Advertisement|Remove ads.

CrowdStrike, Zscaler, Palo Alto, Fortinet: Which Cybersecurity Stock Will Win Next Year? Wall Street Sees 35% Room To Run In This Pick

- Morgan Stanley’s September survey showed that chief information officers expect cybersecurity spending to grow 50% faster than overall software spending.

- Fortinet screens as the cheapest, given its negative returns this year.

- Zscaler comes off as the retail favorite, attracting strongly bullish sentiment and brisk message volume.

Advertisement|Remove ads.

The tech sector’s strong run this year has cooled in recent sessions as some strategists and fund managers question the authenticity of the AI-driven rally that has powered the market since the 2022 bear-market bottom. Performance across the tech sector has been uneven, with the software industry trailing.

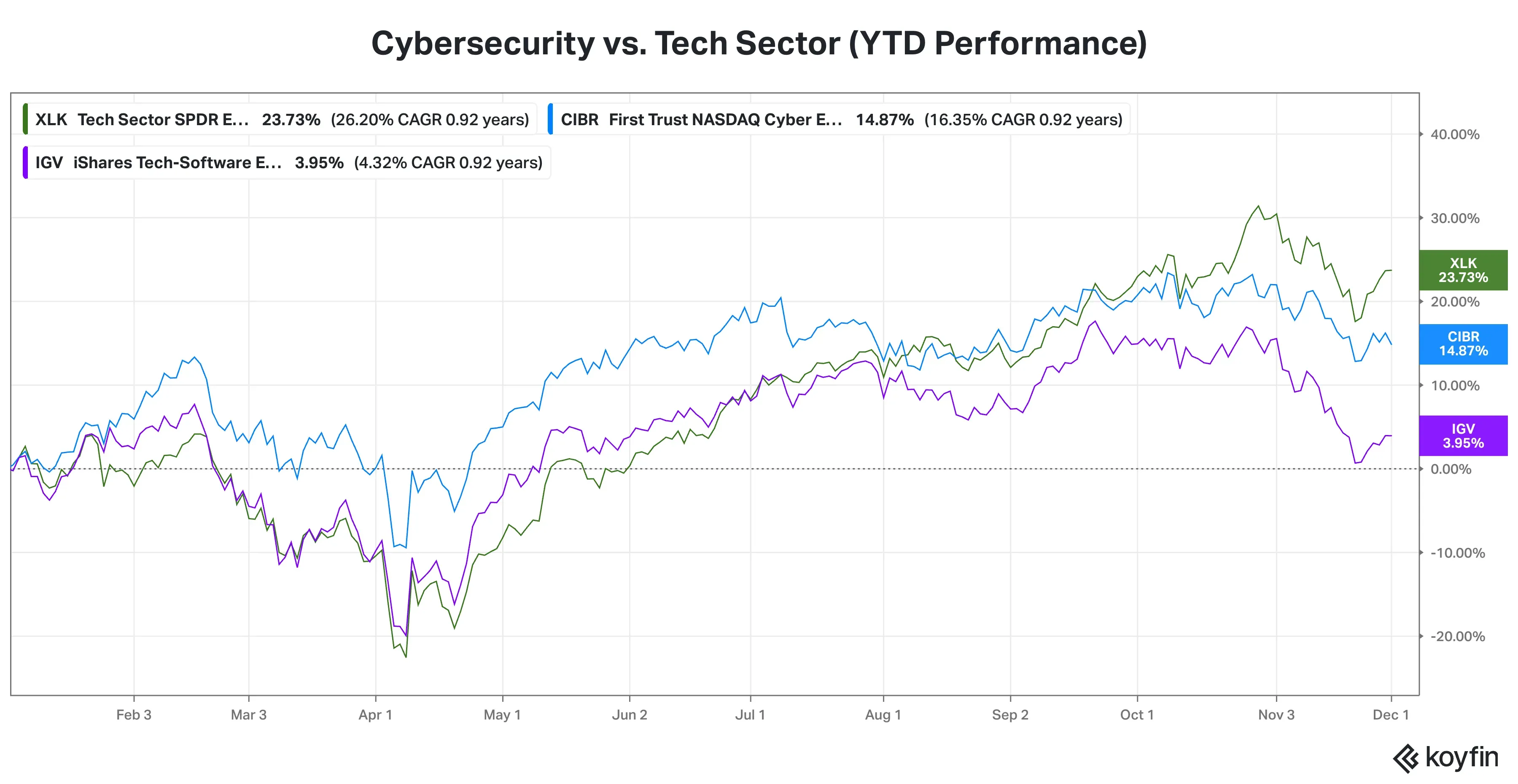

Cybersecurity stocks haven’t lived up to the hype despite the growing need for protection in an increasingly interconnected world. The First Trust NASDAQ Cybersecurity ETF (CIBR), an exchange-traded fund (ETF) that tracks cybersecurity companies, has risen about 15% compared with the Technology Select Sector SPDR Fund’s (XLK) 24% gain. But it has fared better than the iShares Expanded Tech-Software Sector ETF (IGV) (+4%).

Advertisement|Remove ads.

Source: Koyfin

Cybersecurity — High-Conviction Play for Analysts?

Wedbush tech analyst Daniel Ives believes the cybersecurity subsector could be an outperformer within the broader tech space amid the resilient spending trends. According to Morgan Stanley analyst Meta Marshall, the cybersecurity market is a $270 billion market and is set to grow at a 12% annual rate through 2028, the fastest growth rate across the software industry.

Marshall can’t have said enough to underscore the roaring opportunity:

Advertisement|Remove ads.

As the digital landscape grows increasingly complex, the scale and severity of cybercrime expand in tandem. This means that even as companies spend more, the risks are multiplying even faster. For investors, this is both a warning and an opportunity.

Morgan Stanley’s September survey showed that chief information officers expect cybersecurity spending to grow 50% faster than overall software spending.

Which Cybersecurity Name Is Best Bet?

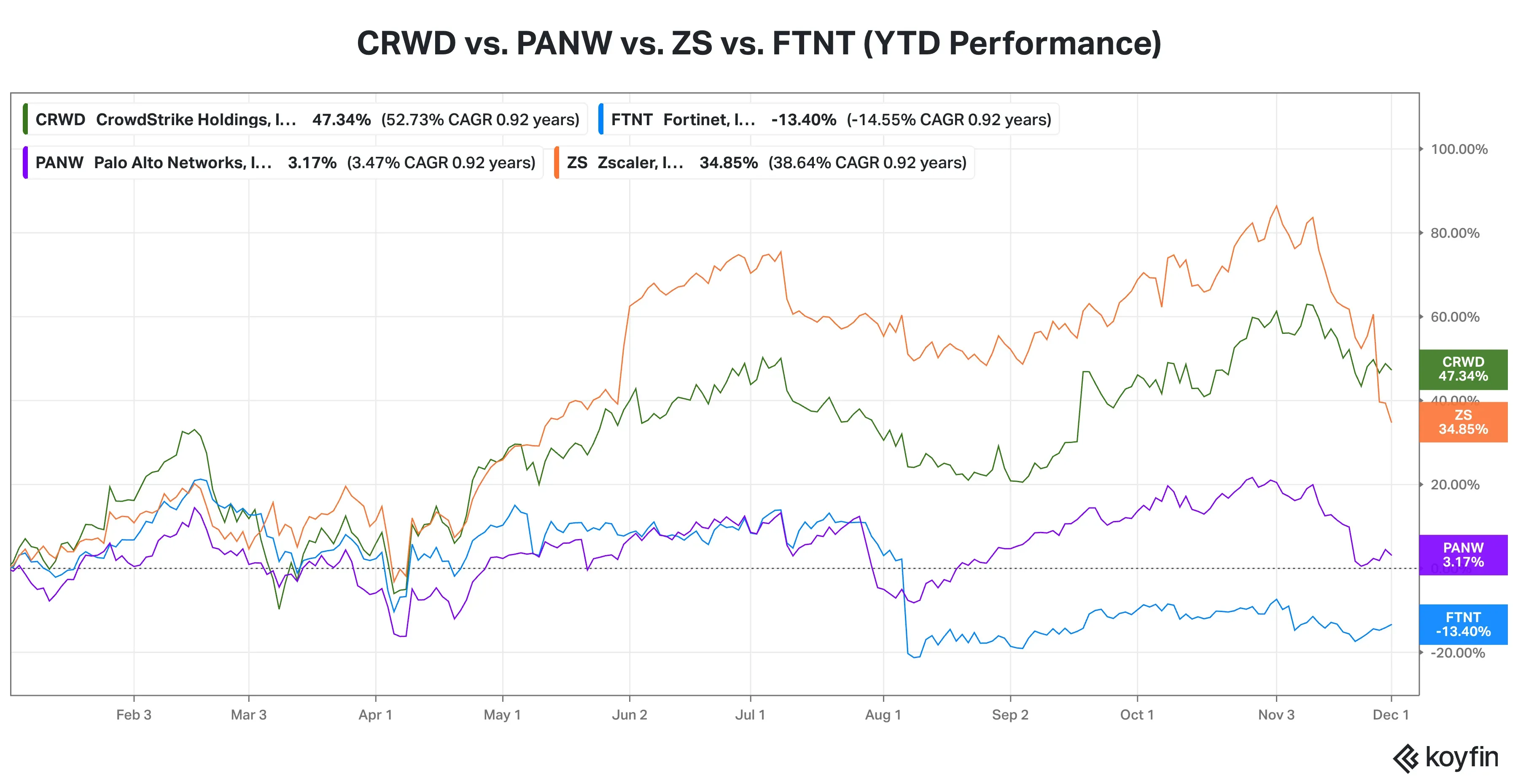

The cybersecurity industry may have enough room for multiple players to grow and thrive, as the massive market opportunity clarifies that it’s not a “zero-sum game.” For comparison purposes, we have considered the Nasdaq 100 names. Here’s a look at how the four Nasdaq 100 cybersecurity vendors, CrowdStrike, Zscaler, Palo Alto Networks and Fortinet, stack up on key metrics:

The comparisons are made up until the fiscal second quarter, given CrowdStrike is due to release its quarterly results after the market closes on Tuesday.

Advertisement|Remove ads.

CrowdStrike is the best performer among the quartet in terms of stock returns. Fortinet, meanwhile, has generated a negative return for the year.

Source: Koyfin

Advertisement|Remove ads.

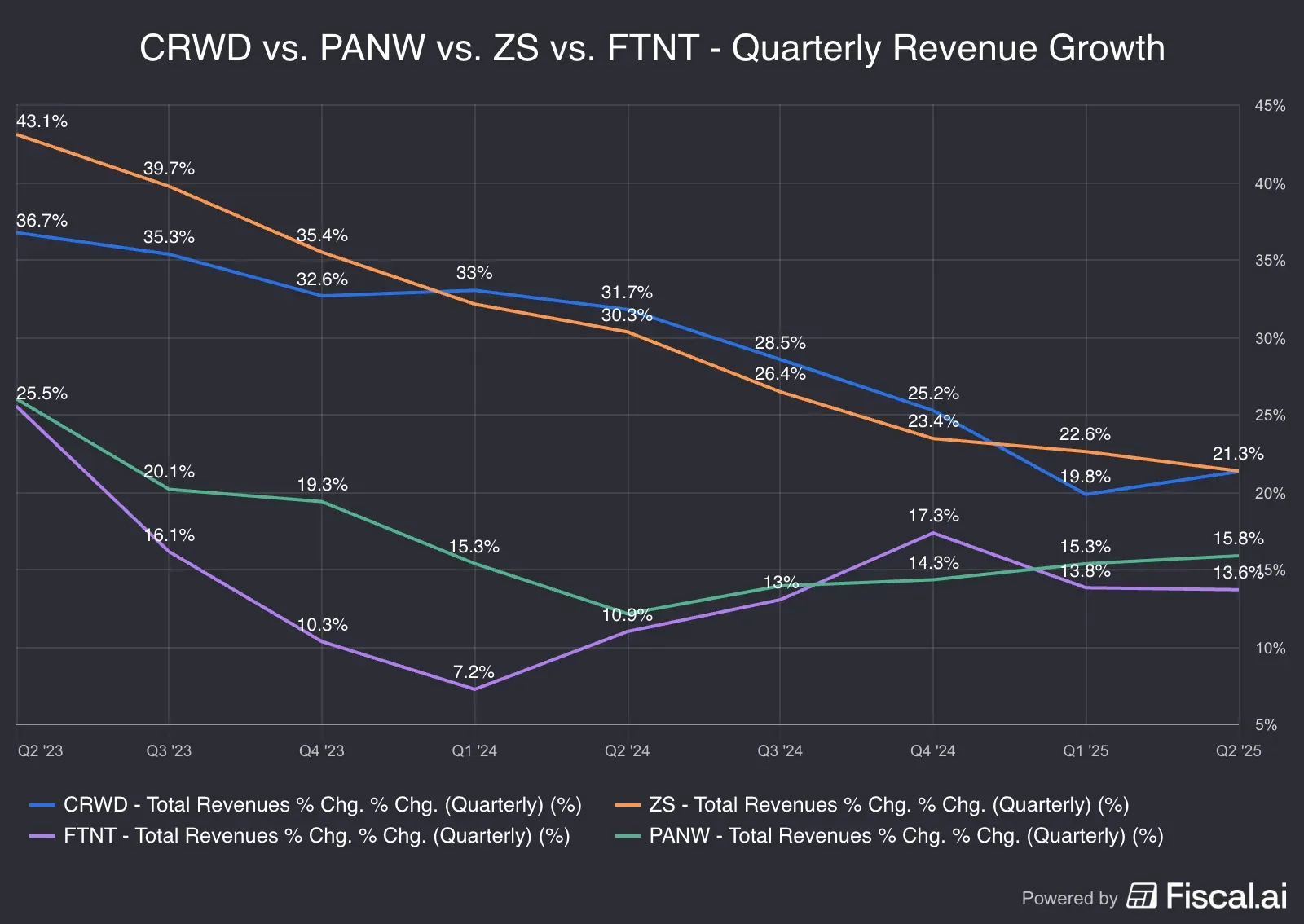

CrowdStrike and Zscaler have shown faster revenue growth than Palo Alto and Fortinet. Zscaler’s revenue growth accelerated in the fiscal third quarter, while CrowdStrike will disclose its growth on Tuesday.

Source: Fiscal.ai

Advertisement|Remove ads.

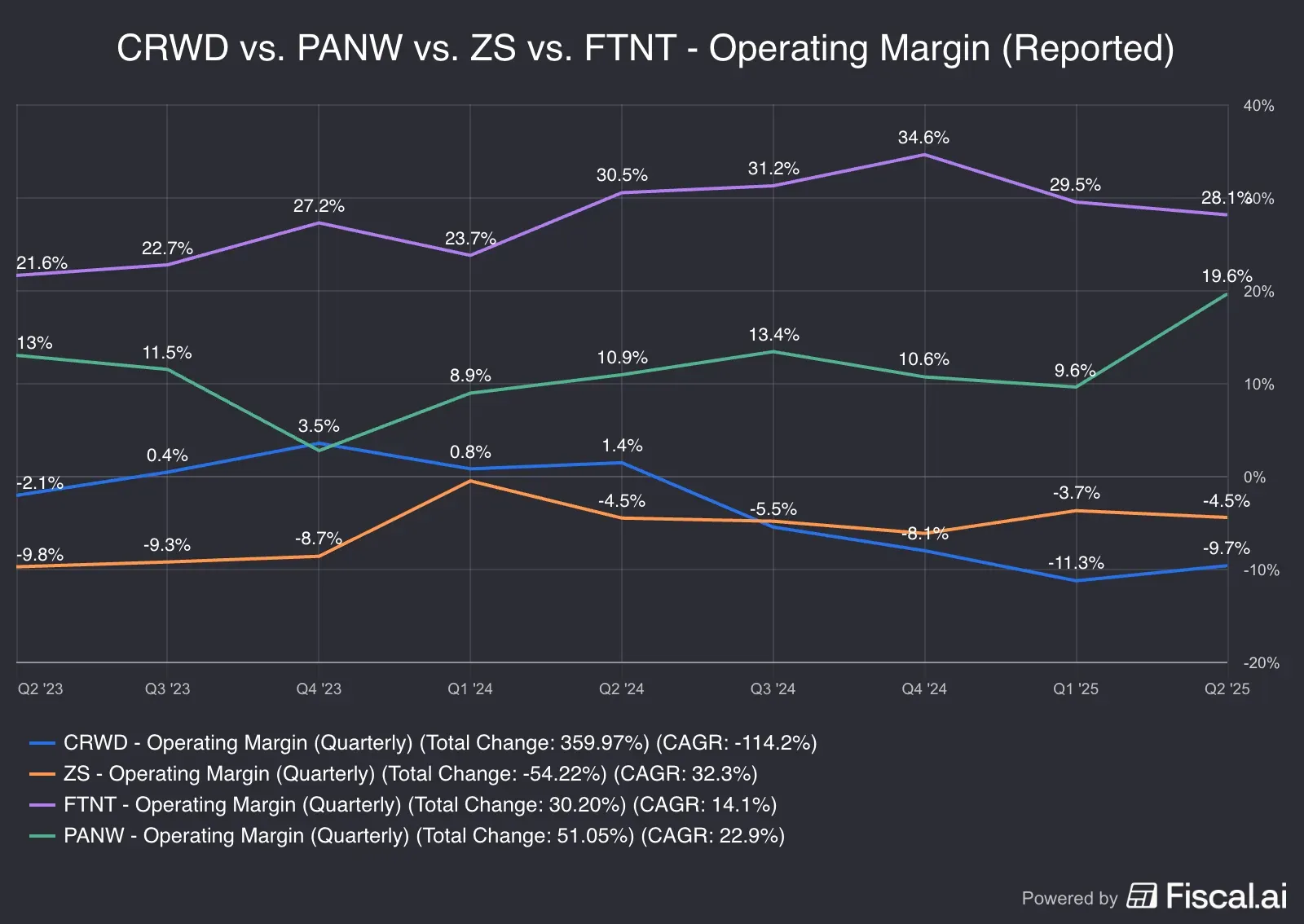

On a reported basis, only Fortinet and Palo Alto generated positive operating margins.

Source: Fiscal.ai

Advertisement|Remove ads.

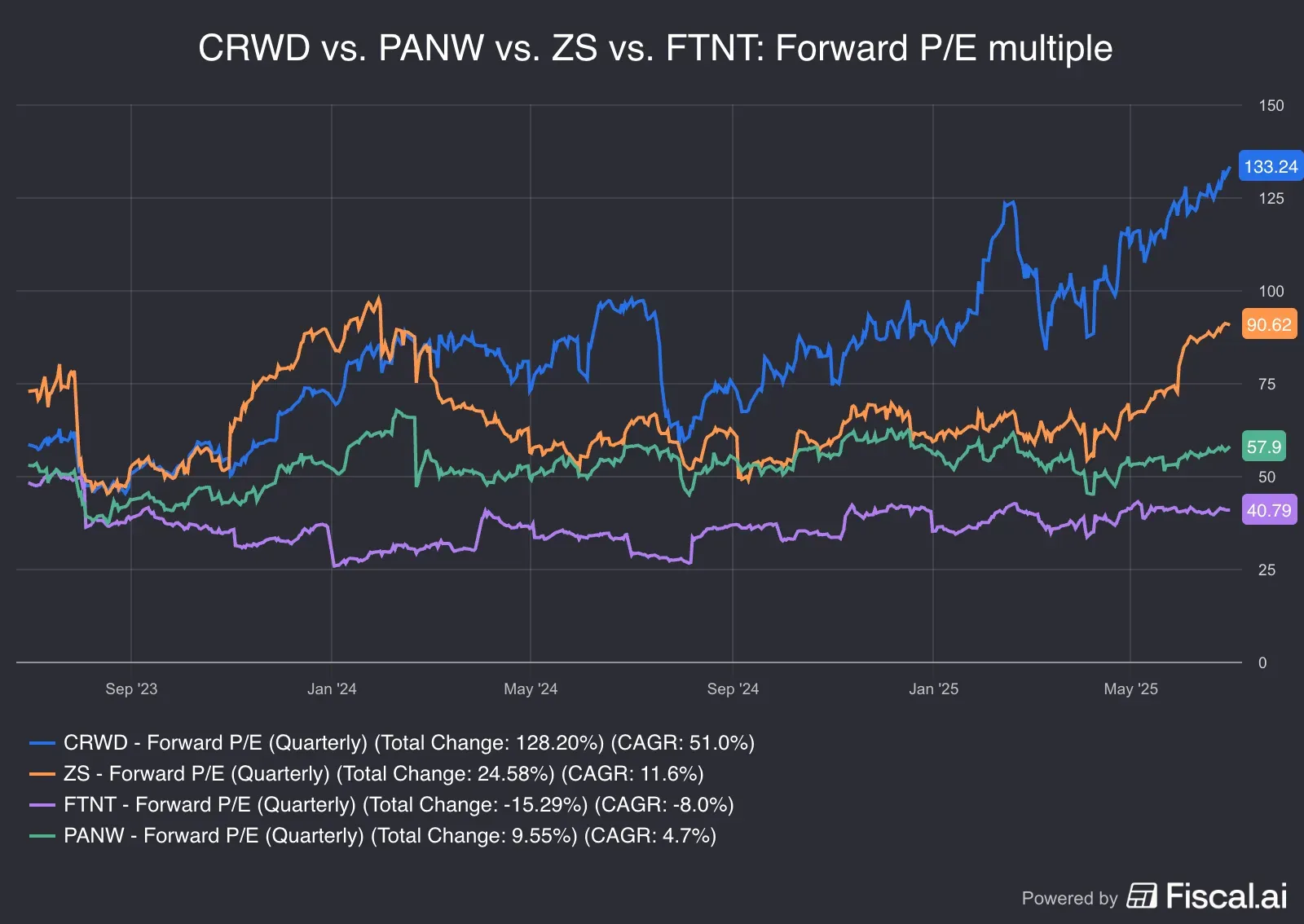

Comparisons of valuation based on a forward price-earnings (P/E) multiple show that Fortinet screens as the cheapest, followed by Palo Alto and Zscaler. CrowdStrike is the priciest among the lot. But Wedbush’s Daniel Ives sees the premium valuation as justified. In a note previewing the earnings, the analyst said, “We believe the Street is underestimating the growth potential for CrowdStrike as a second/third derivative beneficiary of the AI Revolution and this speaks to our core bullishness in the name continuing from current levels.”

Source: Fiscal.ai

Advertisement|Remove ads.

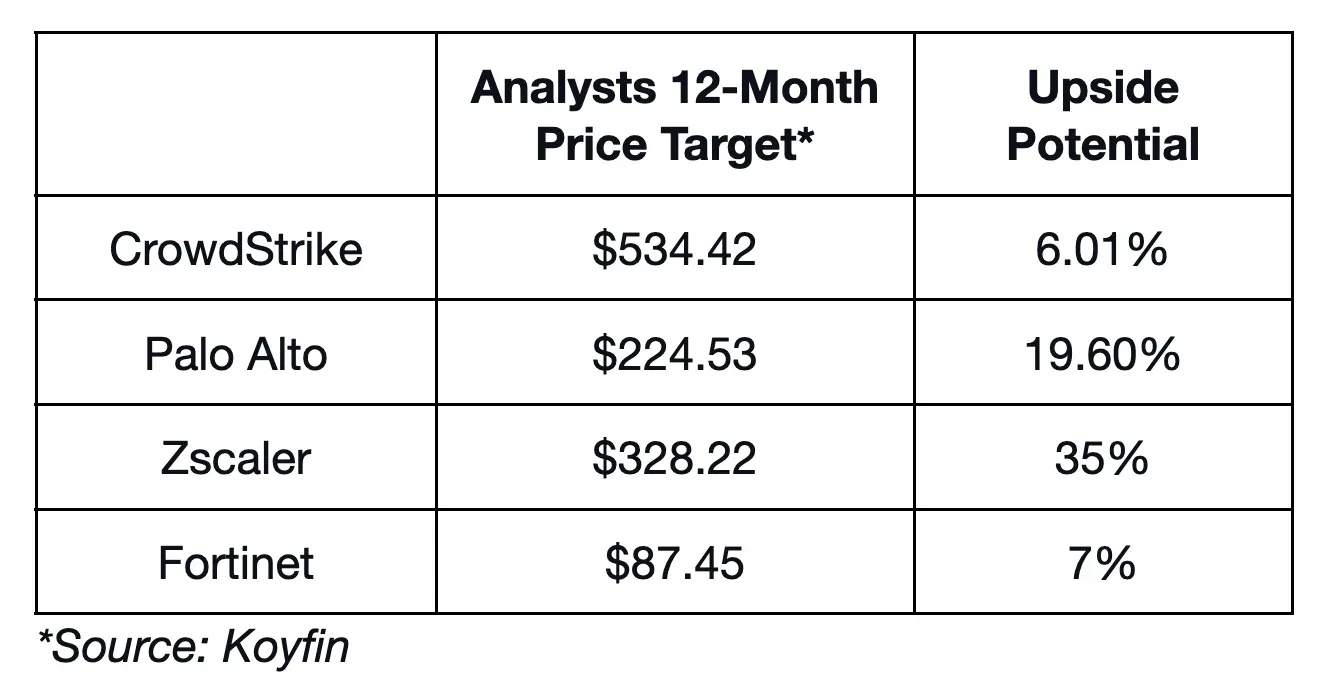

CRWD vs. PANW vs. ZS vs. FTNT Upside Potential

On Stocktwits, retail traders are ‘extremely bullish’ toward Zscaler and CrowdStrike, while they remained ‘neutral’ toward Palo Alto and Fortinet. Message volume was very brisk on the Zscaler stream and ‘high’ for CrowdStrike, while Palo Alto and Fortinet streams saw ‘low’ message volumes.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Read Next: Hey Siri, Is Apple Done Sleeping On AI? Wall Street Is Hunting For Clues Of An Awakening

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2161009632_81a55c17a0.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·14h ago

Anushka Basu·14h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2286019501_0704608c45.jpg) Anushka Basu·15h ago

Anushka Basu·15h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1234739851_1_4e5d1263a0.jpg) Anushka Basu·17h ago

Anushka Basu·17h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1317870360_fd65c7f7d0.jpg) Anushka Basu·19h ago

Anushka Basu·19h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2245018150_cbf31ea70f.jpg) Anushka Basu·20h agoAnushka Basu·22h ago

Anushka Basu·20h agoAnushka Basu·22h ago