Advertisement|Remove ads.

Nvidia Stock Underperformance 'One Of The Mysteries Of The Universe,' Says CEO Jensen Huang — Wall Street Analysts Agree It Shouldn't Be

- Huang said Nvidia’s strong fundamental performance would eventually reflect in the stock price.

- Analysts highlighted Nvidia’s data center business strength, expansion into non-hyperscaler customers, push into the CPU market, and the $80 billion buyback as standout items.

- Stocktwits sentiment for NVDA has remained ‘extremely bullish’ since last Friday.

Advertisement|Remove ads.

Nvidia’s stock has lagged several peer chipmakers in recent months and drew a muted response following its blowout quarterly report on Wednesday — a pattern that has repeated over the past several quarters.

Shares of the AI chipmaker edged up just 0.3% in overnight trading ahead of Friday, even as more than a dozen analysts raised their price targets, citing the company’s record-breaking performance.

Even CEO Jensen Huang is perplexed, saying in a post-earnings interview with CNBC that the move is “one of the mysteries of the universe.” He, however, said the company’s strong fundamentals would eventually reflect in the price.

Advertisement|Remove ads.

“I think all of this is going to get sorted out. In the end, they can’t hold back performance… In time, I think people will recognize our position in the marketplace, the value we deliver, and how we're supporting the ecosystem to create this new industry; everything will get sorted out,” Huang said.

Analysts Turn More Upbeat On NVDA

Nvidia’s first-quarter beat was received well by most analysts, who highlighted the strength in the data center business, expansion to non-hyperscaler customers, push into the CPU market, and the $80 billion buyback as standout items.

At least 17 analysts raised their price targets on Nvidia, with Baird's $500 target the highest, according to The Fly. That’s 128% higher than NVDA’s last close. For the full list of analysts’ revised targets, see below.

Advertisement|Remove ads.

| Analyst | Earlier PT | New PT |

| Truist | $287 | $307 |

| Raymond James | $323 | $330 |

| RBC Capital | $250 | $270 |

| Wedbush | $300 | $330 |

| Morgan Stanley | $285 | $288 |

| Goldman Sachs | $250 | $285 |

| UBS | $275 | $280 |

| Needham | $240 | $270 |

| Stifel | $250 | $282 |

| JPMorgan | $265 | $280 |

| Keybanc | $300 | $310 |

| Baird | $300 | $500 |

| Benchmark | $250 | $335 |

| Evercore | $352 | $413 |

| Bank of America | $320 | $350 |

| Jefferies | $275 | $300 |

| Deutsche Bank | $220 | $255 |

Benchmark analysts said the $200 billion CPU market opportunity Nvidia discussed is incremental to the $1 trillion sales forecast through 2027 that the chipmaker announced earlier this year.

Advertisement|Remove ads.

“The company now expects $20B of FY27 standalone Vera CPU revenue that is not included in the $1T Blackwell/Rubin framework," they said, adding that “Vera is (a) potential additive revenue layer rather than a replacement for GPU demand."

On the muted stock move, they said, “the more likely explanation is that investors have simply become increasingly complacent in their expectations of Nvidia's outsized execution, making almost any degree of outperformance look like a normal course business rather than a catalyst for a positive re-rating."

Morgan Stanley analysts said Nvidia is likely to maintain its pole position in the server market because its chips are best in class and customers want the longest useful life, adding that both the Blackwell and the next-gen Vera Rubin systems will remain in high demand.

Advertisement|Remove ads.

XTB SA's Kathleen Brooks said Nvidia’s share buyback suggests that the chip maker might be out of fresh investment ideas. “This money must be diverted from somewhere, and although there is only a small chance of this happening, it could stifle innovation at the firm," Brooks wrote in an investor note.

NVDA’s Q1 Recap

Nvidia’s fiscal first-quarter revenue increased 85% to $81.62 billion, and adjusted earnings came in at $1.87 per share. Analysts had expected $78.86 billion in revenue and a $1.76. per share profit.

Nvidia also disclosed $30 billion worth of cloud computing agreements, up sequentially from $27 billion. The company increased its quarterly cash dividend to $0.25 per share from $0.01 per share and approved an $80 billion share buyback.

Advertisement|Remove ads.

More importantly, Nvidia for the first time broke down its data center segment, its core data center segment – where revenue surged 92% to a better-than-expected $75.25 billion – into Hyperscale and ACIE (AI Clouds, Industrial, and Enterprise). It said that sales to non-hyperscaler customers were as much as those to hyperscalers.

Another standout item the company’s CPU business. With the launch of the Vera CPU and AI workloads moving to CPUs from the standard GPU options, Nvidia said it expected $20 billion in CPU sales this year and a total addressable market worth $200 billion.

NVDA Stock Move, Valuation

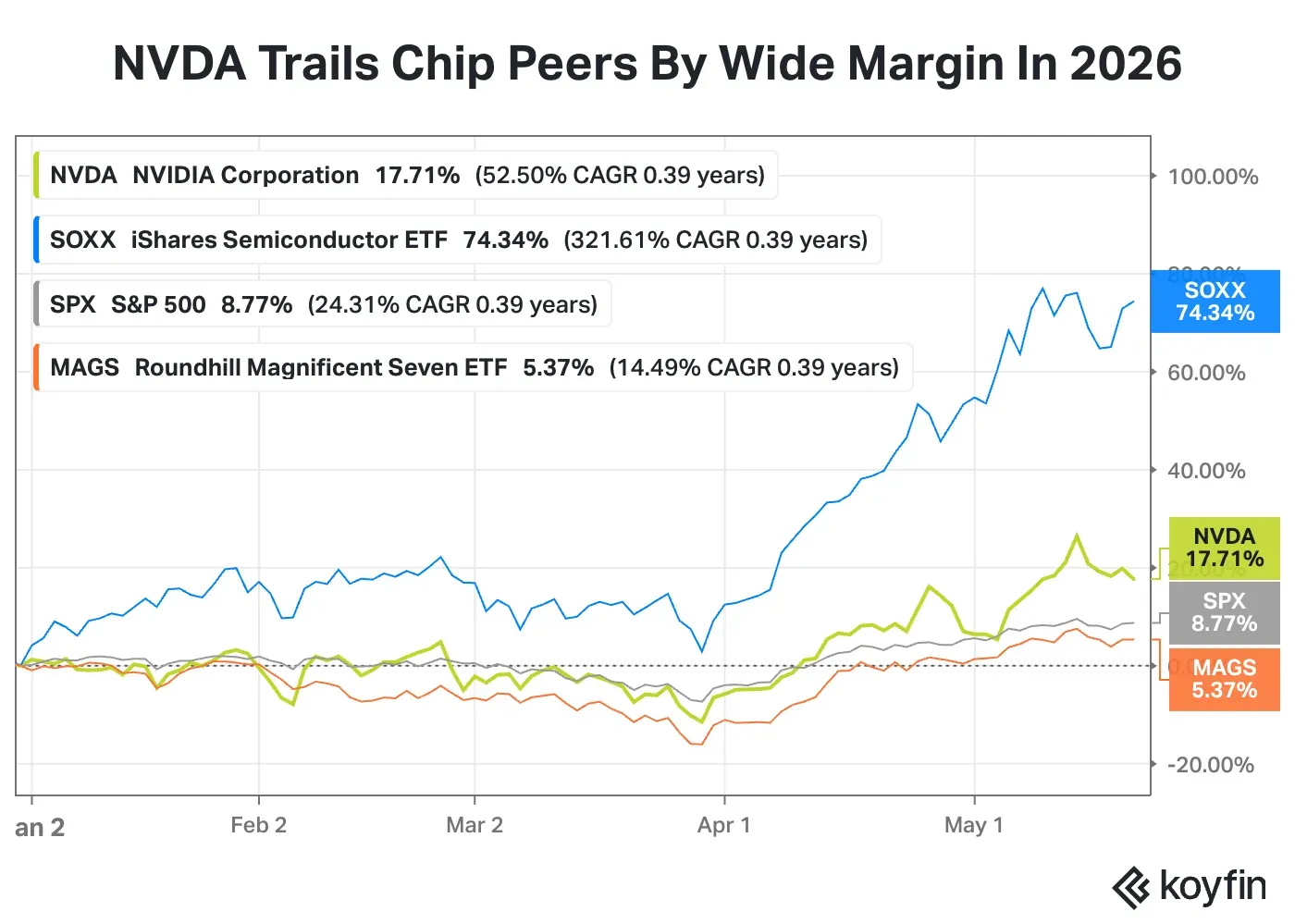

Investors appear to be waiting patiently for gains in the NVDA stock. Year to date, INTC more than tripled and STX tripled, while WDC, ARM, and MU gained over 150% – pushing the iShares Semiconductor ETF (SOXX) 73% higher. In comparison, NVDA stock has gained a mere 17%.

Advertisement|Remove ads.

Interestingly, Nvidia has held up better within the “Magnificent Seven” group. It is the second-best performer in the cohort this year, behind Alphabet, while Meta, Tesla, and Microsoft have slipped into negative territory. In terms of the 12-month forward price-to-earnings ratio, it is the second cheapest among the Mag7s.

| Company | 12-month Forward P/E | YTD Move |

| Nvidia | 22.1 | 17.70% |

| Amazon | 32.1 | 16.30% |

| Microsoft | 22.7 | -13% |

| Meta | 18.5 | -8% |

| Apple | 33.5 | -12.40% |

| Alphabet | 30.8 | 24% |

| Tesla | 194.3 | -7% |

Currently, 59 of 62 analysts covering NVDA have a ‘Buy’ or higher rating, two have ‘Hold,’ and one has ‘Sell,’ per Koyfin data. Their average price target of $292.35 implies an upside of 33% from the stock’s last close. On Stocktwits, retail sentiment for NVDA has remained ‘extremely bullish’ since last Friday.

Advertisement|Remove ads.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2286019501_0704608c45.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·36m ago

Anushka Basu·36m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1234739851_1_4e5d1263a0.jpg) Anushka Basu·2h ago

Anushka Basu·2h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1317870360_fd65c7f7d0.jpg) Anushka Basu·4h ago

Anushka Basu·4h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2245018150_cbf31ea70f.jpg) Anushka Basu·6h agoAnushka Basu·7h ago

Anushka Basu·6h agoAnushka Basu·7h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2208663076_29e54f9e10.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·15h ago

Shashank Nayar·15h ago