Advertisement|Remove ads.

OPEN Stock Can’t Stop Bleeding Yet As Sales Slide, Losses Widen — But Retail Believes CEO's Turnaround Case

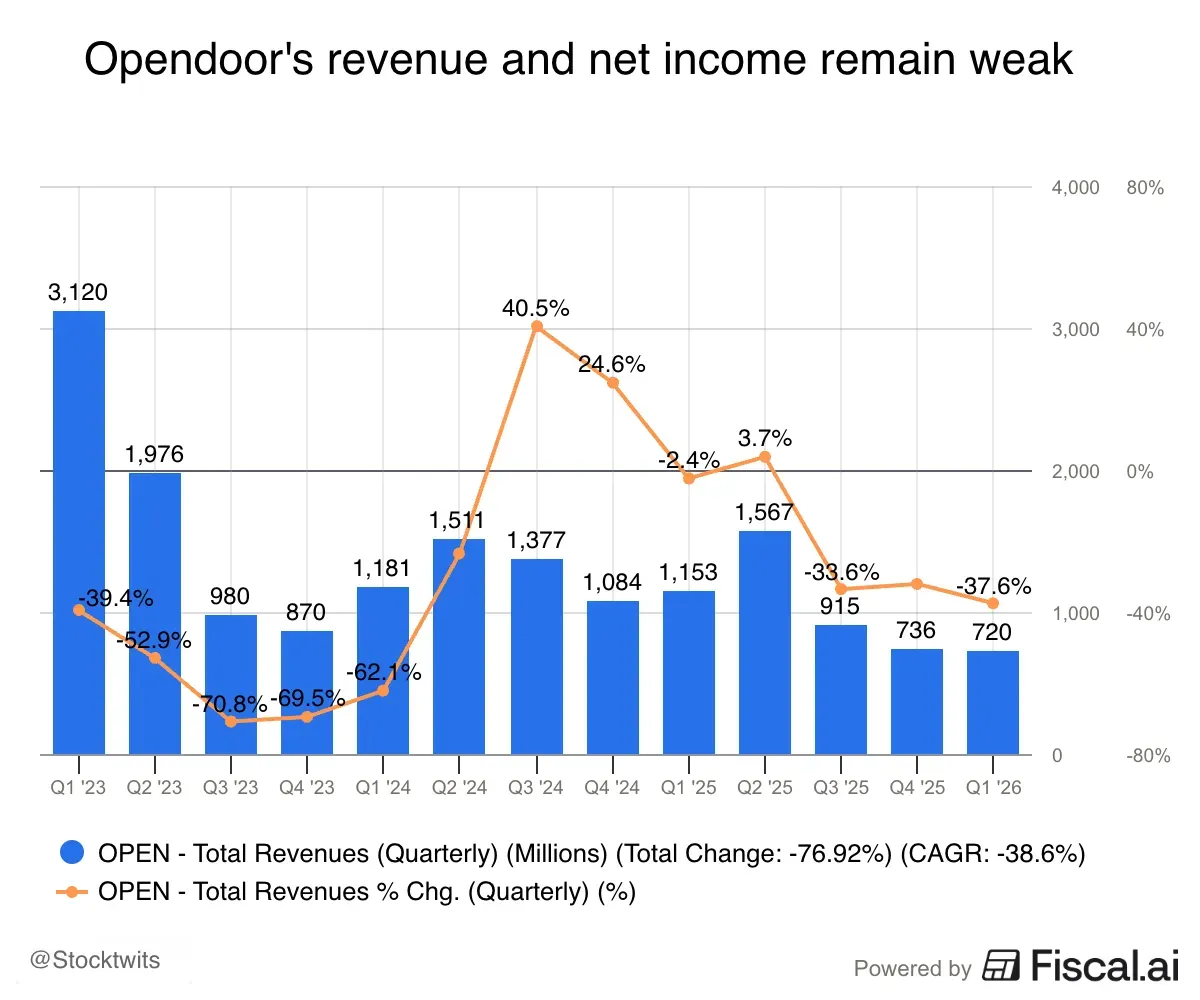

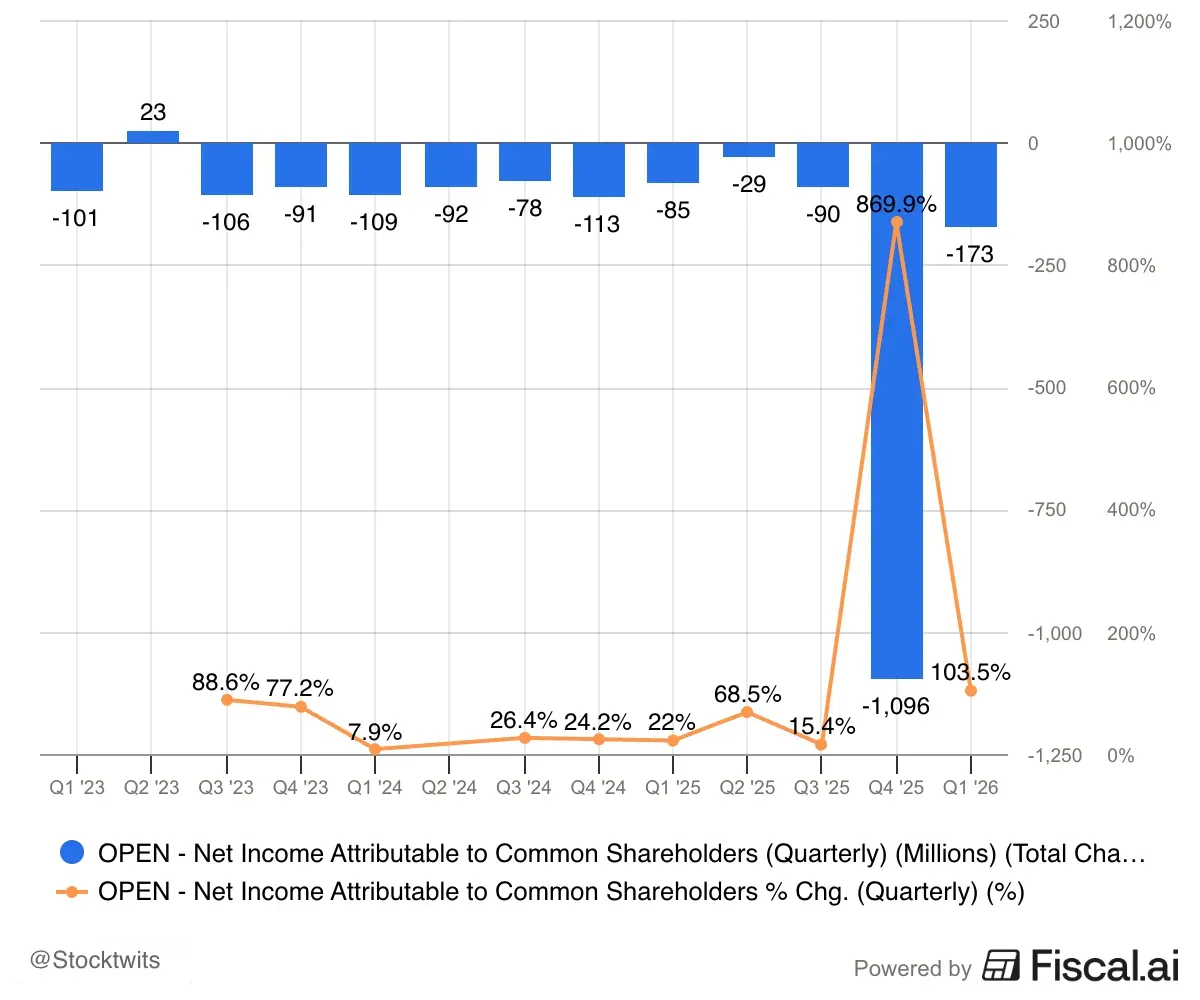

- First-quarter revenue declined 38% year over year to $720 million, and net loss more than doubled to $173 million.

- Management excessively cited the improving health of the company’s housing inventory as part of “structural” improvement in the business.

- OPEN dropped 2.6% after the earnings report, but retail sentiment on Stocktwits improved to ‘extremely bullish’ from ‘bullish.’

Advertisement|Remove ads.

Opendoor Technologies shares fell 2.6% on Thursday after the real estate platform reported first-quarter results that showed continued sales declines and widening losses. Retail investors, however, do not seem overly concerned yet.

The company’s stock is on course for its second straight weekly decline.

Retail sentiment improved as traders focused on management’s commentary on “structural” improvements since Kaz Nejatian took over as CEO last September, including improved housing portfolio health and the path toward EBITDA profitability in the coming quarters.

Advertisement|Remove ads.

Opendoor said second-quarter revenue will be 25% higher sequentially. The quarter will also see the company generate adjusted EBITDA, a trend that it said will continue in the subsequent quarters.

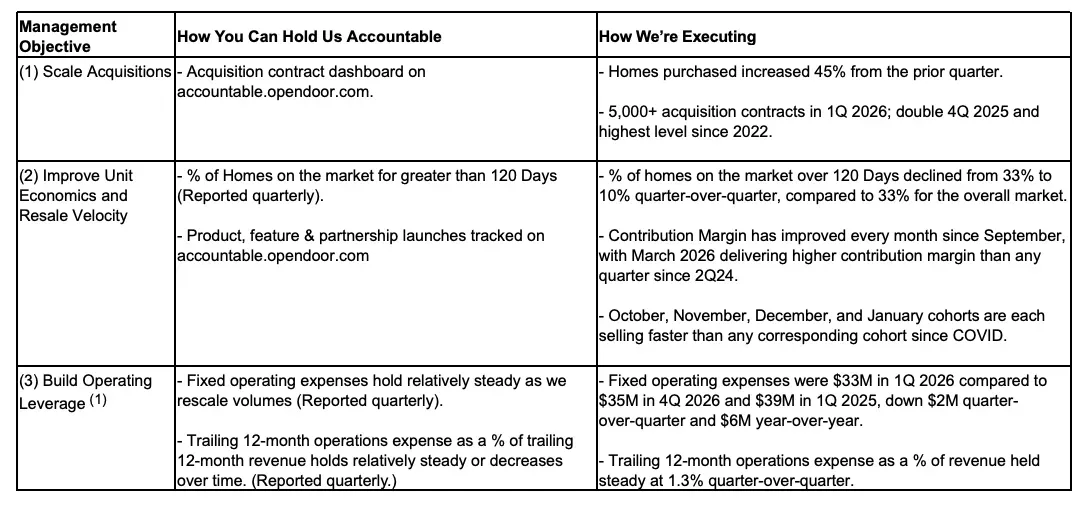

OPEN Improves Housing Inventory

The earnings statement featured lengthy commentary about how housing acquisitions, both the pace and margins, have improved in recent months, and set the business up for better financial performance.

“The October cohort was just the start. A full quarter later, we’ve gone from a claim to a track record,” Nejatian said. “Our 4Q25 and January 2026 cash acquisition cohorts have the best combination of margin, margin stability, and resale velocity of any corresponding cohort in company history (excluding the COVID-era cohorts).”

Advertisement|Remove ads.

“And, each of our October, November, December, and January cohorts are selling faster than any corresponding cohort since COVID. Acquisition contracts are up 2x quarter-over-quarter, back to levels we haven’t seen since 2022. Aged inventory has been cut from half the book to one-tenth while scaling volume. As a result, resale contribution margin is at its highest level in nearly two years.”

Nejatian said aged inventory decreased to 10% from 51% in the third quarter of last year; In terms of housing metrics, the performance is the strongest in 10 years, he said. A snapshot of the company’s focus areas and the plans for them is below:

OPEN’s Underlying Performance Still Concerning

Still, the underlying business continued to see acute weakness. In the first quarter, revenue declined 38% year over year to $720 million – the top line has now shrunk sequentially for the past four quarters. Q1 net loss more than doubled to $173 million.

Advertisement|Remove ads.

Opendoor emerged as a top meme stock, surging more than 2,000% in a two-month stretch last year, but has since slid steadily from September, leaving some traders frustrated. Opendoor shares are down 9% year-to-date, as of their last close.

Advertisement|Remove ads.

Retail Traders Express Hope For OPEN

On Stocktwits, retail sentiment for OPEN turned ‘extremely bullish’ from ‘bullish’ just before the results were issued in post-market hours on Wednesday, with many citing positive EBITDA news and improving inventory health as the standout items.

“$OPEN Super bullish. Turnaround is working and going in the right direction. Conviction grows stronger,” said a trader.

Another wrote: “The report isn’t perfect, sure, but stocks don’t always move off the obvious numbers; they move off what was expected and what’s already priced in. If we reclaim and hold 5.5-5.6 with volume, things get interesting. Better margins, cleaner inventory, and squeeze pressure could start kicking in.”

Advertisement|Remove ads.

On X, hedge fund manager and Opendoor investor Eric Jackson blamed algorithmic traders for the selloff. “Odd... Kaz said on the call ‘Here's what you'd have to see in order to know we're not doing a good job…’ and, as he listed off those things, the stock price sold off 4%... guess the algos aren't that smart,” he said.

OPEN stock is down more than 8% this year, after more than tripling in 2025.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_moonlake_jpg_376bc698df.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·33m ago

Arnab Paul·33m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2274352900_jpg_d03c4e3fff.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·44m ago

Rounak Jain·44m ago/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/large_Archer_Aviation_resized_db3acc3d4e.jpg)

/filters:format(webp)https://st-everywhere-cms-prod.s3.us-east-1.amazonaws.com/Bhavik_Nair_b1ba9448ab.jpg) Bhavik Nair·48m ago

Bhavik Nair·48m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2211161375_jpg_15de12366a.webp) Rounak Jain·1h ago

Rounak Jain·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2196133264_jpg_43c746e098.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/IMG_9209_1_d9c1acde92.jpeg) Yuvraj Malik·1h ago

Yuvraj Malik·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2229019636_jpg_c4ecd5bc01.webp) Arnab Paul·2h ago

Arnab Paul·2h ago