Advertisement|Remove ads.

SLS Vs MLTX: Retail Traders Race To Pick Merck’s Next Biotech Buyout As Keytruda’s $31.7B Patent Cliff Nears

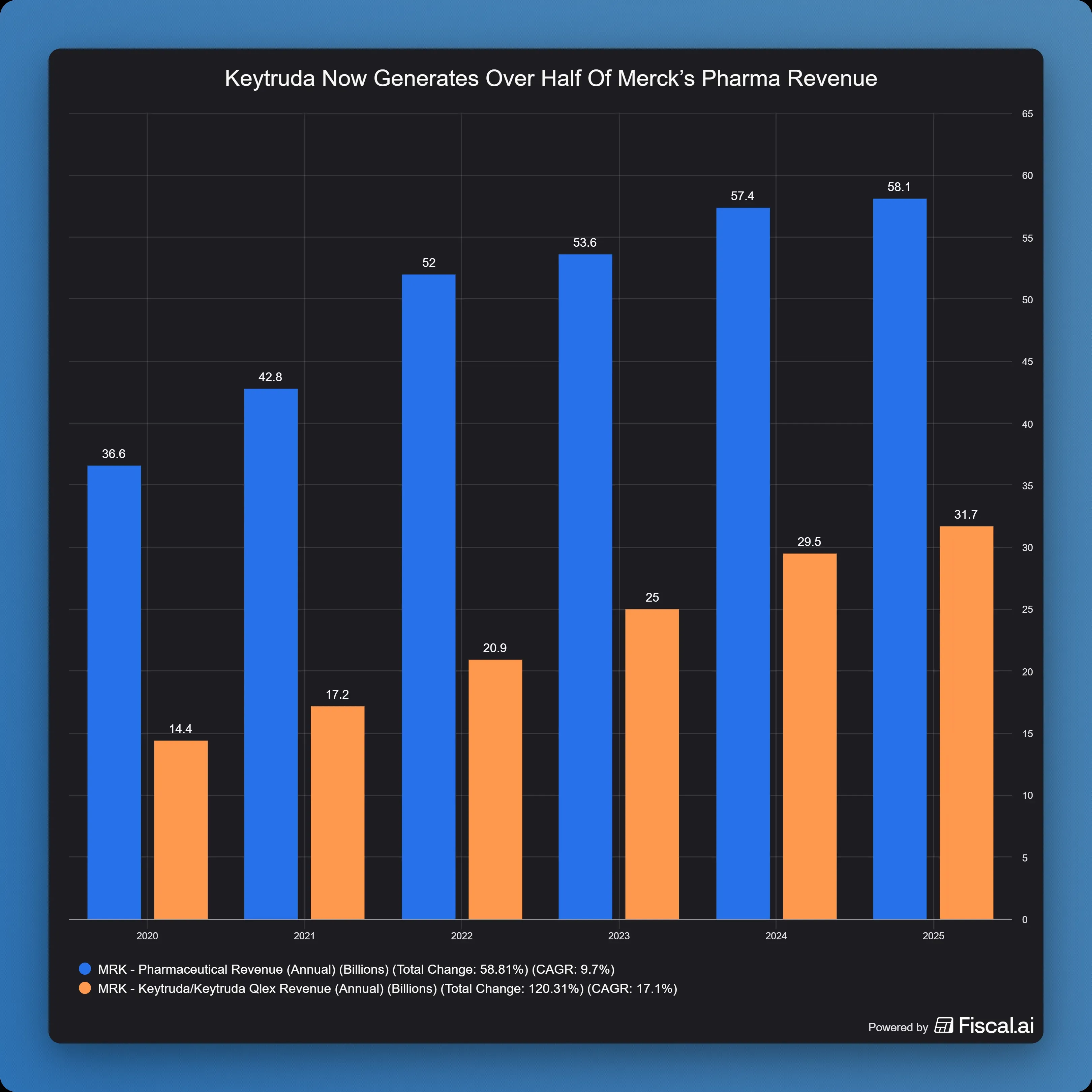

- Keytruda generated $31.7 billion in 2025, accounting for 55% of Merck’s pharma revenue ahead of its 2028 U.S. patent cliff.

- The SLS thesis centers on GPS, an AML immunotherapy nearing its pivotal Phase 3 final analysis after reaching 78 of 80 required events.

- MLTX has prior Merck interest and is preparing an FDA filing for its lead drug, Sonelokimab, to treat a chronic inflammatory skin disease.

Advertisement|Remove ads.

Sellas Life Sciences (SLS) and MoonLake Immunotherapeutics (MLTX) have emerged as retail’s leading candidates for Merck & Co.’s (MRK) next biotech deal as the drugmaker prepares for life beyond Keytruda.

SLS and MLTX each gained more than 2% at the start of overnight trading late Sunday, while MRK edged marginally higher.

MRK’s Keytruda Raises Stakes For New Deals

Merck said on Friday that the U.S. Food and Drug Administration (FDA) approved Keytruda, its flagship cancer drug, and Keytruda Qlex, a newer version given as an injection under the skin, each in combination with Pfizer and Astellas’ Padcev, for use before and after surgery in adults with muscle-invasive bladder cancer. The approval expands Keytruda’s already dominant cancer franchise, while also underscoring Merck’s dependence on it.

Advertisement|Remove ads.

Keytruda and Keytruda Qlex generated $31.7 billion in 2025, equal to about 55% of Merck’s $58.1 billion in pharmaceutical revenue. Since 2020, Keytruda sales have more than doubled, while the total pharmaceutical business has grown at a much slower pace. Keytruda now generates more than half of Merck’s pharmaceutical revenue.

The concentration has become more important as Keytruda nears the loss of its U.S. exclusivity, beginning in 2028. Merck reorganized its human-health operation in February, creating a dedicated oncology division as it seeks to preserve its leadership beyond Keytruda. It has also spent heavily on acquisitions, including Verona Pharma, Cidara Therapeutics, and Terns Pharmaceuticals.

Advertisement|Remove ads.

After outlining Merck’s post-Keytruda growth plans earlier this year, CEO Robert Davis told investors: “And we’re not done.” Retail traders are taking him at his word.

Why SLS Bulls See A Merck Buyout

The Sellas thesis centers on galinpepimut-S (GPS), the company’s WT1-targeting immunotherapy. Sellas is evaluating GPS in the Phase 3 Regal trial as a maintenance therapy for acute myeloid leukemia (AML) patients who entered remission following second-line treatment. The study has recorded 78 of the 80 patient-death events required to trigger its final analysis, placing the program near a potentially final readout.

Sellas has said the trial would be successful if GPS achieves a median overall survival of at least 12.6 months, compared with 8 months in the control arm. The trial remains blinded, meaning the slower accumulation of events may be encouraging but does not prove that GPS succeeded. On the other hand, retail interest is heating up: Stocktwits sentiment eased to ‘bullish’ from ‘extremely bullish’ a week earlier, even as 24-hour message volume surged 53% and the stock’s watcher count climbed 5% over the past month.

Advertisement|Remove ads.

“Things are heating up for SLS,” one bullish user said, while another trader argued: “Over $30 billion of revenue [is] in jeopardy. Who will they buy to extend keytrudas patent monopoly?” The user called Sellas as one possible answer and suggested that competing interest from other pharma companies could force Merck to act.

Other SLS bulls believe GPS could ultimately have uses beyond AML because WT1 is expressed across numerous cancers. “GPS is the one therapy that has such a wide multi-platform application potential,” one user said, arguing that only a large pharma company such as Merck could finance the trials required to test the therapy broadly.

Another trader warned that Merck could weaken its cancer position if a competitor moved first: “If SLS falls into the hands of LLY, JNJ or PFE, Merck loses their oncology crown.”

Advertisement|Remove ads.

Merck’s $6.7 billion acquisition of Terns in March strengthened the retail thesis. The deal gave Merck TERN-701, an investigational drug for chronic myeloid leukemia still in Phase 1/2 testing. “They need to take bigger risks at this moment in the industry,” one SLS bull said. “I think SLS is the right play to combine with Keytruda.” Traders have also highlighted CEO Angelos Stergiou’s Fourth of July reference to “strategic partners” and amended executive agreements containing change-of-control provisions.

Merck’s Past Bid Fuels MLTX Buzz

MoonLake investors have one advantage Sellas bulls do not: a previously reported approach from Merck. Merck reportedly submitted a nonbinding offer valuing MoonLake at more than $3 billion last year. The initial approach was rejected, although talks could potentially be revived. The Merck connection is once again driving attention toward MLTX. Stocktwits sentiment for MLTX improved to ‘bullish’ from ‘neutral’ a day earlier, while weekly message volume surged 760% and the stock’s watcher count rose 5% over the past month.

“Don’t think SLS is the target if Friday’s action says anything,” one trader said, arguing that MoonLake held up better on strong volume while SLS moved with the broader biotech sector. “Tells me something is up with MLTX, not SLS,” the user added.

Advertisement|Remove ads.

MoonLake’s lead drug, Sonelokimab, has completed Phase 3 development in hidradenitis suppurativa. At one year, 67% of patients achieved a strong improvement in disease severity, 33% reached complete skin clearance under a key measure and 26% achieved inflammatory remission. The company plans to submit a Biologics License Application (BLA) to the FDA by Sept.30 and request Priority Review.

“When will rumors turn into reality?” one MLTX bull said. “MRK needs to buy something! Let it [be] MLTX.” Another user claimed MoonLake was “in talks with MRK for a buyout,” although neither company has confirmed any negotiations.

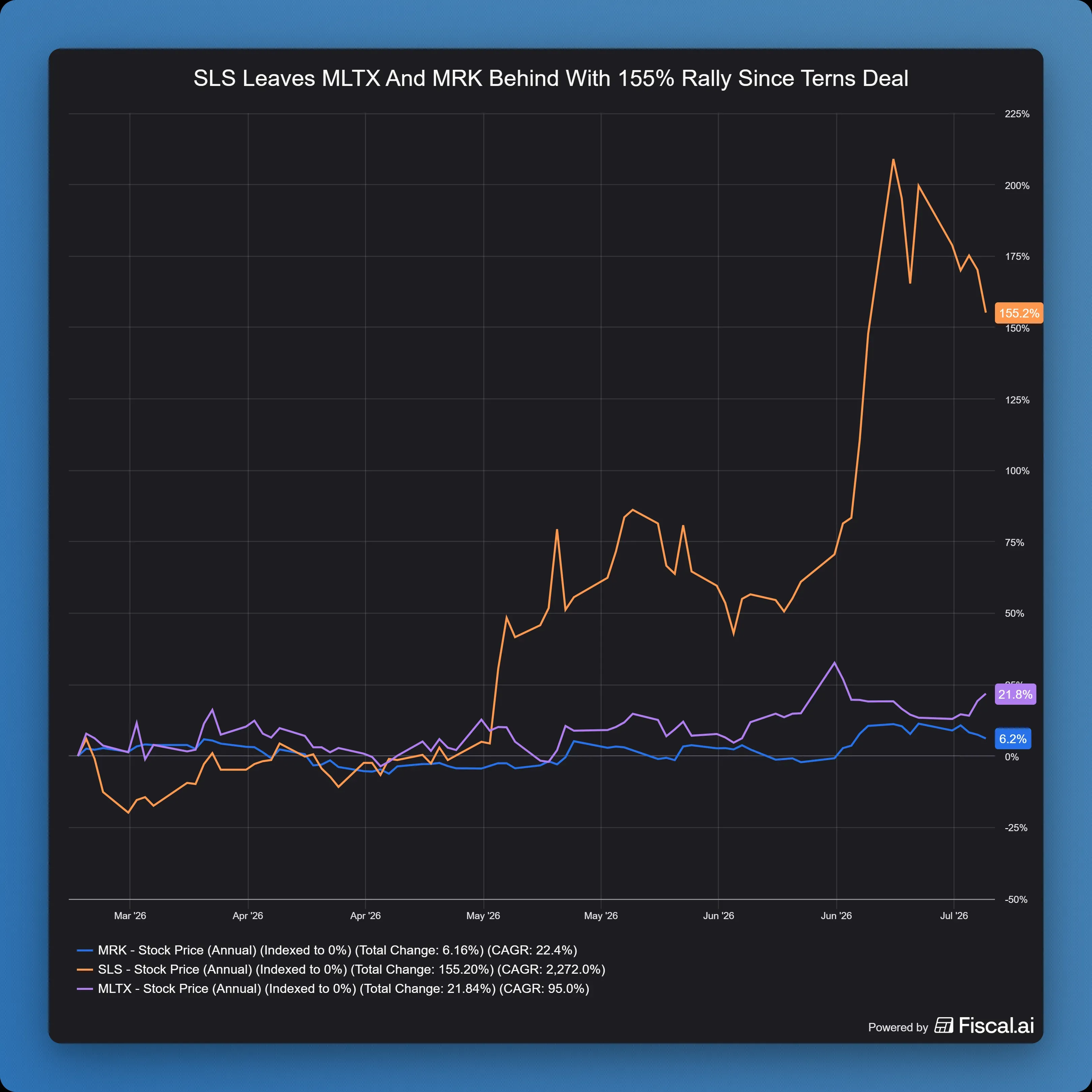

SLS Outruns MLTX As Buyout Pressure Builds

Since Merck announced its acquisition of Terns, SLS shares have risen 155%, compared with 22% for MLTX and 6% for Merck.

Advertisement|Remove ads.

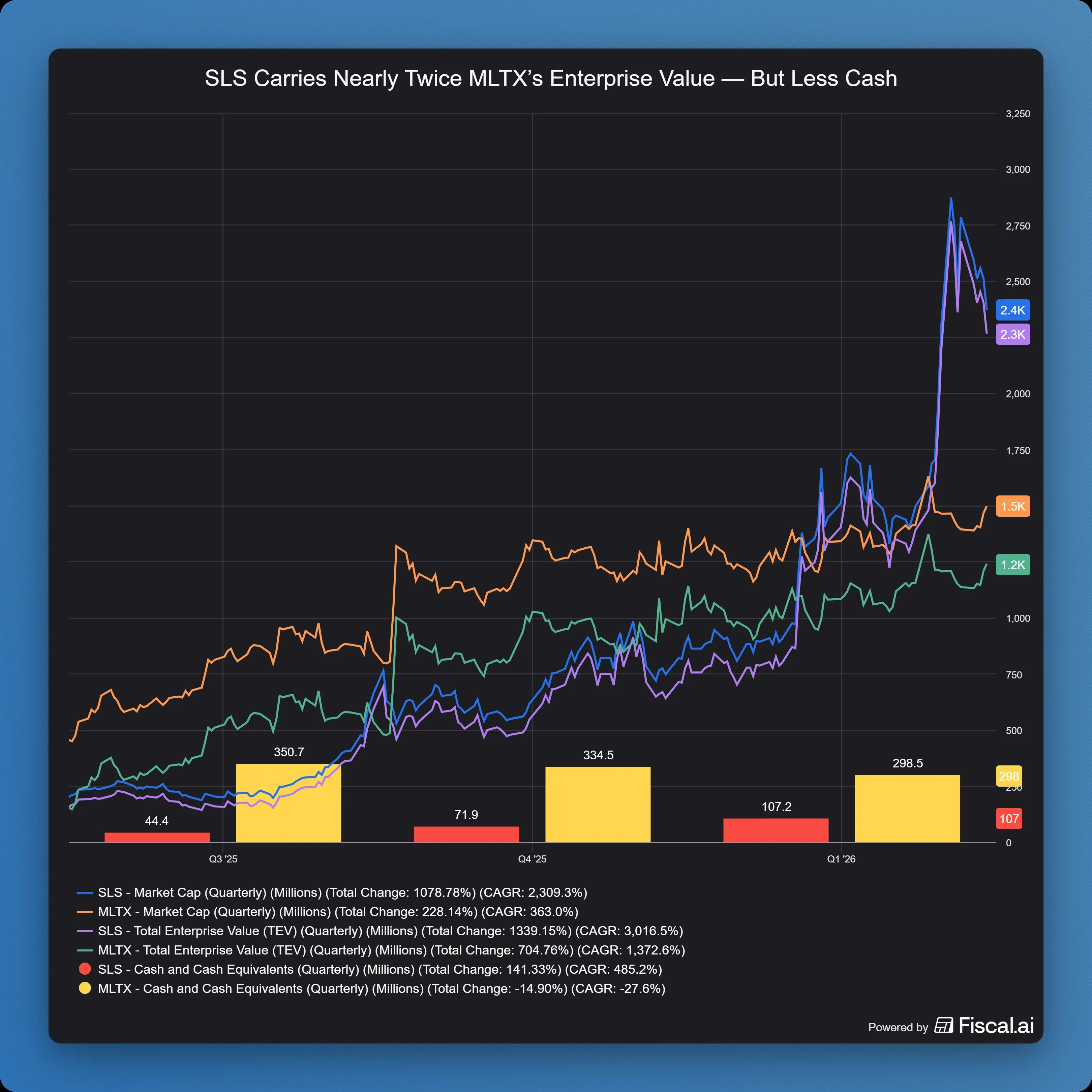

Meanwhile, Sellas carries a market cap of about $2.4 billion and an enterprise value of $2.3 billion. MoonLake is valued at $1.5 billion, with an enterprise value of about $1.2 billion. MoonLake also held $298.5 million in cash at the end of the first quarter, compared with $107.2 million for Sellas.

Advertisement|Remove ads.

David Giroux, chief investment officer at T. Rowe Price Investment Management, told Barron’s on Friday that large pharma companies face a $400 billion to $500 billion patent-expiration hole over the next decade that internal research alone cannot fill. He expects a “tremendous number” of small and mid-cap biotech firm to be acquired at premiums of 50% to 100%. Giroux specifically named MoonLake among seven potential targets. “I would be shocked if all weren’t acquired in the next few years for big premiums over their current value,” he said.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2237643016_jpg_17a9a7eb9d.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·18m ago

Anan Ashraf·18m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_samsung_jpg_fcdaaf7c72.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Prabhjote_DP_67623a9828.jpg) Prabhjote Gill·55m ago

Prabhjote Gill·55m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Astra_Zeneca_jpg_a49cc22562.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/vivekkrishnanphotography_58_jpg_0e45f66a62.webp) Arnab Paul·57m ago

Arnab Paul·57m ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Stock_rising_chart_jpg_77422192ba.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Rounak_Author_Image_7607005b05.png) Rounak Jain·1h ago

Rounak Jain·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2238206656_jpg_35fcb4c6e6.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·1h ago

Anushka Basu·1h ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2229019709_jpg_f82a27a246.webp) Prabhjote Gill·2h ago

Prabhjote Gill·2h ago