Advertisement|Remove ads.

Tesla Stock Rises Premarket: Investor Ross Gerber Says ‘People Just Hate The Brand Now’ As AI Pivot Faces Earnings Reality Check

- Gerber warned that Tesla still relies heavily on its EV and battery-storage businesses for cash generation.

- Ahead of Q1 results due Wednesday, Gerber also pushed back on Tesla’s AI and robotics push, saying the company was “trying to distract from the lack of earnings.”

- Jefferies forecasts about $21.2 billion in revenue and $0.14 EPS amid rising capex and widening production-delivery gaps.

Advertisement|Remove ads.

Shares of Tesla, Inc. (TSLA) rose 0.4% in premarket trading on Monday ahead of its quarterly results due Wednesday, even as investor attention turned to brand sentiment risks and concerns around the EV firm’s shift toward AI and robotics after fresh criticism from longtime shareholder Ross Gerber.

Gerber Warns Tesla EV Demand Drives Cash Risk

Gerber said in an interview with Yahoo Finance: “There’s a lot of analysts that think they’re going to grow sales over the next couple years and I just don’t know with whom.” He also said: “People just hate the brand now and it sucks because it’s all predicated on Elon’s behavior.”

Gerber also warned that Tesla still depends primarily on its EV and battery-storage businesses for cash generation, meaning pressure on vehicle demand risks creating a “snowball going the wrong way.”

Advertisement|Remove ads.

Gerber Kawasaki Wealth & Investment Management owns about a 0.01% stake in Tesla valued at over $90 million, according to Koyfin data. In 2023, Gerber said he planned to pursue a board seat at the company to help “rein in” Musk and argued that Tesla needed to “build its image around Tesla, and not just around Elon.”

He added that brand perception could become especially important as Tesla prepares to compete in autonomous mobility services against platforms such as Alphabet, Uber, Lyft and Amazon. “If people don’t like your brand, they’re not going to take your service when there’s three other people to take,” he said.

Gerber Flags FSD Promise Concerns Again

In posts on X ahead of the earnings release, Gerber also pushed back on Tesla’s positioning as an AI and robotics company.

Advertisement|Remove ads.

“Tesla trying to distract from the lack of earnings they will soon report. They continue to kick the can down the road,” he said, adding separately that Tesla “needs to make people whole” after some customers paid for Full Self-Driving (FSD) features that “have never worked as promised.”

Responding to another user’s comment that Tesla was transitioning toward AI and robotics as part of its long-term strategy, Gerber replied: “They don’t own the brains to their ‘robot’. Call me when it’s ready.”

Tesla’s FSD tech has remained a point of debate among customers and investors, with lawsuits alleging buyers paid thousands of dollars for autonomy capabilities that have yet to materialize as originally marketed, according to a Wall Street Journal report.

Advertisement|Remove ads.

TSLA Q1 Preview

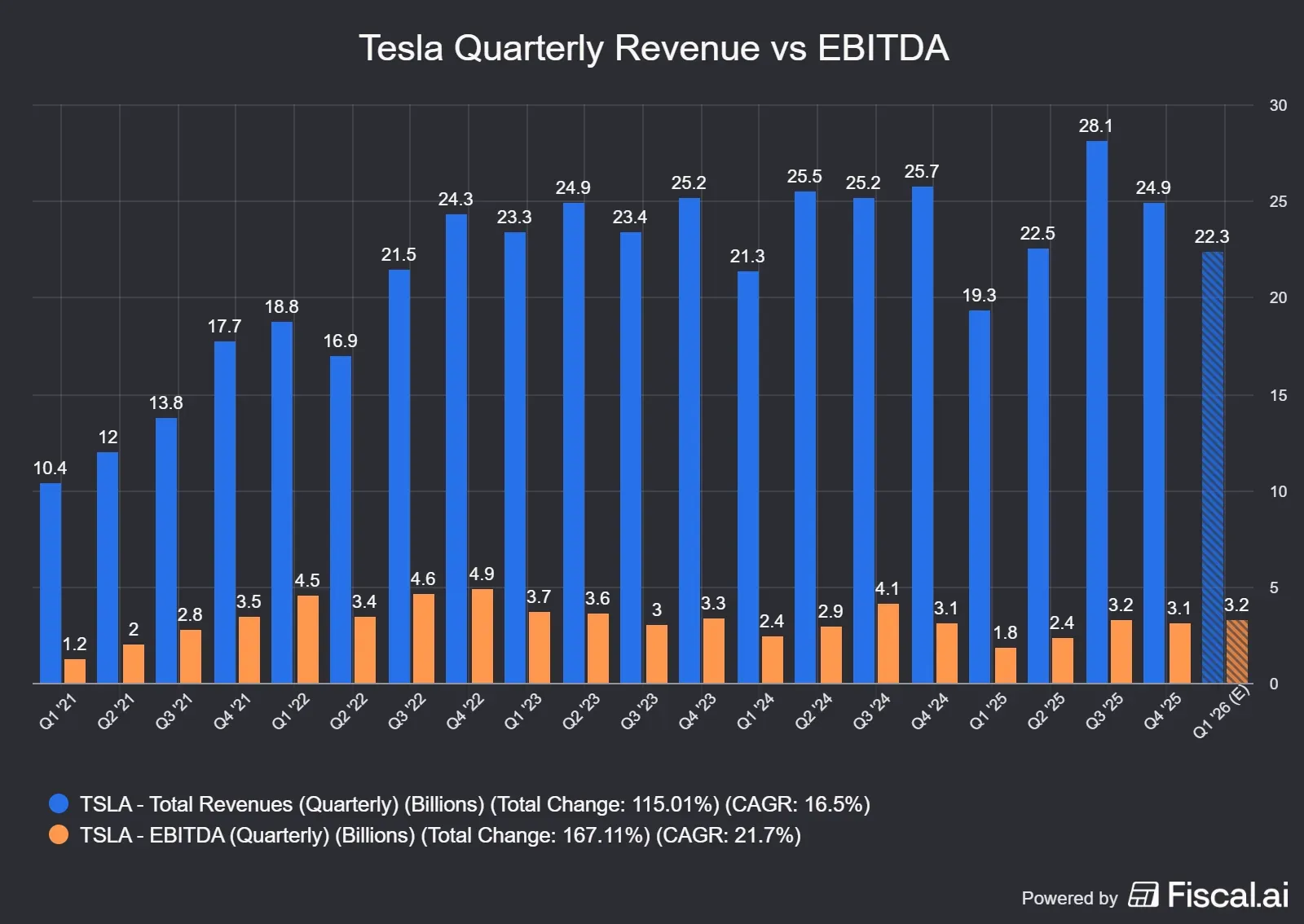

Tesla heads into its first-quarter (Q1) report under pressure after a recent delivery miss and rising capex expectations clouded the near-term outlook.

Jefferies expects about $21.2 billion in Q1 revenue, a core automotive gross margin near 15.5%, an operating margin below 3% and GAAP earnings per share (EPS) of $0.14. Tesla’s company-compiled analyst consensus points to a similarly modest setup, including $21.4 billion in revenue and $541 million in operating income.

Advertisement|Remove ads.

Tesla delivered 358,023 vehicles in Q1, up from 336,681 a year earlierafter last year’s Model Y transition disrupted production. However, production reached 408,386 vehicles, leaving output ahead of deliveries by more than 50,000 units, marking the widest gap in at least four years.

The company also missed company-compiled consensus delivery expectations of 365,645 vehicles, marking the second consecutive quarterly miss.

How Do Retail Traders Feel About TSLA?

On Stocktwits, retail sentiment was ‘extremely bullish’ amid ‘high’ message volume.

Advertisement|Remove ads.

One user said, “I guess you have to ignore the numbers to be a true Tesla bull. Reality is FUD.”

Another user said, “It’s going to hurt so bad when Elon starts with his promises on the earnings call.”

Advertisement|Remove ads.

TSLA stock has risen 63% over the past year.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Michael_Burry_jpg_fa0de6ac92.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/unnamed_jpg_9dff551b50.webp) Anan Ashraf·33m ago

Anan Ashraf·33m ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_2204154647_jpg_f2ab9ac6ab.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/1707726834303_jpg_11f20a9aa9.webp) Shashank Nayar·54m ago

Shashank Nayar·54m ago/filters:format(webp)https://news.stocktwits-cdn.com/Getty_Images_540198451_jpg_3e5f3d8ee7.webp) Shashank Nayar·2h ago

Shashank Nayar·2h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_spacex_53269b0228.jpg) Shashank Nayar·3h ago

Shashank Nayar·3h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2289079202_89814720c2.jpg) Anan Ashraf·3h ago

Anan Ashraf·3h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_us_stocks_jpg_64b4ea4fc0.webp) Shashank Nayar·3h ago

Shashank Nayar·3h ago