Advertisement|Remove ads.

Physical Oil Markets Have Already Priced In US-Iran War, But Paper Markets Haven't, Says Veteran Investor: 'Repricing Will Be VIOLENT'

- The veteran investor believes the physical markets are on the right track.

- When paper oil prices catch up to physical prices, the repricing will be violent, according to Noble.

- Meanwhile, oil prices have been swinging wildly amid ongoing geopolitical uncertainty.

Advertisement|Remove ads.

As markets grapple with uncertainty about the outcome of the war in Iran and its impact on global energy prices, a former associate of legendary investor Peter Lynch is betting on energy stocks.

“Energy stocks remain the most asymmetric trade in this market,” said George Noble, a hedge fund veteran and former Fidelity fund manager, in a post on X on late Tuesday.

The investor highlighted the pricing difference between physical oil markets (spot oil, tanker bookings, actual delivery) and paper markets (futures contracts, options, financial instruments), saying that while the former was pricing in a war, the latter was pricing in a peace deal. “One of them is WRONG,” Noble said.

Advertisement|Remove ads.

Noble Backs This Indicator

The veteran investor believes the physical markets are on the right track. To back his claim, Noble pointed out that 230 loaded oil tankers were stuck in the Persian Gulf amid the blockade of the Strait of Hormuz, where traffic had dropped by over 90%.

He noted that normally 15 to 20 million barrels per day flowed through the critical waterway, but at present, alternatives via Saudi Arabia's East-West pipeline can only handle about 9 million barrels per day, creating a massive gap with no real workaround.

“You cannot close a gap that large with infrastructure that doesn't exist,” he said. “You cannot load 15 million barrels per day onto trucks. There is no land bridge for hydrocarbons. The pipelines are maxed. The tankers are parked,” he added.

Advertisement|Remove ads.

Noble also said that two separate battles were unfolding now — one the global supply chain has already adapted to, and another it simply can’t. Yet paper oil markets were trading as if that divide didn’t exist, he said.

Meanwhile, U.S. President Donald Trump said on Tuesday that the U.S. was extending a ceasefire with Iran, although the blockage of Iranian ports would continue.

Wild Market Swings

Oil prices have been swinging sharply, spiking on any hints of escalation in tensions between the U.S. and Iran, while pulling back on signs of renewed negotiations or ceasefire announcements. Energy stocks have been tracking the wild oscillations.

Advertisement|Remove ads.

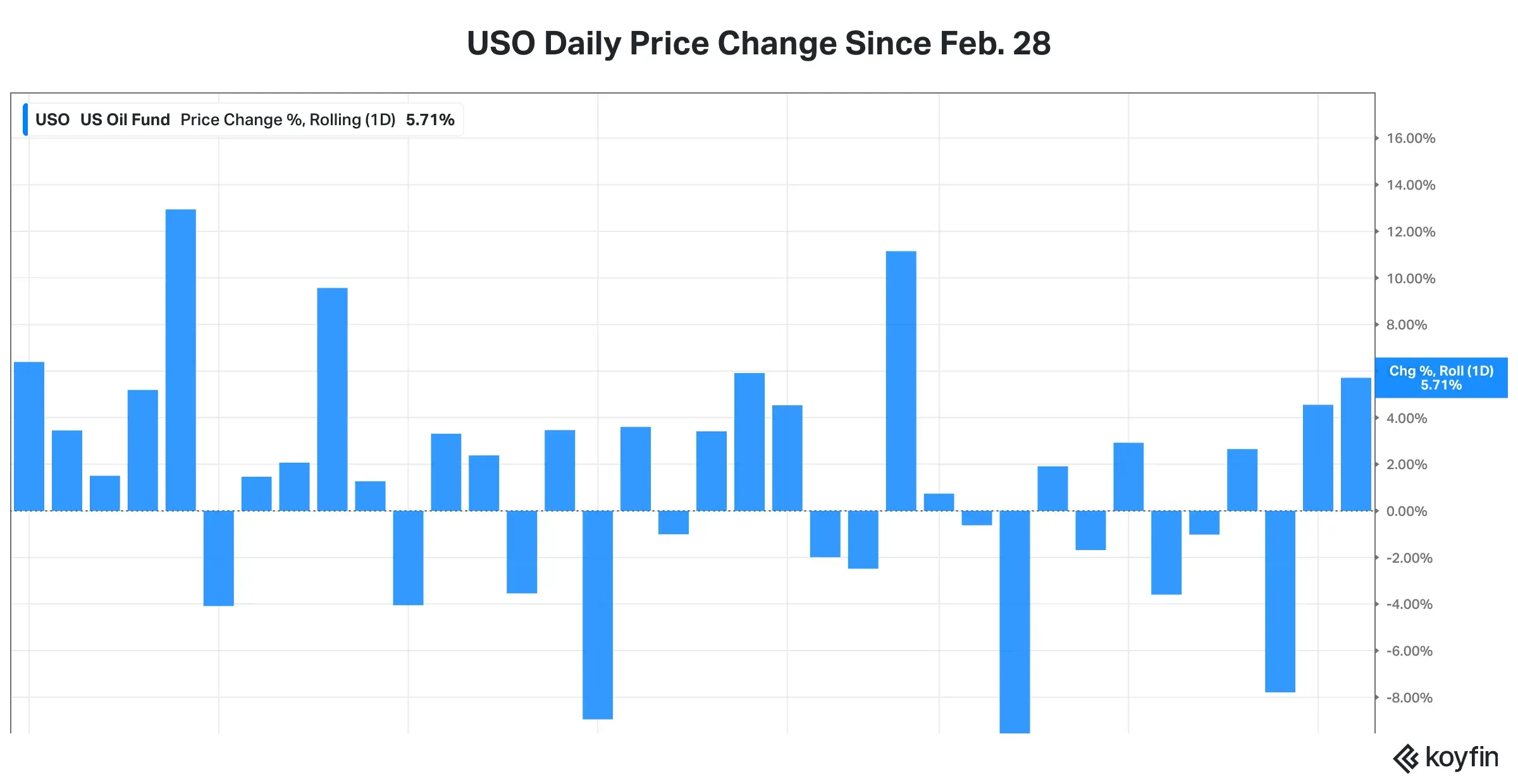

The United States Oil Fund (USO), an exchange-traded fund that tracks the daily price changes of West Texas Intermediate, has been whipsawing in tandem.

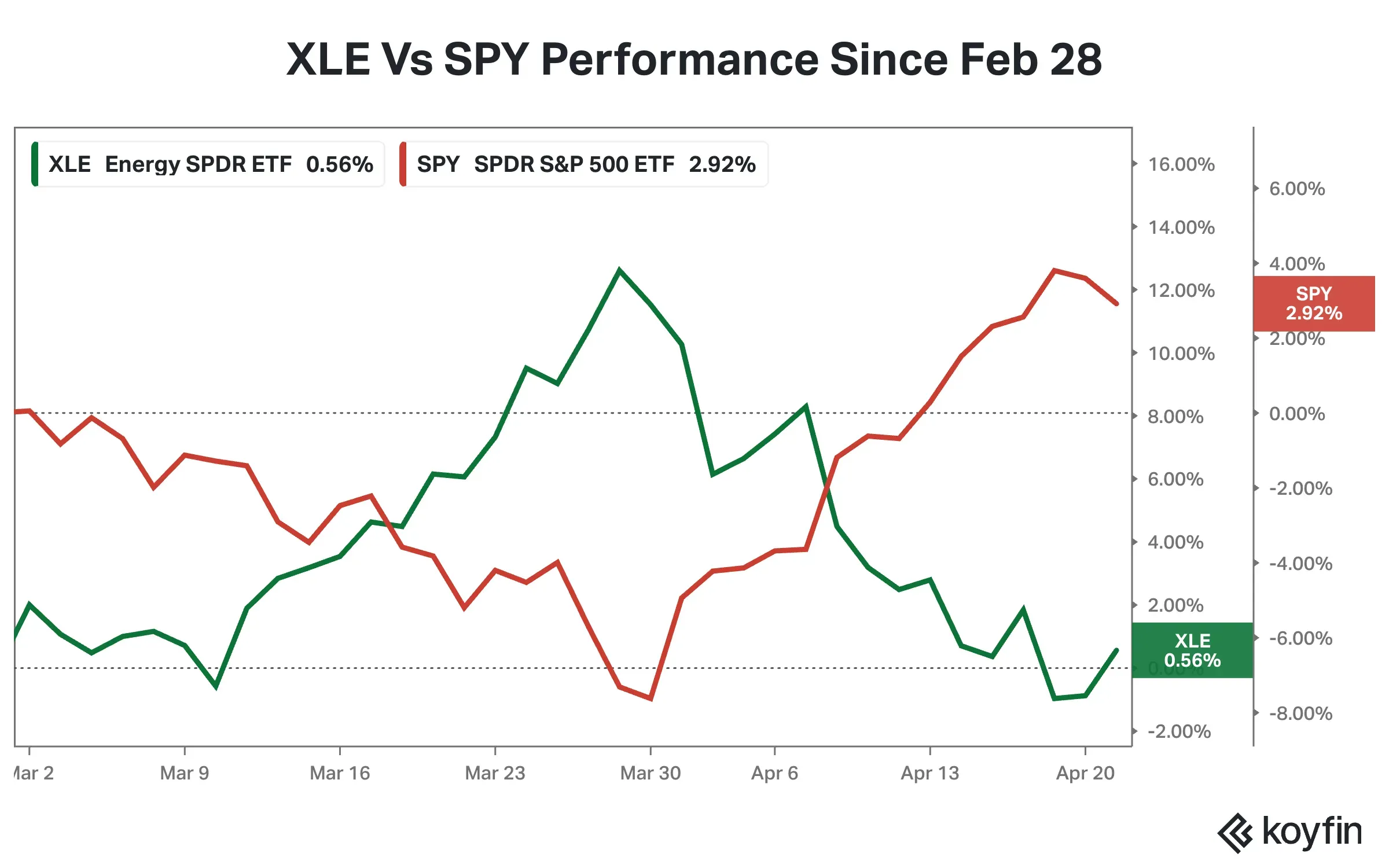

Meanwhile, the State Street Energy Select Sector SPDR ETF (XLE), which tracks American energy companies within the S&P 500, has diverged significantly from the S&P 500 since the start of the war — initially outperforming the benchmark index at the onset of the Hormuz crisis and finally lagging in after signs of a ceasefire and diplomatic breakthroughs.

Shares of major energy stocks have also been fluctuating. For instance, Battalion Oil Corp. (BATL) shares surged more than 38% at the close on Tuesday amid soaring crude oil prices, as uncertainty around an expansion of the U.S.-Iran ceasefire lingered. However, after Trump announced an extension late Tuesday, oil prices declined, pulling BATL's stock down by nearly 13% in overnight trading.

Advertisement|Remove ads.

Chevron Corp. (CVX) stock, meanwhile, was up 10.78% in the first month after the war, but has since pared most of those gains, declining about 10% so far this month. Exxon Mobil Corp. (XOM) and ConocoPhillips (COP) have also followed similar trajectories.

When paper oil prices catch up to physical prices, “the repricing will be VIOLENT,” Noble said.

The United States Oil Fund ETF (USO) has gained nearly 86% so far this year, while the ProShares Ultra Bloomberg Crude Oil ETF (UCO) has surged more than 115% in the same time. Retail sentiment around both was in the ‘bearish’ territory on Stocktwits at the time of writing.

Advertisement|Remove ads.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_btcmanwalking_resized_png_3188b2f46f.webp)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·8h ago

Anushka Basu·8h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2237640344_jpg_bc97a7240c.webp) Anushka Basu·9h ago

Anushka Basu·9h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2225439727_jpg_c06a69226a.webp) Anushka Basu·10h ago

Anushka Basu·10h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2216579148_jpg_3510da9502.webp) Anushka Basu·11h ago

Anushka Basu·11h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_michael_saylor_OG_3_jpg_bb6f728799.webp) Anushka Basu·13h ago

Anushka Basu·13h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1239809343_1_jpg_c4b4efa46e.webp) Anushka Basu·13h ago

Anushka Basu·13h ago