Advertisement|Remove ads.

SanDisk Outperforms Former Parent Western Digital With Nearly 600% YTD Gain — And Climbed To Top Of The S&P 500 Winners List: What Drove The Explosive Rally?

- Sandisk’s spin-off from Western Digital has been a runaway success, thanks to booming AI-related NAND demand, a tightening supply environment, and rapid margin improvement.

- The company’s fundamentals have improved notably.

- Analysts remain broadly optimistic—seeing SanDisk still in the early innings of the NAND cycle—yet caution that its explosive rally may require earnings to catch up.

Advertisement|Remove ads.

After its spin-off from Western Digital (WDC), SanDisk (SNDK) has outperformed its former parent. In under a year as an independent company, it has climbed past every other stock in the S&P 500 — even the Big Tech heavyweights.

Western Digital unveiled its breakup plan in late October 2024, proposing to issue one-third of a share of the newly formed SanDisk for every Western Digital share held. SanDisk returned to the public markets on Feb. 13, marking its second debut. Longtime industry watchers will recall that SanDisk was previously listed before Western Digital acquired it in 2016 for $16 billion.

SanDisk sells an array of flash memory storage products, such as SSDs (solid state drives), memory cards and USB flash drives.

Advertisement|Remove ads.

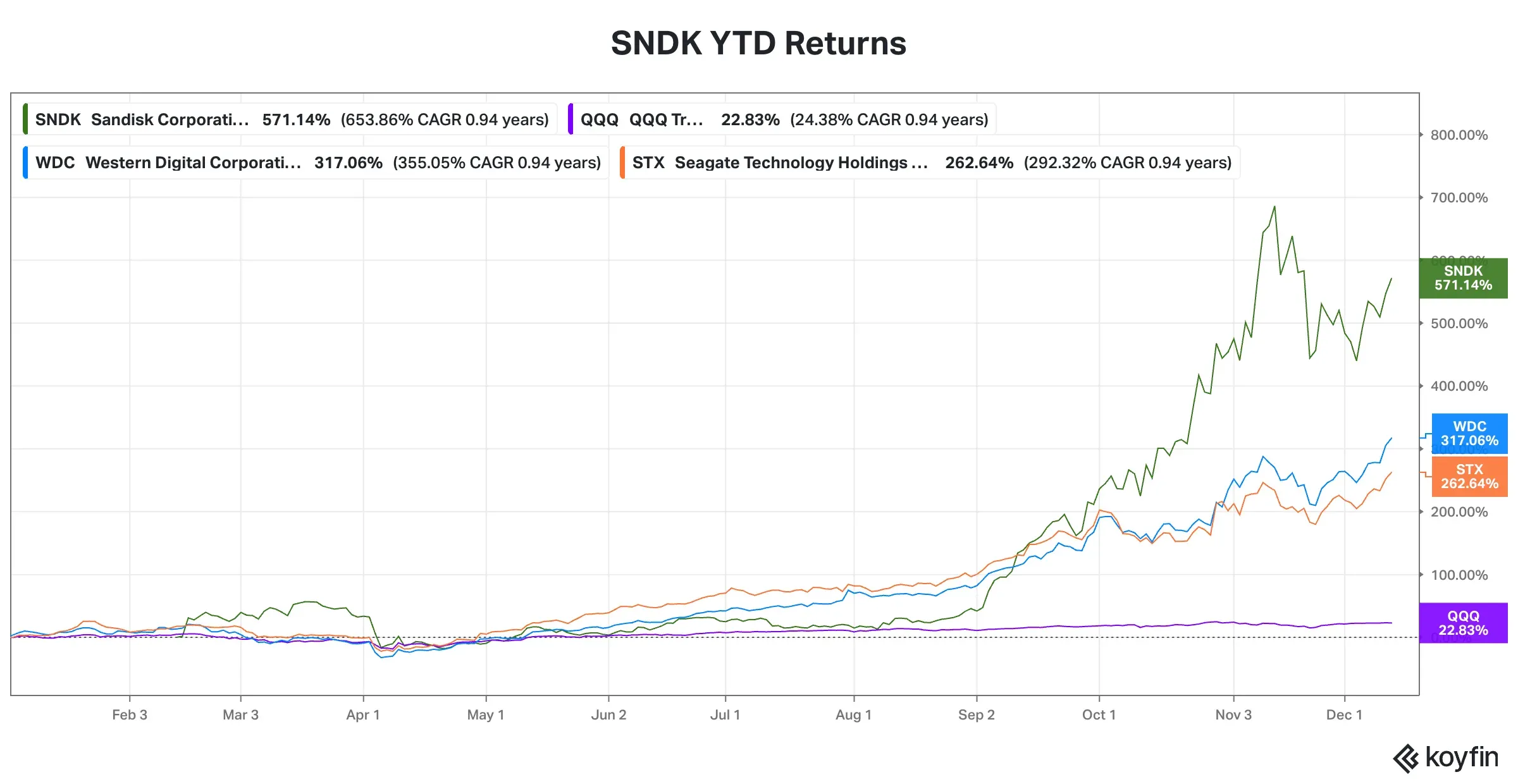

How Sandisk Stock Has Fared Since Listing

Since its debut, SanDisk’s stock has gained 571%, beating WDC and Seagate, another maker of storage solutions, by a mile.

Source: Koyfin

Source: Koyfin

After ending the debut session 18% below its intraday high at $36, Sandisk stock consolidated until early September. What followed was a stellar uptrend as the stock rose fivefold through mid-November. Another consolidation has followed since.

Advertisement|Remove ads.

Source: Koyfin

Source: Koyfin

Strong demand for NAND flash memory chips used in artificial intelligence (AI) infrastructure, an industry-wide supply crunch, and solid quarterly results helped keep the stock on an upward trajectory. The S&P 500's inclusion in late November prevented a steep slide, even as the rest of the AI-leveraged firms went into a tailspin.

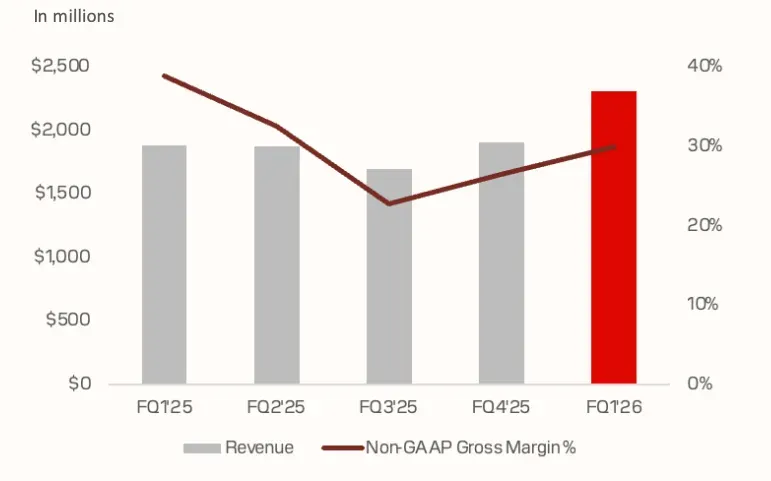

SNDK’s Fundamentals Inflect Higher

Sandisk’s revenue and adjusted gross margin have been trending higher since the third quarter of 2025, underpinned by strong demand across its end markets.

Advertisement|Remove ads.

Source: Company presentation

The company derived roughly 61% of its revenue from edge customers in the first quarter of fiscal year 2026, which ended on Oct. 3. Roughly 28% came from consumers, and the remainder from the data center end market.

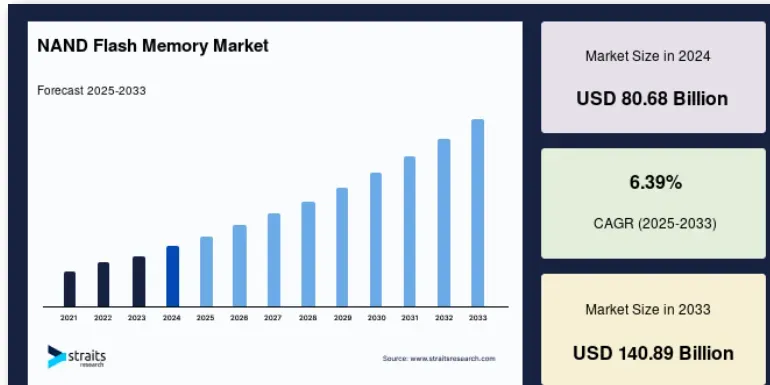

Tapping Growth Hotspot

According to Straits Research, the global NAND flash memory market was valued at roughly $81 billion in 2024, and is poised to grow at a compounded annual growth rate of 6.4% to $141 billion by 2033.

Advertisement|Remove ads.

Source: Straits Research

Advertisement|Remove ads.

Sandisk is focusing on the lucrative data center end market, which grew 26% sequentially in its first quarter. The company said in its earnings presentation that data center and AI infrastructure investment is set to surpass $1 trillion by 2030. It noted strong demand for storage-focused “Stargate” product line and also confirmed that two qualifications with hyperscalers were underway.

The company also expects to add another hyperscaler, along with a major storage OEM, in 2026.

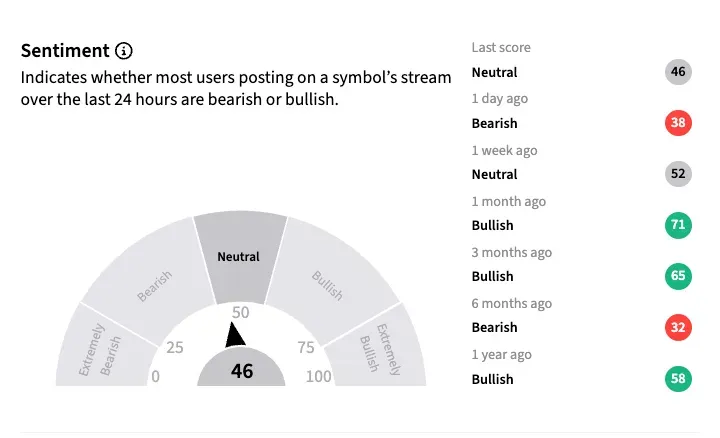

Retail in ‘Wait-and-Watch Mode

From the bullishness seen at the start of the year, retail traders’ mood has fluctuated. As they digest the strong stock gains, sentiment has largely been muted, as seen on Stocktwits’ sentiment meter.

Advertisement|Remove ads.

According to Koyin, the average one-year analysts’ price target for Sandisk is $264.95, implying scope for another 10% upside — not a bad proposition for a stock that has run up too much, too swiftly. Fourteen of the 21 analysts covering the stock rate it as a ‘Buy’ or ‘Strong Buy,’ while six remain in a ‘Hold’ pattern and one has a ‘Sell’ rating.

Wary after the strong rally, in early November, Morgan Stanley’s semiconductor analyst Joseph Moore removed the “Top Pick” status he had accorded to the stock. Explaining the logic, he said:

Advertisement|Remove ads.

“We remain bullish on SNDK after this run, but think it will take time for earnings to grow into the current stock price.”

Morgan Stanley is still ‘Overweight’ on Sandisk. The firm believes that the stock can continue to outperform as the NAND cycle remains in early innings.

As recently as this week, JPMorgan initiated coverage of the stock with a ‘Neutral’ rating, the Fly reported. It sees Sandisk offering leverage to the AI-driven enterprise solid-state disk “supercycle” with a structurally advantaged cost base from its joint venture with Japanese peer Kioxia. Still, it views the company’s current pricing power as a cyclical peak rather than a structural reset.

For updates and corrections, email newsroom[at]stocktwits[dot]com.

Advertisement|Remove ads.

Comments posted here will also appear on symbol pages.

Latest News

/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_1407197934_3a2e8235c9.jpg)

/filters:format(webp)https://news.stocktwits-cdn.com/Anushka_Basu_make_me_smile_in_the_picture_b92832aa_af59_4141_aacc_4180d2241ba8_1_2_png_1086e0ed8c.webp) Anushka Basu·14h ago

Anushka Basu·14h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2197413796_2ae5f600f7.jpg) Anushka Basu·15h ago

Anushka Basu·15h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2279969005_jpg_d203b64c52.webp) Anushka Basu·16h ago

Anushka Basu·16h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2244288176_jpg_c3909aa8e5.webp) Anushka Basu·16h ago

Anushka Basu·16h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_Getty_Images_2272863239_jpg_ed937b18d0.webp) Anushka Basu·17h ago

Anushka Basu·17h ago/filters:format(webp)https://news.stocktwits-cdn.com/large_andre_francois_mckenzie_i_G_Yi_Bhd_N_Tp_E_unsplash_jpg_3d063f0b23.webp) Anushka Basu·19h ago

Anushka Basu·19h ago