ananya Mariam Rajesh·55m ago

Ananya Mariam Rajesh·55m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2227884296_jpg_f4ab8e4dcf.webp) Prabhjote Gill·1h ago

Prabhjote Gill·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Uber_July_8874a038f1.webp)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·1h ago

Rounak Jain·1h ago